You have a credit score of 684. Its a solid number, but not quite in the range of “Very Good” or “Excellent.” This score indicates a generally reliable credit history, though not without a few hiccups. A 684 credit score suggests moderate lending risk for lenders, meaning you might qualify for various financial products but possibly not the best terms available.

This guide will explore what a 684 credit score means for you. Well discuss its benefits and impact on your borrowing options, interest rates, ways to improve your scores and financial decisions. By the end, youd better know where you stand and what steps you can take to enhance your score, allowing you to make informed decisions about your financial future.

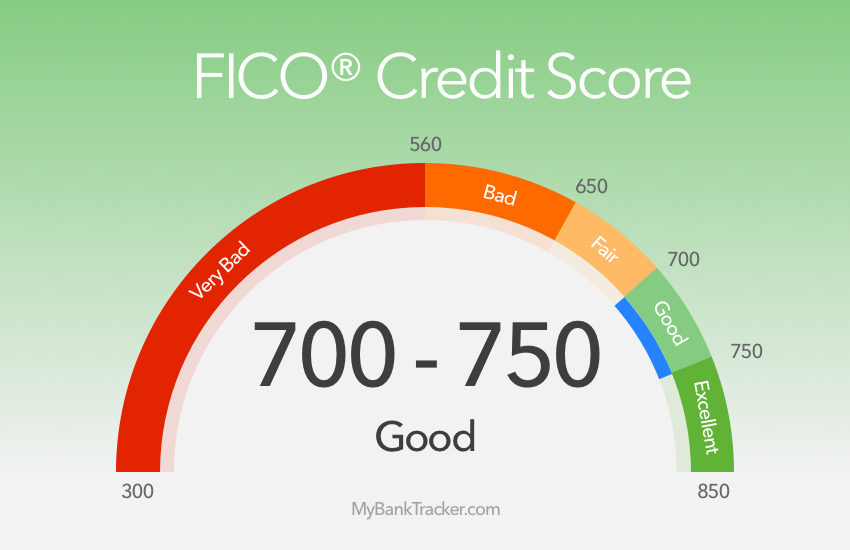

A FICO score of 684 falls right in the middle of what is considered a “good” credit score range But what exactly does it mean to have a credit score of 684? Is that good or bad when it comes to getting approved for credit and loans? Let’s take a closer look

What is a FICO Score?

First, it’s important to understand what a FICO score is FICO is an acronym for the Fair Isaac Corporation, the company that created the most commonly used credit scoring model in the United States.

Your FICO score is a three-digit number that ranges from 300 to 850 and is calculated based on information in your credit report. It’s essentially a snapshot of your credit health that lenders can use to assess how likely you are to repay borrowed money.

The higher your FICO score, the lower your perceived credit risk to lenders. But no single “magic number” can guarantee whether or not you’ll get approved for credit. Many factors go into a lender’s decision

FICO Score Ranges

FICO scores fall into the following classic ranges:

- 800-850: Exceptional

- 740-799: Very Good

- 670-739: Good

- 580-669: Fair

- 300-579: Very Poor

So with a score of 684, you’re in the “Good” credit range. But is that considered good or bad overall?

The Pros of a 684 FICO Score

A FICO score of 684 has some key advantages:

-

It’s above the average credit score. As of 2022, the average FICO score in the United States was 714, so 684 is just slightly below that. You’re doing better than tens of millions of Americans.

-

You have access to credit. Scores above 620 are generally considered decent enough to get approved for credit cards and loans, albeit sometimes with higher interest rates or fees. But if your score was very poor (below 580), you’d have a hard time getting approved for anything.

-

You can get reasonable rates. While a 684 score won’t get you the very best rates, it’s good enough for relatively affordable rates with many lenders. You can still save money on interest compared to someone with poor credit.

-

You’re close to “very good” range. With some work, you can likely increase your score and break the 700 barrier before long. Getting above 740 would qualify you for even better rates. Your 684 score means you’re on the right track.

The Cons of a 684 Score

However, there are some potential drawbacks to having a credit score of 684 as well:

-

You may pay more interest. You will probably pay slightly higher interest rates than someone with excellent credit. With a score in the mid-to-high 700s, you’d get even better deals.

-

You may not get big credit lines. Your credit limits may be lower than they’d be if your score was higher. Lenders remain a bit cautious with credit lines for borrowers under 700.

-

You may not get top rewards cards. The most lucrative travel and cash back credit cards typically require credit scores of at least 720 to get approved. A 684 score may not qualify for premium rewards.

-

One slip-up could drop your score. With a score on the lower end of “good,” just one late payment or credit mistake could knock your score down to “fair.” Your credit is in decent shape, but still sensitive.

How to Get a 684 FICO Score

A credit score of 684 is often achieved by:

-

Having a relatively short credit history. If you’re new to credit, it takes time to build a strong profile. Many people start in the mid-to-high 600s.

-

Making minor mistakes. If you have late payments or collections from when you were younger but have been paying on time recently, you could be around 684.

-

Carrying long-term debt. Installment loans like mortgages and student loans bring down scores more than revolving debt. If you have large, long-term balances, your score may be lower.

-

Racking up high balances. Credit utilization ratios above 30% start to drag down your score. If your balances are over half your limits, that could keep your score around 680.

How to Raise Your 684 Score

Here are some tips for increasing your credit score from the mid-680s:

-

Pay bills on time. Delinquencies severely hurt your score, so prompt payment is critical. Set up autopay or reminders to avoid lateness.

-

Lower credit utilization. Get balances below 30% of your credit limits. Pay down cards with the highest balances first.

-

Don’t close old accounts. Having long, positive payment histories helps your score. Keep old cards open unless they have fees.

-

Limit hard inquiries. Each application for credit dings your score a little. Only apply for credit you need, and avoid opening too many new accounts at once.

-

Monitor your credit reports. Dispute any errors you find to keep your reports accurate. Stay vigilant for identity theft.

-

Build positive history. As you demonstrate responsible use of credit over time, your score will gradually increase. Patience and good habits are key.

The Verdict on a 684 Score

A FICO score of 684 is a decent credit score, sitting right in the middle of the “good” credit range. It comes with pluses and minuses: You have access to credit but may not get ideal interest rates or approvals for premium cards and loans. Overall, a 684 is an encouraging score that shows you’re on the right track, though still with room for improvement.

With diligent credit management over time, you can increase your 684 score to the “very good” range and beyond. Check your latest scores, study your full credit reports regularly, and implement positive financial habits. A journey of small steps can go a long way toward your ultimate credit goals.

Credit Product Eligibility with a 684 Credit Score

Navigating the world of credit products with a 684 credit score can be rewarding, but it also comes with its own challenges. Heres what you can expect:

- With a 684 credit score, youre likely to qualify for most standard credit cards. However, the elite, top-tier cards with the best perks and lowest interest rates might be just out of reach.

- You can still enjoy benefits like rewards points, cashback, and unsecured credit lines. The terms will be reasonable, though not as competitive as those offered to individuals with higher scores.

- Securing an auto loan with a 684 score is generally feasible. However, your interest rates will be higher than those available to individuals with Very Good or Excellent credit.

- Given the potential for higher interest rates, it is important to shop around and evaluate offers from several lenders. This way, you can find the best annual percentage rate (APR) and save money over the life of the loan.

- With a 684 credit score, you have a good chance of qualifying for a mortgage. Lenders will view you as a moderate risk, making homeownership an attainable goal.

- While you can secure a mortgage, the interest rates will not be as low as those given to borrowers with higher credit scores. Its important to factor this into your long-term financial planning.

- Approval for personal loans largely depends on the lenders criteria. Some lenders readily approve your application, while others are more stringent.

- Specific lenders might consider non-traditional factors such as income, employment history, and other financial behaviors. This can work to your advantage if your overall financial health is strong, even if your credit score isnt perfect.

Greater Willingness of Lenders to Extend CreditÂ

Lenders are more willing to extend credit to you with a 684 score. While youre likely to be approved, the interest rates and rewards offered may not be as competitive as those for individuals with Very Good or Excellent scores. Nonetheless, lenders willingness to work with you is a significant benefit, providing you with more options to meet your financial needs.

Is 684 A Good Credit Score? – CreditGuide360.com

FAQ

Can I get a loan with a 684 credit score?

A FICO® Score of 684 provides access to a broad array of loans and credit card products, but increasing your score can increase your odds of …

How good is a 684 FICO score?

With the FICO credit scoring model, credit scores ranging from 300 to 579 are considered poor. Scores that range from 580 to 669 are considered fair. Anywhere between 670 to 739 is considered good. A credit score between 740 to 799 is considered very good.

What is an excellent FICO score?

An excellent FICO score is generally considered to be 800 or higher.

Can I buy a car with a 684 credit score?

There is no minimum credit score required to buy a car, but most lenders have minimum requirements for financing. Most borrowers need a FICO score of at least 661 to get a competitive rate on an auto loan.

Is 684 a good credit score?

However, even with a 684 credit score, you still have opportunities to obtain decent credit cards or loans. It’s worth noting that making slight improvements to your credit can significantly expand your options and lead to substantial savings. Credit Rating: 684 is still considered a fair credit score.

Is a FICO score of 684 good?

Approximately 21 percent of American consumers hold a FICO score in the good range, which includes a score of 684. This will give you access to more loan options and better interest rates than people in lower ranges. However, FICO does have ranges above good, so you won’t be qualifying for the absolute best loan terms with lenders.

Can you get a student loan with a 684 credit score?

Student loans are some of the easiest loans to get with a 684 credit score, seeing as more than 60% of them are given to applicants with a credit score below 700. A new degree may also make it easier to repay the loan if it leads to more income. Note: Borrower percentages above reflect 2020 Equifax data.

Can a 684 credit score qualify for a car loan?

Absolutely. Your 684 credit score will qualify you for an auto loan, assuming your income justifies it. However, it’s important to realize that your credit score can make a big difference in the interest rate you get. And this is especially true in auto lending.

Is 690 a good credit score?

Your 690 credit score puts you solidly in the mainstream of American consumer credit profiles, but some additional time and effort can raise your score into the Very Good range (740-799) or even the Exceptional range (800-850). To keep up your progress and avoid losing ground, steer clear of behaviors that can lower your credit score.

What type of credit does the FICO ® score favor?

The FICO ® Score tends to favor a variety of credit, including both installment loans (i.e., loans with fixed payments and a set repayment schedule, such as mortgages and car loans) and revolving credit (i.e., accounts such as credit cards that let you borrow within a specific credit limit and repay using variable payments).