Paying off collections could increase scores from the latest credit scoring models, but if your lender uses an older version, your score might not change. Regardless of whether it will raise your score quickly, paying off collection accounts is usually a good idea.

Its possible that paying off a collection account will increase your credit score, but that largely depends on the version of the software used to calculate the score.

Paying off collection accounts can be an important step in rebuilding your credit. But a common question is – how much will my credit score increase if I pay off collections? The answer is not straightforward since the impact on your credit score depends on several key factors In this comprehensive guide, I’ll explain how collections affect your credit, whether paying them off improves your scores, and how much your credit could increase when collections are paid.

How Do Collections Hurt Your Credit Scores?

Collections have a major negative impact on your credit for several reasons

-

They fall under payment history – the biggest factor in credit scores, accounting for 35% of your FICO® Score.

-

A collection for $100 or more can lower credit scores for up to 7 years from the first missed payment.

-

Both paid and unpaid collections can reduce scores calculated with older FICO models like the commonly used FICO® 8.

-

Even a single unpaid collection can lower your credit scores significantly. Multiple collections have an even greater impact.

So collections clearly damage credit scores. But what happens when you pay them off?

Does Paying Off Collections Raise Credit Scores?

Whether paying collections improves your credit score depends on which scoring model is used:

-

Newer FICO® 9, 10 and VantageScore 3.0, 4.0 ignore paid collections. So paying collections can increase scores calculated with these newer models.

-

But paid collections still lower scores from older FICO versions like FICO® 8. So your score may not change if your lender uses an older model.

The impact also depends on the type of debt:

-

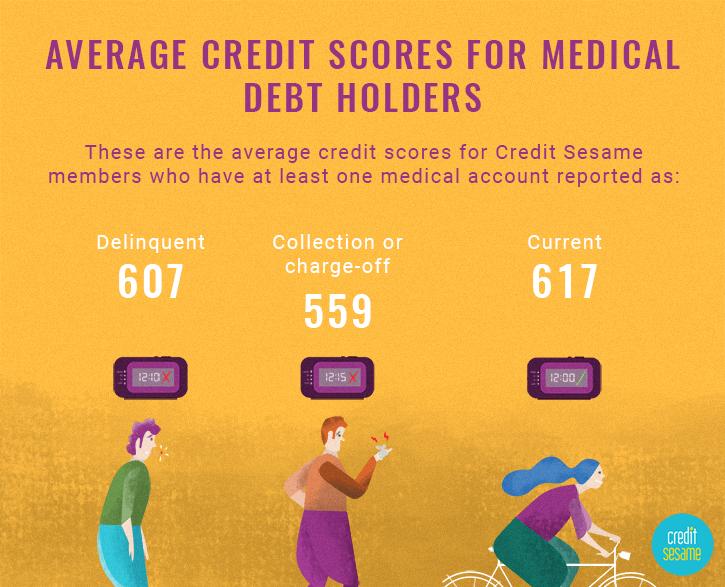

Paid medical collections don’t appear on credit reports and have no impact on scores.

-

Unpaid medical collections under $500 aren’t reported and don’t affect scores either.

-

For non-medical collections, paying them off only raises your score with newer credit models. With commonly used older models, your score won’t improve.

How Much Will Credit Scores Increase?

Since paying collections doesn’t always increase credit scores, how much your score goes up varies:

-

With new credit models, your score could increase substantially after paying off collections – potentially by 100 points or more if you previously had multiple unpaid collections.

-

But with widely used older FICO versions, your score likely won’t change at all when collections are paid off.

-

For medical collections under $500, your credit score won’t increase when paid since they aren’t reported anyway.

Several key factors determine the impact of paying collections on your credit scores:

-

Age of the Collection – Newer collections hurt scores more than older ones. Paying off a recent collection improves scores more.

-

Overall Credit Profile – If you have good credit otherwise, paying collections helps scores more than if you have late payments or other negative marks.

-

Scoring Model Used – Only newer models boost scores for paid non-medical collections. Older versions see no score change.

-

Number of Collections – Multiple unpaid collections damage credit more. Paying them off improves scores more than a single collection being paid.

So while paying collections can increase credit scores calculated with newer scoring models by 100 points or more in some cases, your score may see little or no increase if your lender uses an older FICO version – which many still do.

How to Increase Credit Scores After Paying Collections

If your credit doesn’t immediately increase from paying off collections, here are some ways to continue rebuilding your credit:

-

Pay All Bills On Time – Prevent new late payments which could lower your scores again. Set up autopayments or payment reminders to stay on track.

-

Lower Credit Card Balances – Keep credit card balances below 30% of their limits, as high utilization also hurts credit. Make extra payments to reduce balances.

-

Limit New Credit Applications – Apply for new credit only when needed, as too many applications can lower scores temporarily.

-

Correct Credit Report Errors – If any information on your credit reports is inaccurate or incomplete, file disputes to get errors corrected.

-

Wait It Out – As time passes, the negative impact of both paid and unpaid collections lessens. Your scores will gradually improve.

While paying off collections doesn’t guarantee an immediate boost to your credit, it can increase your scores substantially over time. And it’s still smart to pay collections rather than leaving debts unpaid. By combining this with other credit-building strategies, you can continue to improve your credit situation.

Will Your Credit Score Improve if You Pay Off All of Your Collections?

Depending on the nature of the collection account and the model used to calculate your score, paying off a collection account could cause your score to increaseâor it could have no effect at all on your score.

Paying off collection accounts can raise credit scores calculated using FICO® Score 9 and 10 and VantageScore 3.0 and 4.0, but it wont have any effect on scores produced by older FICO scoring models.

That includes the many lenders who use FICO® Score 8 and, at least for now, issuers of mortgages known as conforming loans, which meet requirements for purchase by Fannie Mae and Freddie Mac. These government-sponsored enterprises, which purchase the majority of U.S. mortgage loans from the lenders that issue them, currently require lenders to report applicants credit scores using “classic FICO” models that predate FICO® Score 8. All that will soon change, however.

In 2022, the Federal Housing Finance Agency (FHFA)âthe regulator that sets lending guidelines for Fannie Mae and Freddie Macâannounced that lenders issuing conforming loans must use FICO® Score 10 T and VantageScore 4.0 to evaluate mortgage applicants. (FICO® Score 10 T is a variant of FICO® Score 10 that, like VantageScore 4.0, can use more nuanced “trended data” compiled at the national bureaus.) The conversion to the new credit scoring requirements is scheduled to be completed by the end of 2025. Among the many implications of the change is the potential for paid collections to help credit scores in the mortgage application review process.

What Are Collection Accounts?

A collection account is an entry on your credit report that signifies an unpaid debt in default (more than 90 days past due) that your creditor has turned over to an in-house collection department or a third-party debt collection agency.

Accounts in collections appear on your credit report and can have serious repercussions for your credit scores. Its usually not necessary to check your credit report to find out if an account is in collections because collection agents are very proactive and persistent in their efforts to get payment. Theyll typically hound you by phone, mail or email, pressing you to pay up.

Paying is often a good idea, not only because you presumably owe the debt theyre seeking or even because it will get the bill collectors off your back. Theres a chance, if no guarantee, that paying off an account in collections could benefit your credit score.

Paying Collections – Dave Ramsey Rant

FAQ

Does paying off a collection increase credit score?

Paying off a collection could cause the score to increase, decrease or have no impact at all. It depends on the change in the information reported on the collection as well as the other information in the credit report.

How many points will my credit score increase if a collection is paid in full?

How Much Will Credit Score Increase After Paying off Collections? Your credit score may not increase at all when you pay off collections. However, if your debt is reported using a newer credit scoring model, your score may increase by however many points were impacted by the collections debt.

How can I raise my credit score by 100 points in 30 days?

For most people, increasing a credit score by 100 points in a month isn’t going to happen. But if you pay your bills on time, eliminate your consumer debt, don’t run large balances on your cards and maintain a mix of both consumer and secured borrowing, an increase in your credit could happen within months.

Can I get a 700 credit score with collections?

You can have a 700 credit score with collections, but it’s rare—collections usually lower scores significantly, especially if they are recent or unpaid. In general, collections will remain on a credit report for a maximum of seven years.