A FICO® ScoreÎ of 727 falls within a span of scores, from 670 to 739, that are categorized as Good. The average U.S. FICO® Score, 714, falls within the Good range. A large number of U.S. lenders consider consumers with Good FICO® Scores “acceptable” borrowers, which means they consider you eligible for a broad variety of credit products, although they may not charge you the lowest-available interest rates or extend you their most selective product offers.

Approximately 9% of consumers with Good FICO® Scores are likely to become seriously delinquent in the future.

Your credit score plays a big role in determining the interest rate and terms you’ll get when financing a car. So where does a 727 credit score stand when it comes to auto loans?

While lenders consider your entire credit profile your score gives a quick snapshot of your creditworthiness. Generally the higher your score, the better financing options you can qualify for.

What Credit Score Do You Need for the Best Car Loan Rates?

Auto lenders view borrowers with credit scores of 720 or higher as having excellent credit, This tier typically unlocks the most competitive interest rates and loan terms

For example, according to myFICO’s data in November 2022, borrowers with credit scores of 720+ had an average new auto loan interest rate of 5.64%. With a score between 690-719, the average rate was 6.83%. And for the 660-689 range, the average rate jumped to 9.19%.

So while scoring above 720 gives you the best shot at prime financing, a score slightly below this mark may qualify you for relatively affordable rates as well. Many lenders draw the line between prime and subprime borrowers around the 640-660 range.

Evaluating a 727 Credit Score for Car Loans

A 727 credit score generally falls into the good credit category. The main credit scoring models, including FICO and VantageScore, classify scores from 670-739 as good.

With a good credit score like 727:

-

You should have reasonable chances of approval from most lenders.

-

You likely won’t qualify for top-tier interest rates reserved for those with excellent scores of 720+ or higher. But you may still be able to get competitive pricing.

-

Your rates and terms will generally be more favorable compared to applicants with fair credit (scores under 670).

According to FICO’s analysis, borrowers with credit scores in the 727 range have a 1.9% likelihood of becoming seriously delinquent on loan payments. So auto lenders see these applicants as relatively low-risk.

Your auto loan rates can vary significantly between lenders, even with the same credit score. So it pays to compare multiple offers. Under FICO models, all rate shopping within a short period counts as a single credit pull, so it won’t hurt your score.

Tips for Improving Your Credit Score for an Auto Loan

If your goal is to reach the 720+ tier to potentially qualify for a lender’s best auto financing, here are some tips that may help boost your credit score over time:

-

Keep credit card balances low. Experts suggest maintaining credit utilization under 30% across all cards. But averages are even lower for those with top scores.

-

Pay bills on time. Payment history is the biggest factor in your scores. Set up autopay or reminders to avoid late payments.

-

Limit new credit applications. Each application causes a hard inquiry that may slightly ding your score short-term. Only apply for accounts you currently need.

-

Build credit history. In general, older accounts strengthen your profile. Letting accounts age while keeping up good habits can help.

-

Maintain credit mix. Lenders like to see you can manage different types of credit, like installment loans and revolving accounts.

-

Dispute errors. If you spot mistakes on your credit reports that may be lowering your scores, dispute them with the bureaus.

-

Monitor your scores. Checking your scores regularly helps you gauge your progress. Consider signing up for free credit monitoring.

What Interest Rate Can I Expect With a 727 Credit Score?

While your actual rates depend on multiple factors, here are some examples of average used auto loan rates from major lenders for applicants with good credit scores in the 727 range:

- Capital One: 5.99% – 9.99% APR

- Bank of America: 6.49% – 9.99% APR

- Wells Fargo: 6.01% – 9.01% APR

- Chase: 6.01% – 9.01% APR

For context, buyers with new car loans and credit scores of 720+ had an average interest rate of just 5.64% in November 2022 according to myFICO.

So while your 727 score may disqualify you from top rates, you can likely still find competitive pricing, especially if you compare multiple lenders. Bringing your score above 720 through responsible credit management may help you potentially qualify for even lower rates.

What Other Factors Do Auto Lenders Consider?

When reviewing your car loan application, lenders look at your entire financial profile, not only your credit scores. Here are some other key factors that come into play:

Income – Lenders want to see you have enough steady verifiable income to comfortably make the monthly payments.

Debt-to-income ratio – Your total monthly debt payments divided by gross monthly income. Most lenders look for a ratio under 50%.

Down payment – The more you put down, the less financing risk for the lender. Minimum down payments allowable can vary by lender.

Loan term – The longer the repayment term, the higher the risk. Many lenders cap terms at 60-72 months for prime borrowers.

Collateral – The car’s value matters too. Some lenders limit loans to certain percentages of the car’s resale value.

While your 727 credit score puts you in a reasonably competitive position for auto loan approval, having other strong financial qualifications can potentially help further.

How Else Can I Get the Best Car Loan Rates?

Beyond improving your credit and financial profile, here are some other tips that may help you get approved for the lowest auto loan rates possible:

-

Get preapproved – Having a preapproval letter can give you negotiation leverage when car shopping. Just beware it causes a hard credit inquiry.

-

Compare multiple lenders – Each lender uses different approval criteria. Shop around online and locally to find your best deal.

-

Bring a down payment – A higher down payment signals lower risk to lenders and may help you qualify for better rates.

-

Opt for a shorter loan term – Shorter terms often have lower interest rates, though monthly payments are higher.

-

Consider a cosigner – Adding a cosigner with excellent credit may help you qualify for a lower rate.

-

Look for current lender discounts – Ask if your bank or credit union offers any rate discounts for existing customers.

While a 727 credit score is considered good, raising it above 720 can potentially unlock even better auto loan rates and terms. But diligently comparing lenders, even with your current score, is key to finding affordable financing.

How to build up your credit score

Your FICO® Score is solid, and you have reasonably good odds of qualifying for a wide variety of loans. But if you can improve your credit score and eventually reach the Very Good (740-799) or Exceptional (800-850) credit-score ranges, you may become eligible for better interest rates that can save you thousands of dollars in interest over the life of your loans. Here are few steps you can take to begin boosting your credit scores.

Check your FICO ScoreFICO® regularly. Tracking your FICO® Score can provide good feedback as you work to build up your score. Recognize that occasional dips in score are par for the course, and watch for steady upward progress as you maintain good credit habits. To automate the process, you may want to consider a credit-monitoring service. You also may want to look into an identity theft-protection service that can flag suspicious activity on your credit reports.

Avoid high credit utilization rates. High credit utilization, or debt usage. Try to keep your utilization across all your accounts below about 30% to avoid lowering your score.

Try to establish a solid credit mix. The FICO® credit-scoring model tends to favor users with multiple credit accounts, and a blend of different types of credit, including installment loans like mortgages or auto loans and revolving credit such as credit cards and some home-equity loans. This doesnt mean you should take on debt you dont need, but it suggests you shouldnt be shy about prudent borrowing as appropriate.

Make sure you pay your bills on time. Avoiding late payments and bringing overdue accounts up to date are among the best things anyone can do to increase credit scores. Establish a system and stick to it. Whether its automated tools such as smartphone reminders and automatic bill-payment services or sticky notes and paper calendars, find a method that works for you. Once youve stuck with it for six months or so, youll find yourself remembering without being nagged (but keep the reminders around anyway, just in case).

How to improve your 727 Credit Score

A FICO® Score of 727 provides access to a broad array of loans and credit card products, but increasing your score can increase your odds of approval for an even greater number, at more affordable lending terms.

Additionally, because a 727 FICO® Score is on the lower end of the Good range, youll probably want to manage your score carefully to prevent dropping into the more restrictive Fair credit score range (580 to 669).

The best way to determine how to improve your credit score is to check your FICO® Score. Along with your score, youll receive information about ways you can boost your score, based on specific information in your credit file. Youll find some good general score-improvement tips here.

How a Car Loan Affects Credit Score – Auto loans raise or lower scores? How fast? How many points?

FAQ

Can I buy a car with a 727 credit score?

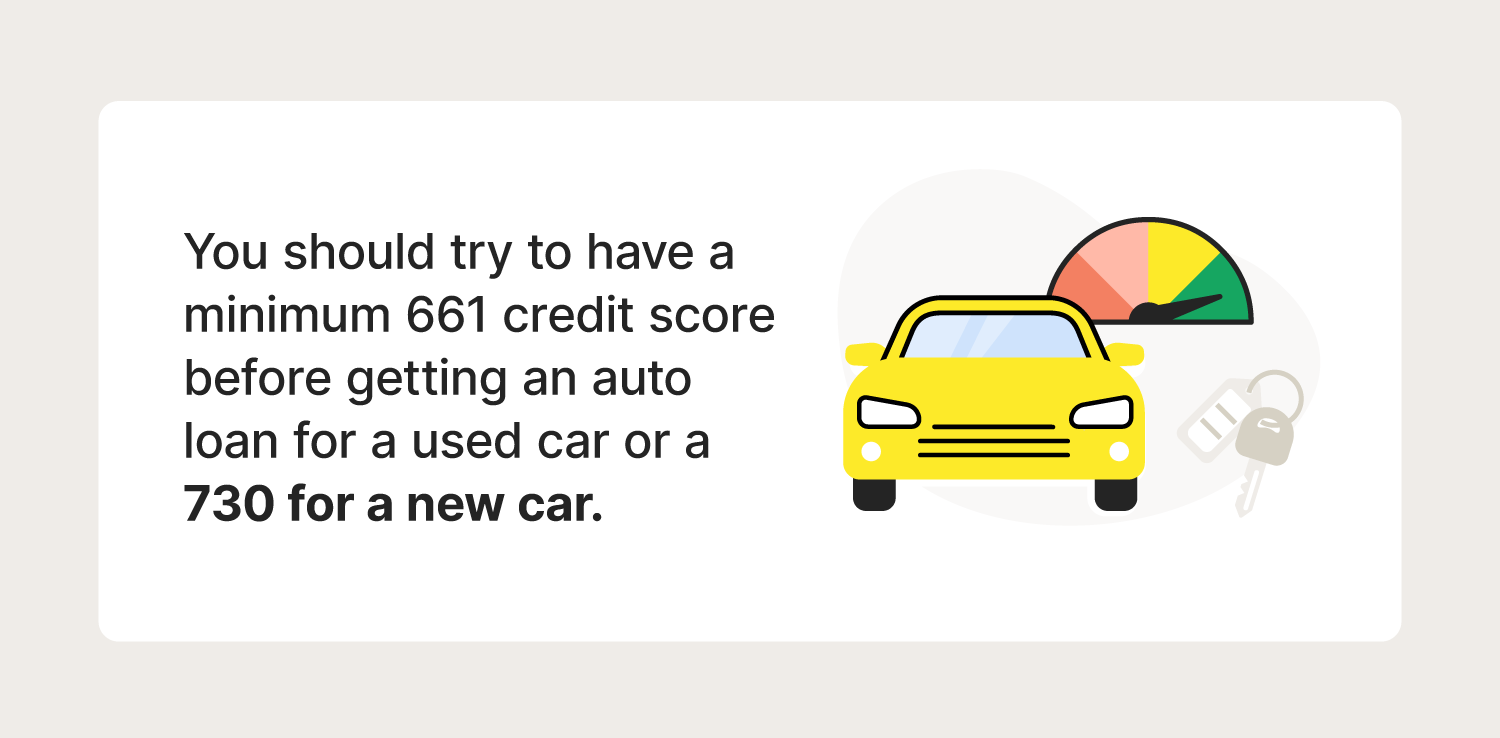

Still, you typically need a good credit score of 661 or higher to qualify for an auto loan.Mar 18, 2025

What credit score is needed for a $30,000 car loan?

What loan can I get with a 727 credit score?

You can get a personal loan with an 727 credit score, but not every lender may approve you. Some lenders require scores well into the 700s for consideration. However, depending on the lender, you may get a personal loan with rather competitive terms.

What is an excellent credit score for a car loan?

According to Experian, a target credit score of 661 or above should get you a new-car loan with an annual percentage rate of around 6.70% or better, or a used-car loan around 9.06% or lower. Superprime: 781-850.

Is a 727 credit score a good credit score?

A 727 credit score is considered a good credit score by many lenders. Credit scores are used by lenders to determine the potential risk of lending to a borrower and are based on credit reports that document your credit history. A good credit score indicates a higher likelihood of repayment. Having good credit can be a significant advantage.

Is a 727 FICO ® score good?

A 727 FICO ® Score is Good, but by raising your score into the Very Good range, you could qualify for lower interest rates and better borrowing terms. A great way to get started is to get your free credit report from Experian and check your credit score to find out the specific factors that impact your score the most.

What is a good credit score for a car loan?

Usually, higher scores mean lower interest rates on loans. According to Experian, a target credit score of 661 or above should get you a new-car loan with an annual percentage rate of around 6.70% or better, or a used-car loan around 9.06% or lower. Superprime: 781-850. 5.18%. 6.82%. Prime: 661-780. 6.70%. 9.06%. Nonprime: 601-660. 9.83%. 13.74%.

What credit score do you need to buy a car?

The report also found that on average, the credit score for a used-car loan was 684, while the average score for a new-car loan was 756. What minimum credit score is needed to buy a car? There isn’t one specific score that’s required to buy a car because lenders have different standards.

What is a good credit score?

Though credit scoring models vary, scores from the high 600s to mid-700s (on a scale of 300 to 850) are usually regarded as good. Generally, the higher your credit score, the better your chances of obtaining loans with favorable terms, including lower interest rates and fewer fees.

Can a low credit score help you get a car loan?

Borrowers with scores of 501 to 600 account for more than 15.64% of cars financed, while people with scores of 500 or below account for 2.39%, according to Experian. A lower credit score won’t necessarily keep you from securing a car loan, but it might spike your interest rate, leading to higher payments. Stress less. Track more.