According to the Government of Canada, a credit score is a 3-digit number that represents how likely a credit bureau thinks you are to pay your bills on time.1 It can be an important part of building your financial confidence and security.1 For example, building a good credit score could help you get approved for loans and larger purchases, like a home.1 You may also be able to access more competitive interest rates.1

There are two main credit bureaus in Canada: Equifax and TransUnion.1 These are private companies that keep track of how you use your credit.1 They assess public records and information from lenders like banks, collection agencies and credit card issuers to determine your credit score.1

Your credit score is one of the most important numbers in your financial life. It impacts everything from whether you can get approved for new credit cards and loans to the interest rates and fees you’ll pay So when you check your credit score and see that it’s 731, you probably have some questions Is 731 a good credit score? How can you raise or maintain your score? This article will explain what a credit score of 731 means and how you can make the most of it.

What Does a Credit Score of 731 Mean?

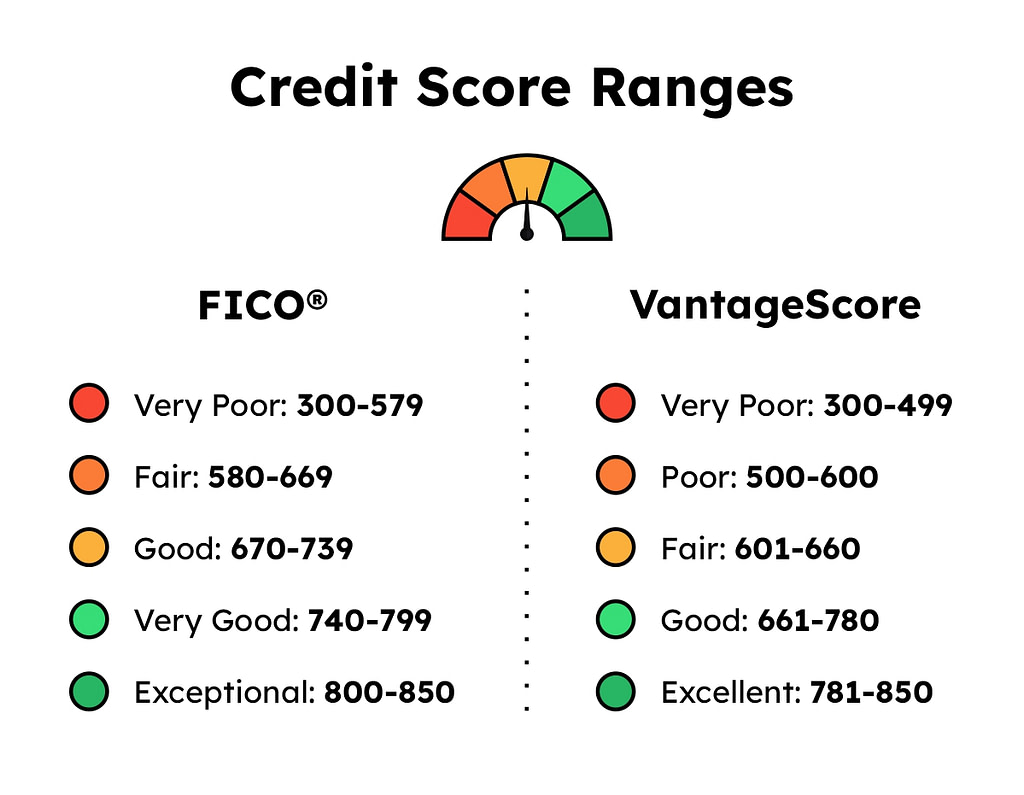

First, some background on credit scores. The most commonly used credit scores come from FICO and range from 300 to 850. According to Experian, a 731 FICO score is in the “good” credit range, which is 670-739. This means lenders view you as an acceptable borrower who is likely to repay debts, but you may not get the very best terms.

Specifically a FICO score of 731 means

-

You have higher odds of approval for credit cards and loans compared to those with lower scores.

-

You may qualify for competitive interest rates, but likely not the absolute lowest rates.

-

21% of consumers have credit scores in the good range of 670-739.

-

45% of people have credit scores below 731.

So while a 731 credit score opens access to mainstream credit, there’s still room for improvement. Boosting your score into the “very good” (740-799) or “exceptional” (800-850) ranges can save you money through lower interest rates over time.

How Your Credit Score Affects Approval Odds

Your 731 credit score means you have reasonably good chances of approval for different types of credit products:

-

Credit cards – A score of 731 makes you eligible for many rewards cards and potentially 0% intro APR offers, but not ultra-exclusive cards.

-

Personal loans – You can likely qualify for a variety of personal loans including debt consolidation and major purchases.

-

Mortgages – 731 should meet the minimum requirements for most conventional mortgages and government-backed loans like FHA and VA.

-

Auto loans – Your credit score makes you a well-qualified borrower who can shop competitively for auto financing.

While having a 731 credit score is helpful for approval odds, lenders also consider other factors like income, existing debts and assets. Pre-qualification can give you a clearer picture of your approval chances.

How to Raise Your Credit Score from 731

Here are some tips to improve your credit score from the good range into the very good or exceptional categories:

-

Lower credit utilization – Keep balances below 30% of your credit limits on each card and across all cards.

-

Pay bills on time – Payment history is the biggest factor in your score. Avoid late payments.

-

Limit hard inquiries – Each application causes a hard inquiry that can temporarily drop your score. Apply conservatively.

-

Increase credit history length – Older accounts strengthen your score, so keep your oldest cards open.

-

Diversify credit mix – Maintain a blend of installment loans and revolving accounts.

-

Check credit reports – Dispute any errors with the credit bureaus to maximize your score.

-

Sign up for credit monitoring – This lets you track your score and get alerts about changes.

With diligent credit management over time, you can likely boost your credit score well over 800. Patience and consistency are key – don’t try to cut corners or rush the process.

Maintaining Good Credit with a 731 Score

A score of 731 puts you in a solid position credit-wise, but you’ll need to practice ongoing good habits to stay there:

-

Make on-time payments – Set up autopay or reminders to avoid missed payments that hurt your score.

-

Keep low balances – High utilization causes your score to drop. Try to report less than 10% on individual cards.

-

Be sparing with hard inquiries – Limit new applications and space them out to control inquiries.

-

Review reports regularly – Verify all information and dispute errors immediately.

-

Have long credit history – Keep your oldest accounts open and active to benefit your score.

-

Mix credit types responsibly – Have a few installment loans along with credit cards, but avoid unnecessary debt.

Sticking to these credit best practices will help preserve your score over the long run. Be especially careful to avoid behaviors like late payments that can quickly drag down your score.

How a 731 Credit Score Compares to Others

Here is how a 731 credit score stacks up against some other common scores:

-

800 – A score of 800 is considered “exceptional” and qualifies you for the most favorable lending terms like ultra-low interest rates.

-

740 – A score of 740 is “very good” and better than 731, with improved access to top rewards cards and loans.

-

720 – A score of 720 is the lower end of “good” credit and may have higher interest rates than 731.

-

680 – A 680 score is “fair” credit and likely needs improvement to access prime borrowing rates.

-

650 – A score of 650 is considered “poor” and may lead to denials or subprime terms from lenders.

As you can see, a 731 credit score puts you in a reasonably competitive position compared to other common scores. While you don’t have perfect credit, you have crossed the important 700 and 740 milestones. Now you can focus on incremental improvements over time to maximize your access to affordable credit. Monitoring your scores and reports will help you track your progress.

How to Check Your Credit Score

Since knowing your credit score is vital, you should check it at least every few months. There are several ways to obtain your latest scores:

-

Get your free credit reports that include scores from AnnualCreditReport.com. You can get one report from each bureau every 12 months.

-

Use a free score service like Credit Karma that provides your VantageScore based on TransUnion and Equifax data.

-

Purchase your FICO score directly from myFICO.com or a credit bureau site for your most up-to-date info.

Checking your credit scores frequently allows you to spot patterns and trends. You’ll see the impact of your credit decisions and can course correct as needed. With a 731 score, monitoring your credit is key to maintaining or elevating your standing.

Take Charge of Your Credit Health

A credit score of 731 clearly gives you options and puts you in a reasonably strong position when applying for credit. You have an opportunity to qualify for top financial products that make your life easier and more affordable. But there’s also room for improvement if you want to achieve elite credit status.

No matter what, the most important thing is to have awareness of where your credit stands today. Get in the habit of checking your credit scores and reports regularly. Understand the key factors that impact your rating. With this knowledge, you can make smart choices that gradually build your credit over time. A score of 731 is respectable, but consistent effort will help maximize your access to credit.

How to maintain your credit score

One way to maintain your credit score is to try to stay within the 35% ratio mentioned above.3 Add up all your credit limits and multiply the total by 35%. That’s the amount you should ideally try to avoid exceeding when borrowing money or using credit.3

Avoid applying for too much credit

There are some downsides to having too many credits cards. You may be tempted to use them and spend more.

According to the federal government, you should also avoid applying for too many loans, having too many credit cards and requesting too many credit checks in a short timeframe.3 That’s because it could negatively impact your credit score too.3

Stay within your credit limit

Avoid going over your credit limit. If you go over your limit, it could lower your credit score.3

Overall, having a good credit score can help boost your financial confidence and security. So, congrats on taking the first step by learning how credit scores work and how you can improve yours!

-

How to make a budget [Video]

Learning how to make and follow a budget is an important step on your journey towards financial confidence.

-

Tips to reduce your spending

Check out our advice for cutting down on your spending to help you save, even during challenging times.

-

Check your credit score

You can check your credit score with the TransUnion CreditView® Dashboard in the TD app. Checking in the TD app will not affect your credit score in any way. Get a free check of your credit score. Learn more

-

TD Debt Consolidation Calculator

Find your debt-freedom date and quickly calculate how soon you can be debt-free. TD Debt Consolidation Calculator Calculate

-

Looking for a credit card?

Use our Credit Card Selector Tool to help you choose. Looking for a credit card? Explore your options

What’s a utilization ratio or debt-to-credit ratio?

According to Equifax, your debt-to-credit ratio, also known as your utilization ratio, is the amount of your debt compared to your credit limit.5 Your debt-to-credit ratio is important because if your ratio is high, it can indicate that you’re a higher-risk borrower.5 That’s because lenders see borrowers who use a lot of their available credit as a greater risk.5

For example, imagine you have a couple of credit cards and a line of credit with a total debt of $14,000 and a combined limit of $20,000. Your debt-to-credit ratio would be 70%.

According to the Government of Canada, a ratio of 35% or below on credit cards, loans and lines of credit is recommended.3

Is 731 A Good Credit Score? – CreditGuide360.com

FAQ

What can I do with a 731 credit score?

A FICO® Score of 731 provides access to a broad array of loans and credit card products, but increasing your score can increase your odds of approval for an even greater number, at more affordable lending terms.

Can you buy a house with a 731 credit score?

More than 40% of first mortgages go to borrowers with credit scores below 740, so you should be able to finance your home purchase without much issue.

How rare is credit score over 800?

What it means to have a credit score of 800. A credit score of 800 means you have an exceptional credit score, according to Experian. According to a report by FICO, only 23% of the scorable population has a credit score of 800 or above.

Can I get a car loan with a 731 credit score?

Key takeaways. There is no minimum credit score required to buy a car, but most lenders have minimum requirements for financing. Most borrowers need a FICO score of at least 661 to get a competitive rate on an auto loan.