When you apply for a credit card, loan, or other financial product from Chase Bank, one of the key factors they consider is your credit score. Specifically, Chase uses FICO credit scores to evaluate applicants. But what exactly is a FICO score and why does it matter so much?

In this article, we’ll take a close look at FICO scoring and explain what credit score ranges Chase looks for when making lending decisions. We’ll also provide tips on how to check and improve your FICO score.

What is a FICO Score?

FICO is an acronym for the Fair Isaac Corporation, the company that created the FICO credit scoring model back in 1989. Since then, FICO has become the industry standard score used by 90% of top lenders, including major banks like Chase, when evaluating credit risk.

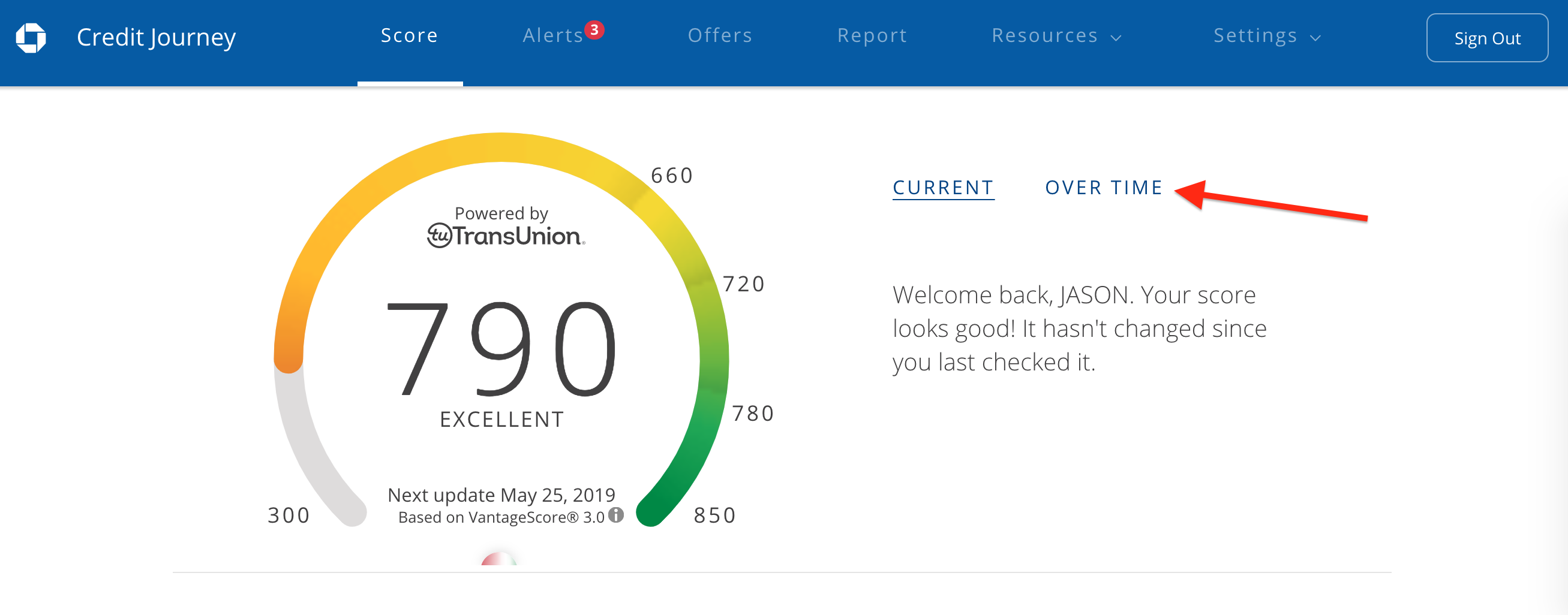

Your FICO score is a three-digit number ranging from 300 to 850 that summarizes your creditworthiness. The higher the score, the lower the perceived risk that you will default on a loan or credit obligation. FICO scores take into account factors like:

- Payment history – Do you pay your bills on time? Late payments can negatively impact your score.

- Amounts owed – How much do you owe on loans and credit cards compared to your credit limits? High balances hurt your score.

- Length of credit history – How long have you been using credit? A longer history helps your score.

- Credit mix – Do you have experience with different types of credit (credit cards, loans, etc.)? Broad experience helps.

- New credit – Opening many new accounts in a short period can negatively impact your score.

FICO uses a proprietary algorithm and mathematical model to calculate your score based on information in your credit reports from the three major credit bureaus (Experian, Equifax, and TransUnion).

Scores are recalculated whenever your credit report data changes, so your FICO score fluctuates over time as your financial profile evolves

FICO Score Ranges

Not all FICO scores are created equal. There are actually 28 different FICO score versions tailored for specific credit products and lenders. However, most fall in the range of 300-850.

Here is how the scale breaks down:

- 800-850 = Exceptional

- 740-799 = Very Good

- 670-739 = Good

- 580-669 = Fair

- Below 579 = Very Poor

In general, you want your score to be over 700 to get approved for credit at favorable rates. The higher the better!

What FICO Scores Does Chase Use?

Chase evaluates applicants based on their FICO 8 scores from Experian and TransUnion.

FICO 8 is a widely used base model introduced in 2009 It weights recent credit patterns more heavily than older FICO versions

For credit cards and personal loans, Chase generally looks for applicants to have FICO 8 scores of 670 or higher for approval. The higher your score, the more likely you’ll be approved and offered better terms like lower interest rates.

For mortgages and home equity products, Chase may use older FICO models that are more conservative, like FICO 2 or 4. They tend to want scores of at least 720 for mortgage approvals.

Auto loans also use industry-specific FICO Auto Score versions tailored to predict repayment risk. Chase typically looks for a minimum FICO Auto Score of 700.

The exact minimum scores vary based on the specific credit product, your income, debt levels, and other variables. But in most cases, Chase looks for applicants to have good to excellent credit.

How to Check Your FICO Score

Since Chase uses FICO scores in their lending decisions, it’s important to monitor your own FICO 8 scores from Experian and TransUnion. Here are some options:

-

Check your credit card statement – Many issuers like Chase provide free FICO scores on monthly statements.

-

Use free FICO score services – Sites like Credit Karma offer free estimates, but they use a different scoring model called VantageScore.

-

Buy scores from myFICO.com – This provides your real FICO scores used by lenders. Costs start at $19.95/month.

-

Get free reports at AnnualCreditReport.com – Federal law allows you to access your Equifax, Experian, and TransUnion reports for free once a year. But they do not include FICO scores.

Checking your own credit report does not negatively impact your scores. In fact, regular monitoring is wise to catch any errors or suspicious activity.

Tips for Improving Your FICO Scores

If your FICO scores fall below Chase’s approval thresholds, here are some tips to improve them over time:

-

Pay all bills on time – Payment history has the biggest impact on your scores. Set up autopay or reminders to avoid late payments.

-

Keep balances low – High utilization hurts, so pay off cards in full each month when possible.

-

Limit new credit – Too many new accounts can lower scores temporarily. Space out new applications over time.

-

Check for errors – Incorrect data like closed accounts listed as open can damage scores. Dispute any errors.

-

Build healthy mix – Using different credit types responsibly demonstrates lower risk.

-

Give it time – FICO scores reflect historical data. Building credit takes patience as you develop a positive track record over years.

With responsible credit use and financial habits, your FICO scores will gradually improve. Just be sure to check your real FICO scores, not just credit monitoring estimates, so you know where you stand with Chase and other lenders.

The Takeaway

-

Chase uses your FICO credit scores, specifically FICO 8 based on Experian and TransUnion data, when deciding whether to approve you for credit cards, loans, mortgages and other products.

-

They generally look for FICO scores of 670+ for credit cards and personal loans, and 720+ for mortgages. Auto loans use FICO Auto Scores.

-

Checking and monitoring your real FICO scores from myFICO.com allows you to see the same information Chase evaluates.

-

Paying bills on time, lowering balances, limiting new credit, fixing errors, and building a healthy credit mix can help improve your FICO scores over time.

Knowing your credit score empowers you to take steps to strengthen your credit profile and maximize approval odds for Chase and other lenders down the road.

What happens if you get rejected?

You will automatically be rejected for this card if any of the below cases apply to you:

- You currently have a Chase Sapphire Reserve® or Chase Sapphire Preferred® Card, regardless of whether you previously received the bonus.

- You previously had a Chase Sapphire Reserve® or Chase Sapphire Preferred® Card and received the bonus within the past 48 months.

If you dont get accepted for the card, issuers and banks are required by federal law to let applicants know why theyve been rejected for a line of credit, and you should be informed within 60 days.

It is possible to contest the rejection by calling Chase. If youre a current customer, you could point to your longtime relationship with the issuer and if possible, your history of on-time payments.

You may also be able to sign up for the card by being a current Chase customer, calling the issuer and requesting a product change, although this means you will not be eligible for the welcome bonus.

What credit score should you aim for?

First off, most credit card issuers will look at your FICO credit score in order to determine your eligibility for a new card. FICO scores range from 300 to 850, with higher scores indicating a higher likelihood that youll be able to pay off your balance on time and in full.

- Very poor: 300 to 579

- Fair: 580 to 669

- Good: 670 to 739

- Very good: 740 to 799

- Exceptional: 800 to 850

Generally, youll need to have a credit score of at least 700 in order to qualify for the Chase Sapphire Preferred® Card. It is possible for you to qualify with a lower score — or even be rejected with a higher score — but to improve your odds of being approved, aim to have a score above 700.

To maintain a good credit score, youll need to make your payments on time, keep a low credit utilization ratio and have a long credit history. Heres how each category contributes to your overall credit score.

- Payment history (35%) — If youve made your previous payments on time

- Amounts owed (30%) — Your credit utilization ratio, or the ratio of the amount of credit youre using to the amount thats been extended and owed on your accounts

- Length of credit history (15%) — The amount of time youve had credit

- New credit (10%) — How often you open new accounts

- Credit mix (10%) — Whether you have different types of credit, such as installment loans or revolving lines of credit

You could also benefit from signing up for a service such as *Experian Boost®, which uses your on-time payments for select subscription services and utilities to calculate your credit score.

-

Cost

Free

-

Average credit score increase

13 points, though results vary

-

Credit report affected

Experian®

-

Credit scoring model used

Results will vary. See website for details.

How to sign up for Experian Boost:

- Connect the bank account(s) you use to pay your bills

- Choose and verify the positive payment data you want added to your Experian credit file

- Receive an updated FICO® Score

Learn more about eligible payments and how Experian Boost works.

Credit card issuers do, however, look at factors besides your credit score, such as your annual income, how long youve had credit and how many credit cards youve applied for recently.

For example, Chase is known for its strict 5/24 rule, which means Chase credit card applicants wont be approved for a new card if theyve opened five or more personal credit cards within the past 24 months. Note that this rule applies to all credit cards, not just the ones offered by Chase.

Another factor issuers consider is the length of your credit history. When I first applied for the Chase Sapphire Preferred, I was rejected immediately even though I had a FICO credit score above 700 (I had been an authorized user on my parents card) since I didnt have any credit history of my own. Generally, the Chase Sapphire Preferred may not be a good option for a first credit card if youre in a similar situation. If you have a lower credit score, consider first looking at cards for those with no credit, bad credit, or fair or average credit.

What FICO Score Does Chase Use For Credit Cards? – CreditGuide360.com

FAQ

Which FICO score does Chase use?

What FICO score do you need for Chase Preferred?

We recommend having a FICO score of at least 690 before applying for this card.

Do banks use FICO 8 or 9?

According to the Fair Isaac Corporation, FICO Score 8 is still the most widely used version of the FICO score, and FICO Score 9 is also still widely used by lenders, even though both models have been available for over a decade.

How rare is a 780 credit score?