This content may include information about products, features, and/or services that SoFi does not provide and is intended to be educational in nature.

A “good” return on investment is subjective, but in a very general sense, a good return on investment could be considered to be about 7% per year, based on the average historic return of the S&P 500 index, and adjusting for inflation. But of course what one investor considers a good return might not be ideal for someone else.

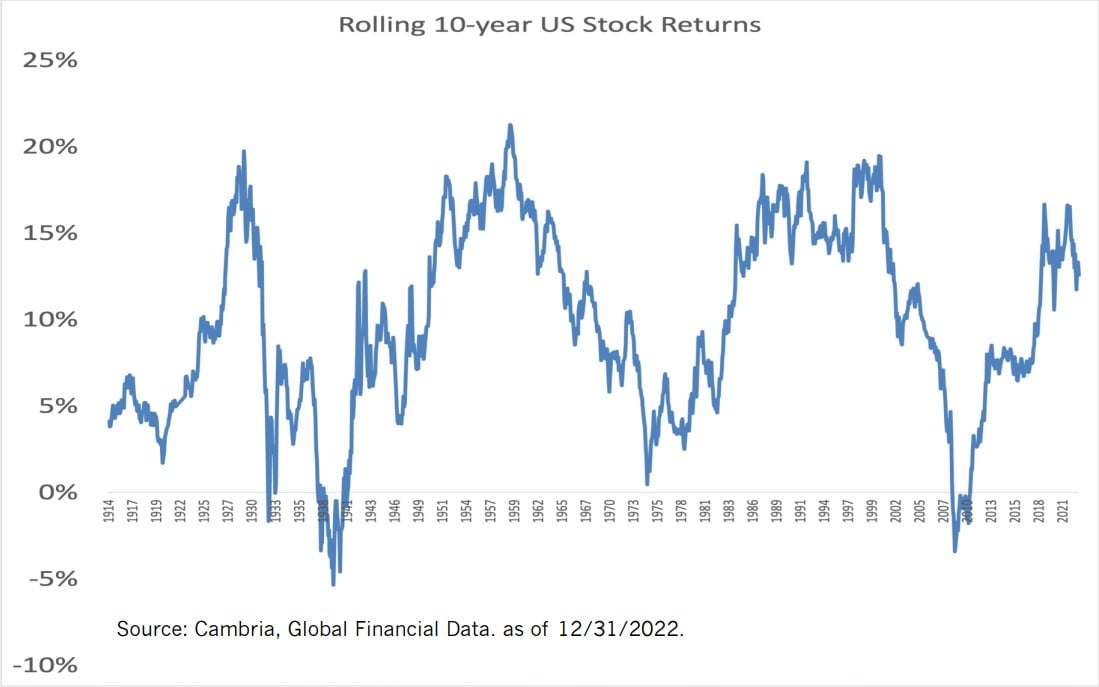

And while getting a “good” return on your investments is important, it’s equally important to know that the average return of the U.S. stock market is just that: an average of the market’s performance, typically going back to the 1920s. On a year-by-year basis, investors can expect returns that might be higher or lower — and they also have to face the potential for outright losses. In addition, the S&P 500 is a barometer of the equity markets, and it only reflects the performance of the 500 biggest companies in the U.S. Most investors will hold other types of securities in addition to equities, which can affect their overall portfolio return.

• A good return on investment is generally considered to be around 7% per year, based on the average historic return of the S&P 500 index, adjusted for inflation.

• The average return of the U.S. stock market is around 10% per year, adjusted for inflation, dating back to the late 1920s.

• Different investments, such as CDs, bonds, stocks, and real estate, offer varying rates of return and levels of risk.

• Investing in stocks carries higher potential returns but also higher risk, while investments like CDs offer lower returns but are considered lower-risk.

Have you ever stared at your investment account and wondered, “Am I actually making enough money here?” You’re not alone. As someone who’s spent countless hours researching this topic, I’ve found that understanding what makes a “good” rate of return is crucial for any investor. Let’s dive into what you should realistically expect from your investments over a 10-year period.

The Magic Number: What History Tells Us

When we look at historical data, the S&P 500—often considered the benchmark for the overall stock market—has delivered an average annual return of 10.11% since 1928 through the third quarter of 2025. But here’s the kicker: once you adjust for inflation, that number drops to about 6.84% in real terms.

This means if your investments are growing at around 7-10% annually over a decade, you’re basically keeping pace with the market’s long-term average. Not too shabby!

But is that “good”? Well, that depends on several factors we’ll explore

Breaking Down “Good” Returns by Investment Type

Different investments come with different expectations Here’s what you might consider “good” depending on where your money is parked

| Investment Type | “Good” 10-Year Average Annual Return |

|---|---|

| Stocks/Equity Funds | 8-12% |

| Bonds | 3-5% |

| Real Estate | 7-10% |

| Mixed Portfolio (60/40) | 6-8% |

| Cash/CDs/Money Markets | 1-3% |

Keep in mind that these figures are before inflation. In real terms (after inflation), you’d subtract roughly 2-3% from each of these numbers.

The Impact of Inflation: Your Silent Return Thief

I can’t stress this enough—inflation is like a stealthy pickpocket that silently steals your purchasing power over time. A 10% return sounds fantastic until you realize that with 3% inflation, your real return is closer to 7%.

This is why simply keeping money under your mattress (or even in a low-yield savings account) is actually losing you money over time!

To illustrate this point, consider that the S&P 500’s nominal average annual return of 10.11% since 1928 translates to only about 6.84% when adjusted for inflation. That’s a significant difference that compounds over decades.

Market Timing: The Return Wildcard

One thing that drives me crazy about most investment articles is they assume you invested at some perfect moment. In reality, when you enter the market drastically affects your returns.

For instance, if you had invested in the S&P 500 in early 2009 (right after the financial crisis), your 10-year return would’ve been phenomenal—well above the long-term average. But if you’d invested in late 2007 (right before the crash), your 10-year return would’ve been much lower.

This is why financial advisors typically recommend dollar-cost averaging—investing a fixed amount periodically regardless of market conditions. It helps avoid the risk of dumping all your money in at market peaks.

Concentration Risk: The Magnificent Seven Effect

An important factor affecting modern returns is the increasing concentration of the S&P 500. As of May 2025, just seven companies—the “Magnificent Seven” (Alphabet, Apple, Amazon, Meta, Microsoft, NVIDIA, and Tesla)—accounted for about 33.5% of the entire index’s market value.

This concentration can be a double-edged sword:

- When these tech giants perform well, they can significantly boost overall returns

- When they struggle, they can drag down the entire market

For perspective, this level of concentration is similar to what we saw just before the dot-com bubble burst in 2000, which makes some investors nervous.

Realistic Expectations Based on Your Investment Timeline

Your investment horizon plays a huge role in what constitutes a “good” return. Here’s my take:

Short-Term (1-3 years)

- Highly unpredictable

- Even “good” investments might show negative returns

- Focus on preservation rather than growth

Medium-Term (3-7 years)

- Returns begin to normalize but can still vary widely

- Annual returns of 5-8% might be considered good

- Still vulnerable to market cycle timing

Long-Term (10+ years)

- This is where historical averages become meaningful

- Annual returns of 7-10% (before inflation) are solid

- Compounding starts working its real magic

How to Invest in the S&P 500 to Get These Returns

Since we’ve used the S&P 500 as our benchmark, you might be wondering how to actually invest in it. You can’t buy the index directly, but you can invest in funds that track it.

The most popular options include:

- SPDR S&P 500 ETF Trust (SPY) – The oldest and most liquid S&P 500 ETF

- iShares Core S&P 500 ETF (IVV) – Slightly lower expense ratio than SPY

- Vanguard S&P 500 ETF (VOO) – Known for its ultra-low fees

These funds will give you essentially the same returns as the S&P 500 index (minus a small expense ratio).

Factors That Could Impact Your Personal Returns

Remember, the average return isn’t necessarily YOUR return. Several factors will impact what you actually earn:

- Fees and expenses: Even small differences in expense ratios can significantly impact long-term returns

- Taxes: Capital gains and dividend taxes can take a bite out of your returns

- Your asset allocation: More stocks generally mean higher potential returns but also higher volatility

- Your behavior: Panic selling during downturns or chasing hot investments can destroy returns

- Rebalancing strategy: How and when you rebalance your portfolio affects long-term performance

Is 7% a Good Return Over 10 Years?

I get this specific question a lot. If you’re earning a consistent 7% average annual return over 10 years, you’re doing quite well! This would be:

- Above the inflation-adjusted historical average

- Enough to double your money in about 10 years (using the Rule of 72)

- Better than many professional money managers achieve consistently

Setting Realistic Goals for Your Next Decade

So what should you aim for in the next 10 years? Here’s my practical advice:

- Conservative goal: 5-6% average annual return (3-4% after inflation)

- Moderate goal: 7-8% average annual return (5-6% after inflation)

- Aggressive goal: 9-10%+ average annual return (7-8%+ after inflation)

These targets assume a diversified portfolio with a reasonable asset allocation based on your risk tolerance and time horizon.

The Power of Consistent Returns Over 10 Years

Let’s see how different rates of return would grow a $10,000 investment over 10 years:

| Average Annual Return | Value After 10 Years | Real Value (After 2.5% Inflation) |

|---|---|---|

| 5% | $16,289 | $12,746 |

| 7% | $19,672 | $15,392 |

| 9% | $23,674 | $18,523 |

| 11% | $28,394 | $22,212 |

This demonstrates why even small differences in return rates make a huge difference over time. The difference between 7% and 9% might not seem like much, but it results in an additional $4,000+ on a $10,000 investment over a decade!

Adjusting Expectations for Different Life Stages

Your definition of a “good” return should evolve as your life circumstances change:

Early Career (20s-30s)

- Higher risk tolerance

- Longer time horizon

- Can aim for 8-10%+ returns

- Should emphasize growth over stability

Mid-Career (40s-50s)

- Balanced approach

- Still need growth but with less volatility

- 6-8% returns might be appropriate

- Should start introducing more stability

Near/In Retirement (60s+)

- Capital preservation becomes crucial

- Income generation often prioritized over growth

- 4-6% returns might be considered good

- Should focus on reducing drawdown risk

My Final Thoughts

When it comes to determining what’s a “good” rate of return over 10 years, context is everything. A 7% average annual return that you can actually stick with through market turbulence is infinitely better than chasing 12% returns if you’ll panic sell during the next market crash.

The most important factors are:

- Beating inflation by a healthy margin

- Making progress toward your specific financial goals

- Maintaining a risk level that lets you sleep at night

- Staying invested consistently rather than timing markets

Remember that even the S&P 500’s impressive long-term average of 10.11% (or 6.84% after inflation) came with significant volatility, including several periods where investors saw negative returns for extended periods.

In my view, if you’re averaging 7-8% annually over a decade, you’re doing well by historical standards—especially if you’re achieving this with a diversified portfolio that matches your risk tolerance.

What’s your experience been with investment returns? Are you satisfied with what you’ve earned over the past decade? I’d love to hear your thoughts in the comments!

What Is a Good Rate of Return for Various Investments?

As noted above, determining a good rate of return will also depend on the specific investments you hold, and your asset allocation. You can always calculate the expected rate of return for various securities. Here are different types of securities to consider.

Purchasing a bond is basically the same as loaning your money to the bond-issuer, like a government or business. Similar to a CD, a bond is a way of locking up a certain amount of money for a fixed period of time.

Here’s how it works: A bond is purchased for a fixed period of time (the duration), investors receive interest payments over that time, and when the bond matures, the investor receives their initial investment back.

Generally, investors earn higher interest payments when bond issuers are riskier. An example may be a company that’s struggling to stay in business. But interest payments may be lower when the borrower is trustworthy, like the U.S. government, which has never defaulted on its Treasuries.

“Investing in stocks can offer the potential to earn a high rate of return in the long term, but that potential comes with some risk. They’re one of the more volatile forms of investing for the short and medium term.”

-Brian Walsh, CFP® and Head of Advice & Planning at SoFi

Stocks can be purchased in a number of ways. But the important thing to know is that a stock’s potential return will depend on the specific stock, when it’s purchased, and the risk associated with it. Again, the general idea with stocks is that the riskier the stock, the higher the potential return.

This doesn’t necessarily mean you can put money into the market today and assume you’ll earn a large return on it in the next year. But based on historical precedent, your investment may bear fruit over the long-term. Because the market on average has gone up over time, bringing stock values up with it, but stock investors have to know how to handle a downturn.

As mentioned, the stock market averages a return of roughly 7% per year, adjusted for inflation.

Returns on real estate investing vary widely. It mostly depends on the type of real estate — if you’re purchasing a single house versus a real estate investment trust (REIT), for instance — and where the real estate is located.

As with other investments, it all comes down to risk. The riskier the investment, the higher the chance of greater returns and greater losses. Investors often debate the merit of investing in real estate versus investing in the market.

Why Your Money Might Lose Value If You Don’t Invest it

It’s helpful to consider what happens to the value of your money if you simply hang on to cash.

Keeping cash can feel like a lower-risk alternative to investing, so it may seem like a good idea to deposit your money into a traditional savings account. But cash slowly loses value over time due to inflation; that is, the cost of goods and services increases with time, meaning that cash has less purchasing power. Inflation can also impact your investments.

Interest rates are important, too. Putting money in a savings account that earns interest at a rate that is lower than the inflation rate guarantees that money will lose value over time. This is why, despite the risks, investing money is often considered a better alternative to simply saving it: The inflation risk is typically lower.

What is a Good Rate of Return on My Investments? – Gary Mishuris

FAQ

What is a good 10 year return on investment?

Is 7% return on investment realistic?

General ROI: A positive ROI is generally considered good, with a normal ROI of 5-7% often seen as a reasonable expectation. However, a strong general ROI is something greater than 10%. Return on Stocks: On average, an ROI of 7% after inflation is often considered good, based on the historical returns of the market.

What is the average market return over the past 10 years?

Can you live off interest of $1 million dollars?