Disclosure: This post contains affiliate links, which means we receive a commission if you click a link and purchase something that we have recommended. Please check out our disclosure policy for more details.

Your credit score can open the door to helping you achieve many of your financial goals, like buying a house, renting an apartment at your desired location, or even getting approved for a credit card that allows you to earn free travel rewards. When it comes to accessing these different financial products, lenders look at your credit score as one of many factors when determining eligibility.

Learning about FICO® Scores will help you to understand how lenders view your creditworthiness and in what ways you can improve it to increase your odds of a loan or credit approval.

Getting a mortgage is an exciting yet complicated process With so many moving parts, it can be confusing to understand which credit model mortgage lenders like Rocket Mortgage use to evaluate borrowers This comprehensive guide will clarify the credit scoring system used by Rocket Mortgage to assess your mortgage eligibility.

An Overview of Credit Scoring Models

Before diving into Rocket Mortgage’s specific credit model let’s quickly go over the major credit scoring systems in use today

-

FICO Scores: Developed by the Fair Isaac Corporation, FICO Scores are the most widely used credit scores by lenders. They range from 300 to 850.

-

VantageScore: Created by the three major credit bureaus, VantageScore also ranges from 300 to 850. Though not as widely used as FICO, it has gained traction in recent years.

-

Educational Credit Management Corporation (ECMC) Score A lesser known scoring model used by some specialty lenders It ranges from 501 to 990

Rocket Mortgage and FICO Scores

When it comes to mortgages, Rocket Mortgage primarily relies on FICO Scores to evaluate a borrower’s creditworthiness. Let’s explore this further:

-

Why FICO? FICO Scores are the industry standard for mortgage lending decisions. Since the vast majority of lenders use FICO Scores, it makes sense for Rocket Mortgage to align with this norm.

-

Which FICO model? Rocket Mortgage specifically looks at FICO Score 2 (from Experian), FICO Score 4 (from TransUnion), and FICO Score 5 (from Equifax).

-

Why these models? They represent the scoring models used by the three major credit bureaus. Each bureau has customized the score to leverage their unique credit data.

How Rocket Mortgage Uses FICO Scores

Now that we know which FICO models Rocket Mortgage uses, let’s look at how they use them:

-

Pulling credit reports: During the mortgage application process, Rocket Mortgage will pull your credit reports from Experian, TransUnion, and Equifax.

-

Obtaining FICO scores: Based on the data in these reports, your FICO Score 2, 4, and 5 will be calculated.

-

Evaluating middle score: Rocket Mortgage takes the median of the three FICO scores as an evaluation of your creditworthiness.

-

Comparing joint applicants: For joint applicants, they will look at the lower median FICO score of the two people applying.

-

Meeting minimums: There are general credit score minimums to qualify for Rocket Mortgage products. For example, 620 for conventional loans. Specific programs may have different thresholds.

Why Your FICO Score Matters

You may be wondering, why does your FICO score matter so much in the mortgage process? Here are some key reasons:

-

Mortgage eligibility: Your FICO score is a major factor determining whether you qualify for a mortgage in the first place.

-

Loan terms: Higher FICO scores generally lead to better interest rates and overall loan terms. Every point matters!

-

Underwriting: Your creditworthiness affects many aspects of underwriting, including required down payment and loan amount.

-

Automated processes: Many lenders use automated underwriting software which incorporates FICO scores.

Beyond The FICO Score

While your FICO score is important, it does not tell your whole financial story. Rocket Mortgage looks at other aspects too:

-

Income history: Verifying your income provides insight into your ability to make payments.

-

Debt-to-income ratio: This measures how much of your income goes to debt payments. Lower is better.

-

Down payment: Your down payment percentage can affect mortgage eligibility.

-

Employment history: Steady employment makes you appear low risk.

-

Assets & reserves: Liquidity like savings accounts and retirement funds are viewed positively.

Frequently Asked Questions

Which credit bureau does Rocket Mortgage use?

Rocket Mortgage will pull credit reports from all three major bureaus: Experian, TransUnion, and Equifax.

What FICO scores are required for approval?

Requirements vary by product, but generally you need FICO scores of at least 620. Some specialized programs accept lower scores.

What if my three FICO scores are very different?

Rocket Mortgage will take the middle score of the three as a benchmark for evaluating your credit.

Does Rocket Mortgage use other credit models?

Primarily FICO, which is industry standard. Less commonly used models like VantageScore are not a focus.

Can I still get approved with no credit history?

Yes, through specialized mortgage programs. Manual underwriting and alternative credit data may be used.

The Bottom Line

Understanding that Rocket Mortgage relies on your FICO Scores, specifically versions 2, 4, and 5 from the three credit bureaus, can help you take proactive steps to ensure your credit profile is mortgage-ready. Checking your scores, disputing errors, and maintaining healthy credit habits are key. While credit counts, also remember Rocket Mortgage takes a holistic look at your finances during underwriting. With preparation and insight into the credit model used, you can feel confident embarking on your home buying journey with Rocket Mortgage!

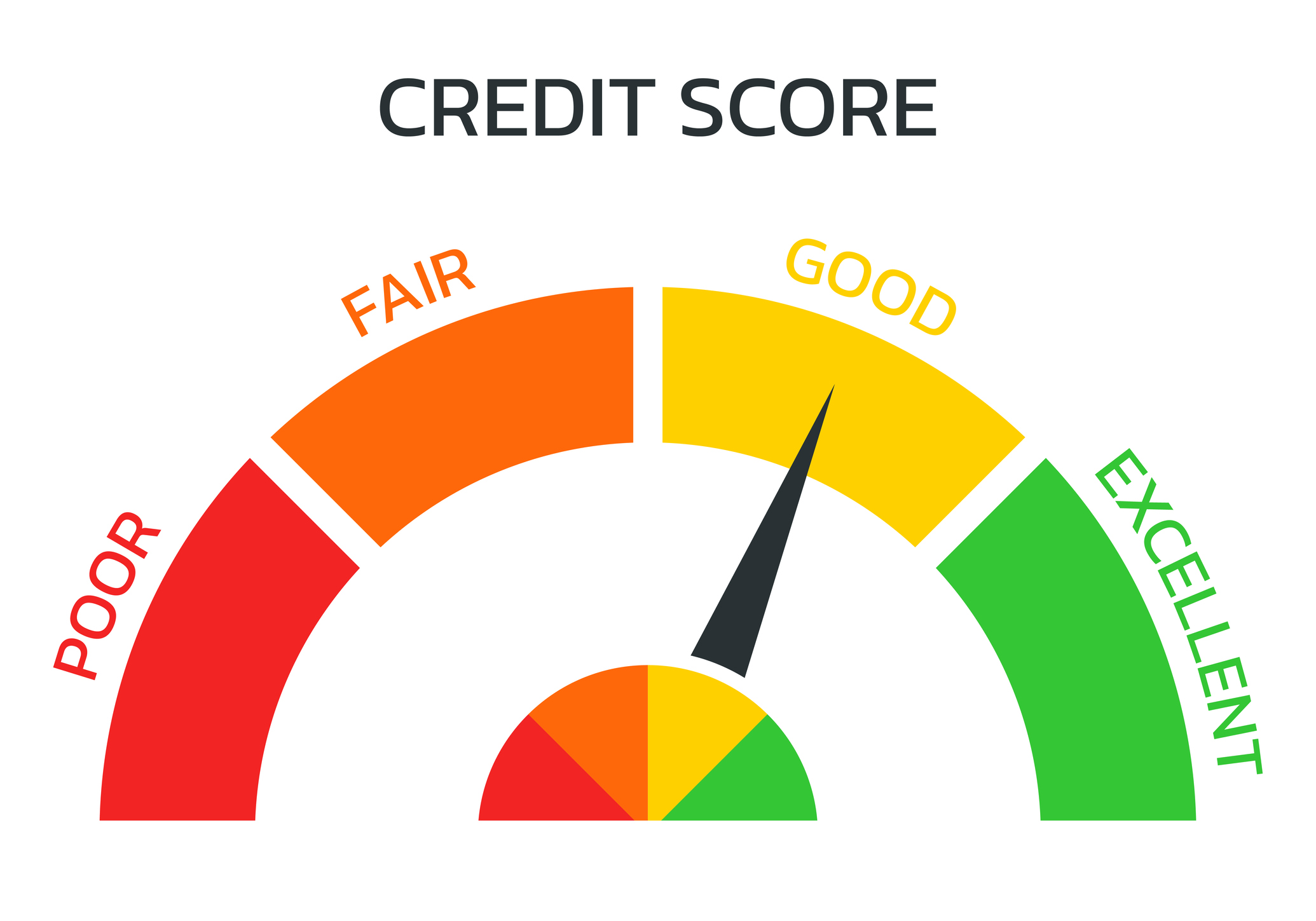

What Is A Good FICO® Score?

The higher your score, the less of a risk you pose to lenders. A higher score usually also indicates a positive credit history. For example, it could mean you’re more likely to pay back your loans on time and that you are mindful of how much of your credit limit you use.

In many cases, lenders consider a 670 FICO® credit score or higher a good score. The highest credit score possible you can get is 850.

The following table shows the breakdown of FICO® credit scores.

|

Poor |

Fair |

Good |

Very Good |

Exceptional |

|

Below 580 |

580 – 669 |

670 – 739 |

740 – 799 |

800 and above |

How do I get a better FICO® Score?

You can try to boost your credit score by using any of these suggestions:

- Checking your credit reports from all three credit bureaus and reporting any errors you find

- Work on paying your loans and credit cards bills on time and at least the minimum required amount

- Hold off applying for any new credit until you really need to

- Monitor your credit cards and lines of credit to make sure you’re not using too much of your credit limit