How long youve had credit affects your score. But paying on time and not using a lot of your limit matter more.

Many, or all, of the products featured on this page are from our advertising partners who compensate us when you take certain actions on our website or click to take an action on their website. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and heres how we make money.

Whether you’ve had credit for six months or 20 years can make a difference in your credit scores.

A long track record without any major slip-ups suggests that your credit behavior will be similar in the future — and lenders and credit card issuers like that.

Credit scoring company VantageScore combines two things in its 3.0 scoring model — how long you’ve been using credit and what types of credit you have — into a single factor and considers it “highly influential.” FICO credit scores break it out a little differently, with the length of your credit history accounting for 15% of your score and the mix of accounts making up 10%.

Hey there, fam! Ever wondered why some folks got credit scores that shine brighter than a new penny, while others are stuck in the mud? Well, lemme tell ya, one sneaky lil’ factor is somethin’ called “credit age.” At MoneyMaverick, we’re all about breakin’ down the complicated money stuff into bite-sized, easy-to-digest chunks So, grab a coffee (or a soda, no judgment here), and let’s dive into what a good credit age really means and how it can be your secret weapon to boostin’ that score

So, What Exactly Is Credit Age?

Let’s kick things off with the basics. Credit age ain’t nothin’ but the average length of time all your credit accounts have been open. Think of it like the silent ninja of your credit score—it’s workin’ behind the scenes, quietly shapin’ how lenders see ya. Every credit card, loan, or line of credit you’ve got open gets factored into this average. The older the average, the better you look to banks and credit card companies.

Here’s the deal when you first start out maybe with that shiny new credit card at 18 or 20 your credit age is gonna be super young—like, baby young. But as you keep accounts open and active over the years, that age creeps up. And trust me, lenders love seein’ a seasoned credit history. It tells ‘em, “Hey, this person’s been at this game for a while and ain’t messin’ up.”

Why Does Credit Age Matter So Much?

Now, you might be thinkin’, “Why should I care about how old my credit is?” Fair question! Here’s the scoop: credit age plays a big role in your overall credit score. If we’re talkin’ FICO scores (one of the big dogs in credit scorin’), the length of your credit history makes up about 15% of your total score. Another 10% comes from the mix of credit types you’ve got—like cards, loans, or mortgages. So, that’s a solid chunk of your score tied to how long you’ve been playin’ the credit game.

There’s another system called VantageScore that lumps credit age and credit mix together as a “highly influential” factor. Either way, whether it’s FICO or VantageScore, the message is clear: the longer you’ve had credit without major slip-ups, the more trustworthy you seem to lenders. It’s like havin’ a long resume—it shows you’ve got experience.

What’s Considered a “Good” Credit Age?

Alright, let’s get to the juicy part what’s a good credit age? Here’s the thing—it ain’t a one-size-fits-all number It depends on where you’re at in life If you’re in your early 20s, havin’ a credit age of just a couple years might be fine. But if you’re pushin’ 40, you’d wanna aim for a decade or more of credit history under your belt.

Now, let’s tie this to credit scores for a clearer picture. Word on the street is that the average credit score for folks aged 18 to 26 hovers around 680. For peeps between 27 and 42, that average bumps up a bit to between 680 and 690. If your score is sittin’ in that range or higher for your age group, you’re likely in good shape, and your credit age is probably helpin’ ya out. A longer credit age often means you’ve had time to build a solid track record, which boosts that score.

Here’s a quick lil’ table to give you a rough idea of how credit age might look across different life stages:

| Age Group | Average Credit Age (Rough Estimate) | Average Score Range |

|---|---|---|

| 18-26 | 1-5 years | Around 680 |

| 27-42 | 5-15 years | 680-690 |

| 43-58 | 15-25 years | 690-720 |

| 59+ | 25+ years | 720+ |

Keep in mind, these are just ballpark figures. Your personal credit age being “good” depends on how it stacks up with your payment history and other factors. But generally, the longer, the better.

How Credit Age Fits Into the Bigger Picture

Before you go obsessin’ over your credit age, let’s put it in perspective. Yeah, it’s important, but it ain’t the whole story. There’s other stuff that weighs way heavier on your credit score. Lemme break it down for ya:

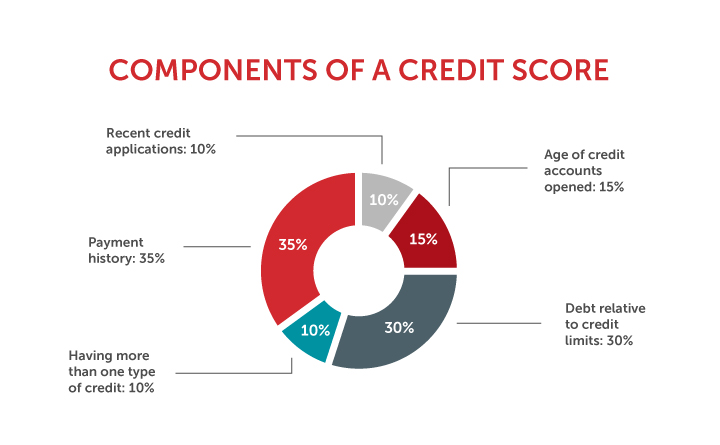

- Payment History (35% of FICO score): This is the big boss. Payin’ your bills on time, every time, is the single best thing you can do. Miss a payment, and your score takes a nosedive.

- Credit Utilization (30% of FICO score): This is how much of your available credit you’re usin’. Keep it under 30%—like, if you got a $1,000 limit, don’t owe more than $300. Less is even better.

- Length of Credit History (15%): That’s our buddy credit age. It matters, but not as much as the first two.

- Credit Mix (10%): Havín’ different types of credit—like a card and a car loan—helps a bit.

- New Credit (10%): Openin’ too many new accounts at once can spook lenders. Take it slow.

So, while credit age is a player in the game, it’s more like a supportive teammate than the star quarterback. Focus on payin’ on time and keepin’ your balances low, and the age thing will sorta take care of itself over time.

Can You Actually Improve Your Credit Age?

Now, you might be wonderin’, “Can I make my credit age better?” Well, sorta. You can’t speed up time (wish I could, tho!), but there’s a few tricks to help it along. Here’s what me and my team at MoneyMaverick suggest:

- Don’t Close Old Accounts: Even if you ain’t usin’ that first credit card from college no more, keep it open. Closín’ it shortens your credit history, and that’s a bummer for your age average.

- Become an Authorized User: If you got a parent or a buddy with a super old credit account in great standin’, ask if they can add ya as an authorized user. Their account’s history might give your credit age a lil’ boost. Just make sure they’re responsible—any mess-ups on their end could hurt ya.

- Be Patient: Real talk—credit age grows naturally as you keep accounts open. Just hang tight and don’t do nothin’ crazy like closin’ accounts for no reason.

One thing to watch out for: openin’ a bunch of new accounts at once can drag your average age down, since new accounts got zero history. So, if you’re applyin’ for a new card or loan, space ‘em out a bit.

A Lil’ Story From Yours Truly

Lemme share a quick tale. Back when I was just startin’ out, me and my buddy was clueless about credit. We thought havin’ a credit card was just for emergencies or splurgin’ on pizza. I closed my first card after a year ‘cause I didn’t wanna “deal with it.” Big mistake! My credit age took a hit, and it took years to build back up. If I’d known then what I know now, I woulda kept that sucker open and just let it chill in my wallet. Learn from my goof, y’all—don’t ditch those old accounts.

Common Myths About Credit Age (Let’s Bust ‘Em!)

There’s a lotta nonsense floatin’ around about credit age, and I’m here to set the record straight. Check out these myths and the real deal:

- Myth #1: Credit age is the most important thing for your score.

Nah, fam. Like I said earlier, payment history and how much credit you’re usin’ matter way more. Credit age is just one piece of the puzzle. - Myth #2: You can’t get a good score if you’re young.

Not true! Even with a short credit age, you can rock a solid score by payin’ on time and keepin’ balances low. It’s tougher to hit super high numbers like 800, but “good” is totally doable. - Myth #3: Closín’ an old account don’t hurt ya.

Wrong-o! Closín’ old accounts can shrink your credit history and lower that average age. Keep ‘em open unless there’s a crazy fee or somethin’.

How to Check Your Own Credit Age

Curious about where you stand? It’s pretty easy to figure out your credit age, tho you might need to do a lil’ math. Here’s how we do it at MoneyMaverick:

- Pull Your Credit Report: Get a free report from one of the big credit bureaus (there’s three of ‘em, ya know). It’ll list all your accounts and when they were opened.

- List the Ages: For each account, note how long it’s been open. If a card was opened in 2018 and it’s 2023, that’s 5 years.

- Find the Average: Add up the ages of all accounts and divide by the number of accounts. That’s your credit age.

- Check Your Score: See how your score compares to averages for your age group. If it’s in the 680-690 range or higher, you’re likely golden.

Don’t stress if your credit age seems low. Remember, it’s just one factor, and time will naturally bump it up as long as you play your cards right.

Tips to Build a Stellar Credit History (Beyond Just Age)

Since credit age works hand-in-hand with other stuff, let’s talk about buildin’ a rock-solid credit profile. I’ve been down this road, and these tips have saved my bacon more than once:

- Pay On Time, Every Time: I can’t stress this enough. Set up auto-payments if you gotta. Late payments are like kryptonite to your score.

- Keep Balances Low: Don’t max out your cards. Aim to use less than 30% of your limit. Got a $2,000 limit? Keep the balance under $600.

- Mix It Up (Slowly): Over time, havin’ different kinds of credit—like a card, a car loan, or a mortgage—can help. But don’t rush to open new stuff just for variety.

- Check Your Report: Peek at your credit report now and then to catch errors. Wrong info can drag ya down, and disputin’ it is free.

- Avoid Too Many Applications: Each time you apply for credit, it can ding your score a lil’. Only apply when you really need somethin’.

Stick to these habits, and your credit age will grow into a nice, mature number without you even tryin’ too hard.

What If Your Credit Age Is Low? Don’t Panic!

If you’re just startin’ out or had to close accounts for whatever reason, a low credit age don’t mean you’re doomed. Focus on what you can control. Pay every bill on time, keep your credit use low, and avoid openin’ a ton of new accounts. Over the months and years, your credit age will climb, and so will your score.

One sneaky move I’ve seen work is gettin’ added as an authorized user on someone else’s old account, like I mentioned before. My cousin did this with his mom’s credit card—she’s had it forever—and it gave his credit age a nice lil’ nudge. Just make sure the main account holder is solid with their payments, or it could backfire.

Wrappin’ It Up: Your Credit Age Journey

So, there ya have it, peeps! A “good” credit age ain’t just a magic number—it’s about how long you’ve been in the credit game compared to your life stage, and how you’ve managed it. Whether you’ve got a couple years or a couple decades of credit history, the real key is keepin’ accounts open, payin’ on time, and usin’ credit smartly. At MoneyMaverick, we’re rootin’ for ya to build that score into somethin’ you can brag about.

Got a credit age story or a question? Drop it in the comments below. I’m all ears! And hey, stick around our blog for more no-nonsense tips on makin’ your money work for you. Let’s keep this financial journey rollin’ together!

Length of credit history vs. credit age

The “length of credit history” means how long any given account has been reported open, says Rod Griffin, senior director of public education and advocacy for Experian, one of the three major credit bureaus.

“Generally, the longer an account has been open and active, the better it is for the credit score,” Griffin says. “That’s particularly true for an account with a positive payment history that has no delinquency.”

The credit scoring algorithms calculate the average of how long all your accounts have been open. That average age of accounts is your “credit age.”

It’s all but impossible to get a score higher than 800 if you’re young, because your credit age likely will be low.

What is a GOOD Credit Score in 2025? What’s the Average Credit Score Overall & By Age / Generation?

FAQ

What is a good credit age average?

Is 3 years of credit history good?

Building a good length of credit history takes time, and while 3 years and 10 months is a solid start, most lenders consider 5 to 8 years as the “good” range for credit history. Anything above 8 years typically falls into the “excellent” category.

What credit should a 25 year old have?

As of my last update, the average credit score for individuals aged 20 to 25 typically falls in the range of 630 to 680. This range can vary based on factors like geographic location, economic conditions, and individual financial behavior. Young adults often have shorter credit histories, which can impact their scores.

Can a 20 year old have a 700 credit score?

While someone who is 20 years old probably has a relatively short credit history, it is possible to have a score of 700.Jan 9, 2025

How much does credit age affect your credit score?

Your credit age accounts for 15% of your credit score. Apply for credit early, and keep your accounts open as long as you can. Length or age of credit history is how long you’ve had credit lines in your name. It accounts for about 15% of your credit score, and there’s not much you can do except be patient to help this factor improve.

What does credit age mean?

Credit age measures the length of your credit history. In other words, how long you’ve been using different types of credit, including: For individual credit accounts, credit age measures the length of time they’ve been open. What Is a Thin Credit File? Is 700 a Good Credit Score?

What is a good credit score if you’re young?

That average age of accounts is your “credit age.” It’s all but impossible to get a score higher than 800 if you’re young, because your credit age likely will be low. While credit age matters for credit scoring purposes, the only thing you can do about it is to keep your credit accounts in good standing and avoid closing credit cards unnecessarily.

What percentage of credit score is based on age?

When it comes to credit scores, the importance of credit age depends on the scoring model. Credit-scoring company FICO® says credit age accounts for 15% of its credit scores. VantageScore® says it accounts for 20%-21% of its latest credit scores. Join the millions using CreditWise from Capital One. What is length of credit history?

What is the average age of credit?

This is simply the average age of all of your accounts as measured using the same date opened field. For example, if you have two accounts that are 3 years old and 5 years old, your average age of credit is 4 years. Because items can age off your credit report, credit age can change.

Is there a perfect credit age?

Broadly speaking, the longer you’ve had an account open the better. But there’s no perfect credit age. Improving your length of credit can take time. If you’re trying to establish credit, secured credit cards and credit-builder loans are two options. Becoming an authorized user is another.