Bankrate is always editorially independent. While we adhere to strict , this post may contain references to products from our partners. Heres an explanation for . Our is to ensure everything we publish is objective, accurate and trustworthy. Bankrate logo

Founded in 1976, Bankrate has a long track record of helping people make smart financial choices. We’ve maintained this reputation for over four decades by demystifying the financial decision-making process and giving people confidence in which actions to take next.

Bankrate follows a strict editorial policy, so you can trust that we’re putting your interests first. All of our content is authored by highly qualified professionals and edited by subject matter experts, who ensure everything we publish is objective, accurate and trustworthy.

Our investing reporters and editors focus on the points consumers care about most — how to get started, the best brokers, types of investment accounts, how to choose investments and more — so you can feel confident when investing your money.

The investment information provided in this table is for informational and general educational purposes only and should not be construed as investment or financial advice. Bankrate does not offer advisory or brokerage services, nor does it provide individualized recommendations or personalized investment advice. Investment decisions should be based on an evaluation of your own personal financial situation, needs, risk tolerance and investment objectives. Investing involves risk including the potential loss of principal. Bankrate logo

Bankrate follows a strict editorial policy, so you can trust that we’re putting your interests first. Our award-winning editors and reporters create honest and accurate content to help you make the right financial decisions.

We value your trust. Our mission is to provide readers with accurate and unbiased information, and we have editorial standards in place to ensure that happens. Our editors and reporters thoroughly fact-check editorial content to ensure the information you’re reading is accurate. We maintain a firewall between our advertisers and our editorial team. Our editorial team does not receive direct compensation from our advertisers.

Bankrate’s editorial team writes on behalf of YOU – the reader. Our goal is to give you the best advice to help you make smart personal finance decisions. We follow strict guidelines to ensure that our editorial content is not influenced by advertisers. Our editorial team receives no direct compensation from advertisers, and our content is thoroughly fact-checked to ensure accuracy. So, whether you’re reading an article or a review, you can trust that you’re getting credible and dependable information. Bankrate logo

The Incredible Advantage You Have as an 18-Year-Old Investor

Let’s be real – at 18, investing money probably isn’t the first thing on your mind. Maybe you’re thinking about college, your first job, or just enjoying your newfound adulthood But here’s the thing starting to invest at 18 gives you a massive advantage that older folks would kill to have – time

Time is literally your superpower when it comes to investing. Thanks to compound interest (which Einstein allegedly called “the eighth wonder of the world”), even small amounts invested now can grow into something substantial by the time you’re ready to retire.

I remember when I was 18 I thought investing was something only rich people did. Boy, was I wrong! If I’d started then rather than waiting till my late 20s I’d be in a much better position today. Don’t make my mistake!

Your Financial Goals as a Young Adult

Before jumping into specific investments let’s talk about what you might be saving for

- Emergency Fund: This is your financial safety net

- Education: College costs or further training

- Big Purchases: Like a car or home down payment

- Retirement: Yes, think about it now!

- Wealth Building: Growing your money for future opportunities

Each of these goals requires different investment approaches and timeframes. Let’s break down the best options for each.

Retirement Investing: Start Now, Thank Yourself Later

It sounds crazy to think about retirement at 18, but this is actually your biggest opportunity. Here’s why:

401(k) Plans: Free Money Is the Best Money

If you have a job that offers a 401(k), especially with employer matching, jump on it immediately. This is literally free money!

How it works:

- You contribute pre-tax money from your paycheck

- Your employer might match a percentage of your contributions

- The money grows tax-deferred until retirement

- Many plans now offer a Roth option, which I’ll explain next

Roth IRA: Your Best Friend for Tax-Free Growth

If I could recommend just ONE investment account for an 18-year-old, it would be a Roth IRA. Here’s why it’s perfect for young investors:

- You contribute after-tax dollars (which isn’t a big hit when you’re in a low tax bracket)

- Everything in the account grows TAX-FREE

- You can withdraw your contributions (but not earnings) penalty-free if needed

- At retirement, ALL withdrawals are completely tax-free

For 2024, you can contribute up to $7,000 per year to a Roth IRA. Even if you can only put in $50 or $100 a month, that money will have DECADES to grow tax-free.

What to Invest In Within Your Retirement Accounts

Once you’ve opened a 401(k) or Roth IRA, what should you actually invest in? At 18, with 40+ years until retirement, you can afford to be aggressive:

- Index ETFs: Exchange-traded funds that track market indexes like the S&P 500 provide broad diversification with low fees. They typically outperform actively managed funds over the long run.

- Target Date Funds: These automatically adjust their risk level as you approach retirement – a set-it-and-forget-it option.

- Dividend-paying stocks: Companies that share profits with shareholders through dividends can provide both growth and income.

Medium-Term Goals: Saving for Big Purchases

Not all your investing should be locked away until retirement. For goals like buying a car, making a house down payment, or paying for education, consider these options:

Exchange-Traded Funds (ETFs)

ETFs are a basket of securities that trade like individual stocks. They’re perfect for medium-term goals because:

- They provide instant diversification

- They have lower fees than most mutual funds

- You can sell them any time the market is open

- They come in varieties ranging from conservative to aggressive

For money you’ll need in 3-7 years, consider a mix of stock and bond ETFs to balance growth potential with stability.

Home Ownership: A Special Case

Buying a home is often both a lifestyle choice and an investment. While traditional wisdom says homes are great investments, the reality depends on:

- How long you’ll live there (at least 5-7 years to make financial sense)

- The housing market in your area

- Current mortgage interest rates

- Rent vs. buy calculations for your situation

If homeownership is on your radar, start saving for a down payment in a relatively safe, liquid investment.

Short-Term Goals & Emergency Funds

Every young adult needs an emergency fund covering 3-6 months of expenses. This isn’t really an investment – it’s financial insurance. Keep this money in:

- High-yield savings accounts

- Money market funds

- Short-term CDs

The returns won’t be exciting, but that’s not the point. This money needs to be safe and available when you need it.

College Savings Options

If you’re saving for your own education (or perhaps planning far ahead for future children), consider these education-specific investments:

529 College Savings Plans

Nearly every state offers these tax-advantaged education savings plans:

- Contributions grow tax-free when used for qualified education expenses

- Some states offer additional tax benefits

- Contribution limits are typically very high

- Parents and grandparents can also contribute

Coverdell Education Savings Accounts

These federally-sponsored accounts also allow tax-free withdrawals for education:

- $2,000 annual contribution limit per beneficiary

- More investment flexibility than most 529 plans

- Can be used for K-12 expenses as well as college

U.S. Savings Bonds

These government-backed securities offer:

- Tax-free interest when used for higher education

- Extremely low risk

- Modest but guaranteed returns

Practical Investment Strategy for an 18-Year-Old

Now, let’s put this all together into a practical plan you can actually follow:

Step 1: Start Your Emergency Fund

Before investing for growth, set aside money for emergencies:

- Aim for $1,000 initially, then build toward 3-6 months of expenses

- Keep this in a high-yield savings account

Step 2: Take Advantage of Free Money

If your employer offers a 401(k) match:

- Contribute at least enough to get the full match

- Choose a target date fund or low-cost index funds

Step 3: Open a Roth IRA

This should be your priority if you have earned income:

- Try to contribute regularly, even small amounts

- Invest in a total stock market index ETF

- Set up automatic contributions if possible

Step 4: Invest for Medium-Term Goals

For money you’ll need in 3-7 years:

- Consider a balanced portfolio of stock and bond ETFs

- Adjust the ratio based on your timeline and risk tolerance

- Keep these investments in a regular taxable brokerage account

Step 5: Continue Learning About Investing

The best investment might be in your financial education:

- Read books on personal finance

- Follow reputable financial websites

- Consider taking a financial literacy course

Common Mistakes Young Investors Should Avoid

I’ve seen too many young people make these mistakes:

- Day trading or stock picking without knowledge: This is gambling, not investing

- Following investment advice from social media: Be wary of “get rich quick” schemes

- Investing emergency money: Keep your safety net separate from investments

- Ignoring fees: Even small percentage differences add up dramatically over time

- Being too conservative: At 18, time is on your side – don’t fear normal market volatility

Real Talk: The Challenge of Investing at 18

Let’s be honest – investing at 18 is HARD. You probably don’t have much money, and what you do have might be needed for education, transportation, or just living expenses.

That’s OK! Even small amounts matter. Consider this:

- Just $50 a month invested from age 18 to 65 could grow to over $200,000 (assuming 8% average returns)

- Even if you can only invest sporadically, getting started builds the habit

- Understanding investing concepts now will benefit you tremendously as your income grows

Final Thoughts

The fact that you’re even thinking about investing at 18 puts you ahead of 99% of your peers. The absolute best investments an 18-year-old can make are:

- In yourself – through education and skills that increase your earning potential

- In good financial habits – including regular saving and investing

- In time-leveraged accounts – like Roth IRAs that maximize tax advantages

- In low-cost, diversified investments – that will grow steadily over decades

Remember that investing is a marathon, not a sprint. Your goal isn’t to get rich overnight but to build wealth consistently over time.

I wish someone had explained all this to me when I was 18! I’d have made very different choices. But that’s the thing about being young – you have time to learn, make mistakes, adjust, and still come out way ahead.

What questions do you have about investing as a young adult? The most important step is simply to begin!

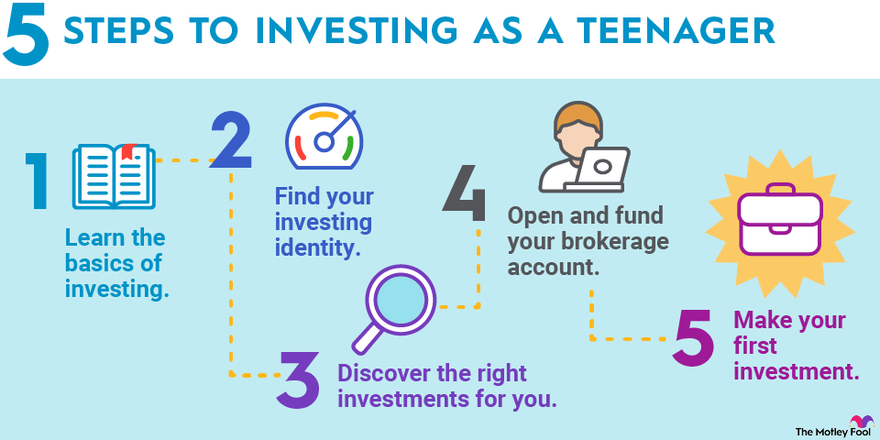

Set your investment goals

Identify what you hope to achieve with your investments. Are you saving for a big purchase like a car, college tuition, a home of your own or just aiming to grow your wealth? Having clear goals will guide your investment decisions and help you choose the right investments. Remember, investing is not about getting rich quickly but growing your money over the long term. For short-term goals, a high-yield savings account might be more appropriate.

What teens should consider before starting to invest

Investing involves the risk of losing some or all of your initial investment. The degree of risk varies depending on the type of investment. For example, stocks are generally riskier than bonds, but they also offer the potential for higher returns. It’s important to understand these risks and to only invest money that you can afford to lose.

Don’t let the risks stop you from investing, though. Instead, learn to manage risk effectively by investing in low-cost, broadly diversified index funds, setting a budget for your investments and maintaining a long-term perspective.

Before starting to invest, it’s helpful to ask yourself the following questions:

- Do you have money that you can invest, and are you prepared to lose some or all of this money if your investments don’t perform as expected?

- Are you willing to commit time to learning about investing and managing your holdings?

- If you’re under age 18, are you willing to work with a parent or guardian to set up a custodial account?

If you can confidently answer ‘yes’ to these questions, you may be ready to start your investing journey. Just remember, investing is often a long-term commitment, so it’s important to continue learning and adapting as you go.

How To Invest as a Teenager To Become A Millionaire in Your 20s

FAQ

What is the best way to invest money as an 18 year old?

The best place to start is by opening a Roth IRA or a brokerage account with a reputable platform like Fidelity, Vanguard, or Schwab. A Roth IRA is great for young investors because your contributions grow tax-free, and you’ll thank yourself later when you can withdraw those earnings without paying taxes in retirement.

How much will $1000 invested be worth in 20 years?

How much is $100 a month for 18 years?

What is the 7% rule in investing?

The “7% rule” in investing can refer to two different strategies: one is a trading rule to cut losses by selling a stock that has dropped 7% from its purchase price, while the other is a debt payoff rule to pay off any debt with an interest rate of 7% or higher before investing. It’s important to distinguish which “7% rule” is being discussed based on the context.