“Expert verified” means that our Financial Review Board thoroughly evaluated the article for accuracy and clarity. The Review Board comprises a panel of financial experts whose objective is to ensure that our content is always objective and balanced.

Bankrate is always editorially independent. While we adhere to strict , this post may contain references to products from our partners. Heres an explanation for . Our is to ensure everything we publish is objective, accurate and trustworthy. Bankrate logo

Founded in 1976, Bankrate has a long track record of helping people make smart financial choices. We’ve maintained this reputation for over four decades by demystifying the financial decision-making process and giving people confidence in which actions to take next.

Bankrate follows a strict editorial policy, so you can trust that we’re putting your interests first. All of our content is authored by highly qualified professionals and edited by subject matter experts, who ensure everything we publish is objective, accurate and trustworthy.

Our mortgage reporters and editors focus on the points consumers care about most — the latest rates, the best lenders, navigating the homebuying process, refinancing your mortgage and more — so you can feel confident when you make decisions as a homebuyer and a homeowner. Bankrate logo

Bankrate follows a strict editorial policy, so you can trust that we’re putting your interests first. Our award-winning editors and reporters create honest and accurate content to help you make the right financial decisions.

We value your trust. Our mission is to provide readers with accurate and unbiased information, and we have editorial standards in place to ensure that happens. Our editors and reporters thoroughly fact-check editorial content to ensure the information you’re reading is accurate. We maintain a firewall between our advertisers and our editorial team. Our editorial team does not receive direct compensation from our advertisers.

Bankrate’s editorial team writes on behalf of YOU – the reader. Our goal is to give you the best advice to help you make smart personal finance decisions. We follow strict guidelines to ensure that our editorial content is not influenced by advertisers. Our editorial team receives no direct compensation from advertisers, and our content is thoroughly fact-checked to ensure accuracy. So, whether you’re reading an article or a review, you can trust that you’re getting credible and dependable information. Bankrate logo

Hey there, congrats if you’re even thinkin’ about paying off your mortgage! That’s a huge freakin’ deal, and I’m stoked to chat about what comes next. One big question folks got is, “What happens to escrow when mortgage is paid off?” If you’re scratchin’ your head about escrow in the first place, don’t worry—I gotchu. We’re gonna break this down real simple, step by step, so you know exactly what to expect when that last mortgage payment clears. At our lil’ blog here, we’re all about keepin’ it real and makin’ sure you’re set for success, so let’s dive right in!

What Even Is an Escrow Account? Let’s Get the Basics Down

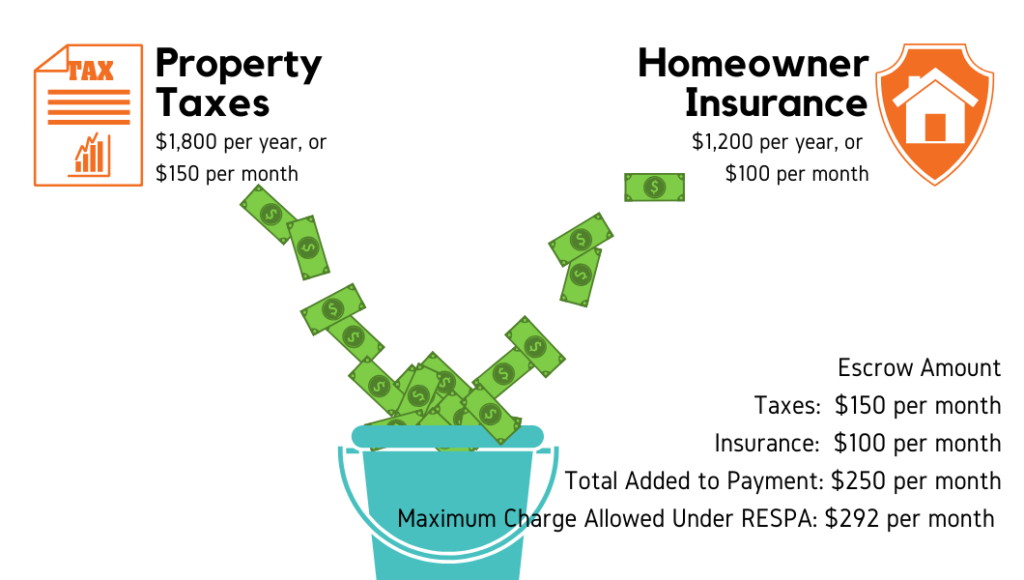

Before we get to the juicy part, let’s make sure we’re on the same page about what escrow is Think of an escrow account like a piggy bank your lender holds for you Every month, when you pay your mortgage, a chunk of that cash goes into this account. It ain’t for them to spend on fancy vacations—it’s to cover your property taxes and homeowners insurance.

Why do they do this? Well, it’s kinda like a safety net. Lenders wanna make sure those big bills get paid on time, ‘cause if you don’t pay taxes, the government could slap a lien on your house, and that’s a mess for everyone. Same with insurance—if your place burns down and you ain’t covered, they’re outta luck too. So, they collect a lil’ bit each month, stash it in escrow, and pay those bills for you when they’re due.

But here’s the kicker: once your mortgage is paid off, the game changes. You’re no longer tied to that lender, so what happens to this piggy bank? Let’s unpack that next.

The Big Moment: What Happens to Escrow When Your Mortgage Is Paid Off?

Alright, you’ve made that final payment. Pop the champagne, ‘cause you own your home free and clear! But what’s the deal with your escrow account now? Here’s the straight-up answer: once your mortgage is paid in full, that escrow account gets closed. Done. Finito. Your lender ain’t managing it no more, ‘cause they ain’t got a stake in your property anymore.

Now, here’s the part you’ll wanna hear—any money left in that escrow account comes back to you. Yup, you heard that right! If there’s leftover cash after all the taxes and insurance bills are settled, your lender is legally required to refund it. Most times, they gotta send you that money within 20 days of closing the account. Some say it could stretch to 30 days, dependin’ on the rules, but either way, it’s comin’ your way. You don’t even gotta beg for it—they’ll send a check or direct deposit automatically.

But hold up, it ain’t all just free money and high fives. There’s a catch: with the escrow account gone, you’re now 100% responsible for payin’ your own property taxes and homeowners insurance. No more middleman. That’s a big shift, and we’ll get into how to handle it in a sec. For now, just know the escrow account closes, you get any leftovers, and the responsibility is all yours.

How Much Will You Get Back? And When?

So, you’re probly wondering, “How much dough am I gettin’ back from this escrow thing?” Truth is, it depends. The refund amount hinges on what’s left in the account at the time you pay off your mortgage. If your taxes and insurance were paid up recently, there might be a decent chunk waitin’ for ya. But if a big tax bill just got paid outta that account, it might be slim pickins.

Here’s a quick breakdown of the timeline and what affects your refund:

- Timeline for Refund: By law, your lender gotta return any remaining escrow funds within 20 days after the mortgage is paid off. Some might drag their feet a tad longer, but 20 days is the standard.

- What Impacts the Amount: It’s all about timing. If your property taxes or insurance premiums went up or down recently, that changes what’s left. Also, if you overpaid into escrow over the years, you might see a bigger refund.

- How You Get It: Most lenders will mail a check or do a direct deposit. You don’t gotta do nothin’ to claim it—just keep an eye on your bank account or mailbox.

If you don’t see that refund after a month don’t just sit there—give your lender a call. Mistakes happen and I ain’t trustin’ nobody to just “figure it out” without a lil’ nudge from me.

Your New Responsibilities: Taxes and Insurance Ain’t Goin’ Nowhere

Now that the escrow account is kaput, it’s on you to handle the bills it used to cover. This is where a lotta folks trip up so pay attention. You gotta pay your property taxes directly to your local government now. Dependin’ on where you live that might mean one big yearly bill or a buncha smaller ones from different places like your city, county, or even school district.

Same goes for homeowners insurance. While you ain’t legally required to keep it once the mortgage is gone, you’d be nuts not to. It protects your house, your stuff, and even covers your butt if someone gets hurt on your property. You’ll need to contact your insurance company and make sure they know to bill you direct now—no more lender in the middle.

Here’s a quick checklist to keep things straight:

- Reach Out to Your Tax Office: Make sure they’re sendin’ bills to you, not your old lender. Hit up your local clerk’s office if you ain’t sure who to talk to.

- Update Your Insurance: Tell your insurance folks to remove the lender from your policy. Set up direct payments so you don’t miss a beat.

- Set Aside Cash: Without escrow, them big bills can sneak up. Stash some money each month so you ain’t scramblin’ when taxes are due.

I’ll be real with ya—I forgot to update my tax billing info once after a refinance, and it was a headache gettin’ it sorted. Learn from my dumb mistake and get this locked down quick.

What Should You Do with That Escrow Refund? Some Ideas

Alright, let’s say you got that sweet escrow refund check in hand. What now? It ain’t a fortune usually, but it’s still extra cash you can put to work. Here at our blog, we’re all about makin’ smart moves, so here’s a few ideas to chew on:

- Save It for Taxes and Insurance: This is the safe bet. Toss that refund into a separate savings account and use it for your next property tax or insurance bill. It’s like givin’ yourself a head start.

- Pay Down Other Debt: Got credit card bills or a car loan weighin’ ya down? Use this cash to knock off some of that high-interest junk. You’ll save more in the long run.

- Invest It for Growth: If you’re feelin’ frisky, throw it into somethin’ like a high-yield savings account or even a lil’ stock action. Just don’t gamble what you can’t afford to lose.

- Treat Yoself (Just a Lil’): Hey, you paid off a whole dang mortgage! Maybe take a small slice of that refund for a nice dinner or a weekend trip. You earned it, fam.

I remember gettin’ a small refund like this back in the day, and I used it to fix up a leaky gutter. Felt good knowin’ my house was tighter ‘cause of that lil’ bonus. Whatever you pick, just make sure it fits your big-picture goals.

Any Pitfalls to Watch Out For? You Bet!

Payin’ off your mortgage is awesome, but there’s a couple gotchas when it comes to escrow closin’ out. I ain’t tryin’ to scare ya, just keepin’ it 100. Here’s what to watch for:

- Missin’ the Refund: Some lenders mess up and don’t send your escrow refund on time. If it’s been over a month, get on the phone and raise hell ‘til it’s sorted.

- Forgetting Tax Payments: Without escrow, it’s easy to forget a tax bill ‘til it’s late. Set reminders or auto-payments if your local office allows it.

- Insurance Lapse: If you don’t update your insurance billing, you might miss a payment and lose coverage. That’s a disaster waitin’ to happen if a storm hits.

I’ve seen buddies get hit with late fees ‘cause they didn’t realize their tax bill wasn’t bein’ handled no more. Don’t let that be you—stay on top of this stuff!

A Lil’ Table to Keep Timelines Straight

Just to make this crystal clear, here’s a quick table with the key timelines around escrow after payoff. Keep this handy for reference:

| Action | Timeline | Who Handles It? |

|---|---|---|

| Escrow Account Closure | Upon mortgage payoff | Lender/Servicer |

| Refund of Remaining Escrow Funds | Within 20-30 days | Lender/Servicer |

| Update Tax Billing Info | ASAP after payoff | You (Homeowner) |

| Update Insurance Billing | ASAP after payoff | You (Homeowner) |

This lil’ chart is your cheat sheet. Pin it somewhere if you’re close to payin’ off that mortgage!

How Does This Affect Other Stuff? Like Credit or Equity?

You might be wonderin’ if closin’ out escrow and payin’ off your mortgage messes with other parts of your finances. Let’s touch on a couple quick things. First, your credit score. Payin’ off a mortgage don’t usually tank your score, but it might dip a tiny bit ‘cause you’re losin’ a long-term account from your credit mix. On the flip side, havin’ less debt can boost it. Check your credit report after a month or two to make sure it shows the mortgage as closed.

Second, your home equity. With the mortgage gone, you got 100% equity in your crib. That means if you need cash down the road, you can tap into it with somethin’ like a home equity loan or line of credit. It’s a powerful tool, but don’t go borrowin’ just ‘cause you can—be smart about it.

And taxes? One last thing—payin’ off your mortgage means you can’t deduct mortgage interest on your tax return no more. That might bump up what you owe come tax season, so chat with an accountant to see how it shakes out for ya.

Why This Matters to Me (And Should to You)

Look, I gotta be straight with ya—payin’ off a mortgage is one of them life moments that feels like you’ve climbed a dang mountain. But figurin’ out stuff like escrow after the fact? That’s the kinda thing that can trip you up if you ain’t ready. I’ve been through financial headaches myself, and I hate seein’ good folks stressed over somethin’ that’s easy to fix with the right know-how.

That’s why we’re breakin’ this down here at our blog. We wanna make sure you’re celebratin’ your big win without a buncha “what ifs” hangin’ over your head. Escrow might seem like a small piece of the puzzle, but gettin’ it wrong can mean late fees, lapsed insurance, or worse. So take this as your roadmap to keep rollin’ smooth.

Wrappin’ It Up: You Got This!

So, let’s recap the big question: what happens to escrow when your mortgage is paid off? It’s simple—the account closes, you get back any leftover funds within about 20 days, and you take over payin’ your own taxes and insurance. It’s a shift, sure, but it’s also a chance to take full control of your homeownership game.

Make sure you update your billing info with the tax folks and insurance peeps right away. Use that refund wisely, whether it’s savin’ for future bills or knockin’ out other debt. And keep an eye out for any hiccups—don’t let a late refund or forgotten tax bill rain on your parade.

We’re rootin’ for ya here at the blog. If you got questions or wanna share how you handled your escrow refund, drop a comment below. Let’s keep this convo goin’! And hey, if you’re close to payin’ off that mortgage, give yourself a pat on the back—you’ve earned it, champ!

Get in touch with your accountant

After paying off your mortgage, you should notify your accountant. You’ll no longer have mortgage interest to deduct on your tax return, which could potentially increase your tax liability.

However, paying off your mortgage might also free up cash that you can use for other purposes. Your accountant or a financial advisor can suggest ways to leverage the money you’re saving. You might use the extra funds to:

What happens when you pay off your mortgage?

Here are a few things you’ll need to do once you’ve paid off your mortgage.

What Happens To Escrow When You Pay Off Your Mortgage? – CountyOffice.org

FAQ

Do I get escrow money back after paying off mortgage?

If you’ve paid off your mortgage in full, the balance in your escrow account should be returned to you within 20 days. If you are still paying into escrow but an escrow analysis (a process conducted every 12 months) has found you’re due money back, you should receive it within 30 days.

What happens when a mortgage is fully paid off?

After your loan is closed, your mortgage servicer will also close your escrow account and return any remaining funds to you. Legally, the servicer must issue your escrow refund within 20 days of closing the account. You will then be responsible for paying your home insurance premiums on your own.

Does homeowners insurance go down when a mortgage is paid off?

Can I keep an escrow account without a mortgage?