Buying a $400,000 home typically requires a down payment between $12,000 and $20,000, depending on the type of loan you choose. Some borrowers may qualify for zero-down programs, while others may need to budget for both a down payment and additional closing costs.

The median U.S. home price has hovered just below $400,000 in recent years, leading many prospective buyers to wonder what it takes to get into such a property.

Some buyers may be able to purchase a $400k home with no money down, depending on the loan type. Most borrowers, though, can expect to put down 3% to 5% of the purchase price, or $12,000 to $20,000.

Buying a $400000 home is a major financial milestone that requires careful planning and budgeting. As exciting as homeownership can be a house in this price range also means a substantial down payment and mortgage commitment. Here’s a detailed look at how much cash you typically need to put down on a $400k house.

Typical Down Payment Amounts

When getting a mortgage for a $400.000 home. common down payment options include

-

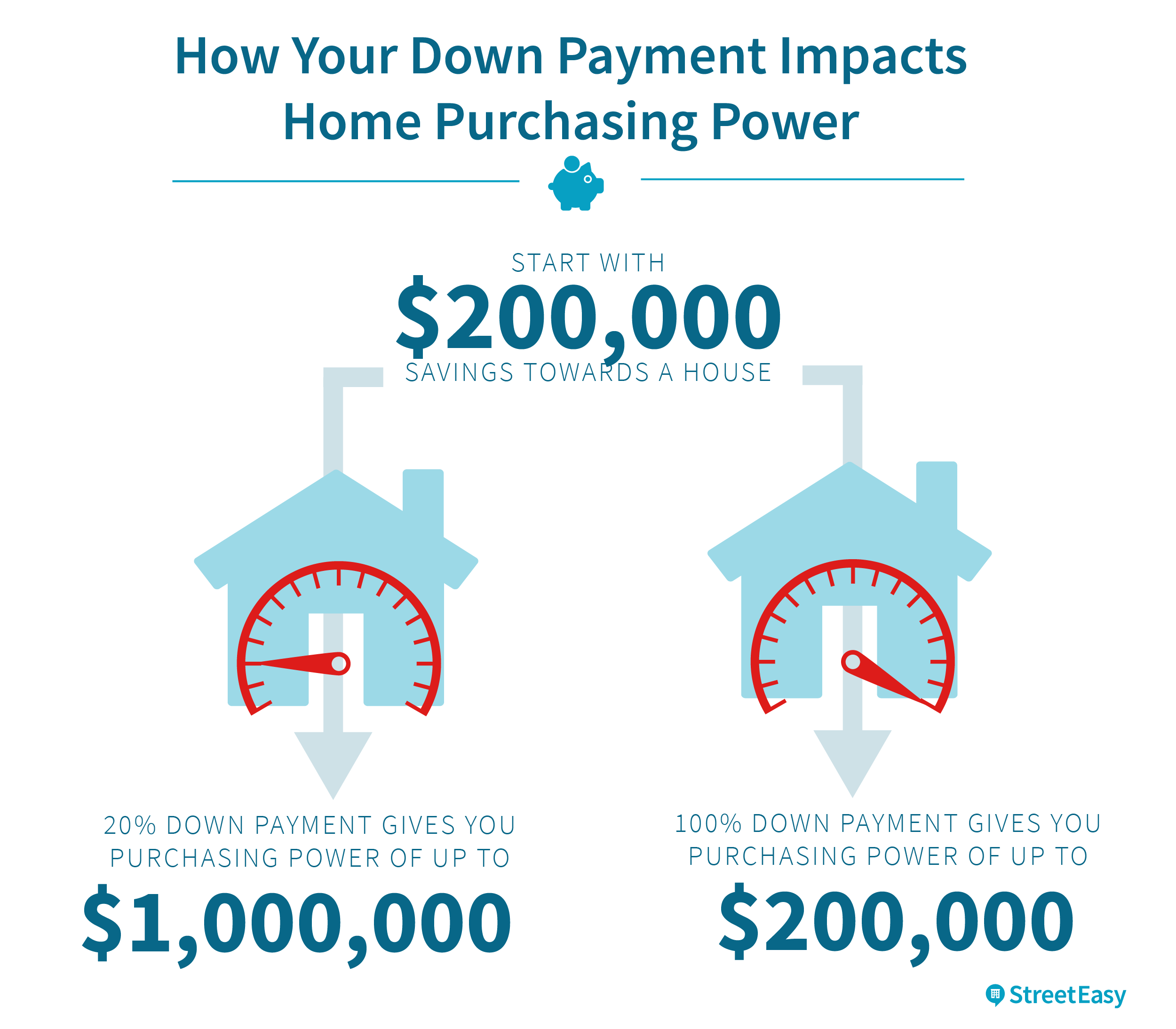

20% down – For a $400k house, 20% down is $80,000 This is an ideal amount that helps you avoid private mortgage insurance (PMI) and get better loan terms

-

15% down – A 15% down payment on $400,000 is $60,000. This is a moderate amount that reduces your monthly costs versus lower down payments.

-

10% down – With 10% down on a $400k home, you’d need $40,000 upfront. This makes homeownership more accessible but leads to higher long-term costs.

-

5% down – Putting 5% down on a $400,000 home requires $20,000 cash. This lower down payment results in higher monthly payments and usually requires PMI.

-

3% down – Programs like FHA loans allow down payments as low as 3%, which is $12,000 on a $400k house. This gets you into homeownership faster but with more carrying costs.

The down payment directly impacts your mortgage amount, monthly payment, and total interest paid over the life of the loan. In general, a 20% down payment is best if you can afford it, while 10% down is a reasonable middle ground.

How Much Income You Need

Mortgage lenders generally want your total monthly debt payments, including the future house payment, to be less than 43% of your gross monthly income. Known as your debt-to-income ratio, staying under 43% shows you can afford the mortgage.

For a $400k home with 20% down and a 30-year loan at 6.5% interest, the estimated monthly mortgage payment is around $2,348. Assuming you have $1,000 in other monthly debts, your total monthly obligations are roughly $3,348.

To keep your debt ratio under 43% with these factors, you’d need a minimum gross monthly income of around $7,787 to comfortably afford the $400k home. Of course, a higher income provides more financial breathing room.

Tips for Affording a $400k House

If your current finances make a $400k home seem out of reach, there are steps you can take to boost your home buying ability:

-

Save aggressively for a down payment – Set a monthly savings goal and stick to it religiously. Shoot for 20% down if possible.

-

Pay down debts – Reduce credit card balances and other debts to lower your DTI ratio.

-

Increase your income – Consider taking on a side job or finding a higher-paying position.

-

Improve your credit – Good credit scores lead to lower mortgage rates, saving you money.

-

Lower other costs – Cut back discretionary spending to free up more cash for housing.

-

Choose lower-priced homes – Widen your search to include less expensive properties to reduce the down payment and mortgage needed.

With smart planning, financial discipline, and responsible borrowing, a $400,000 home can absolutely be within your reach. Connect with a mortgage professional to assess your situation and start mapping out a path to homeownership.

USDA Loan – 0% Down

Minimum Down Payment (%): 0%

Minimum Down Payment on a $400k House ($): Zero Down Payment

Minimum Credit Score: 580 to 620

The U.S. The Department of Agriculture offers USDA loans to promote homeownership in eligible rural areas for low- and moderate-income buyers. Income limits vary by region and the number of occupants in your home, but you’ll generally need to make less than 115% of your area’s median income — about $110,000 per year in most areas.

USDA loans typically have low interest rates because they’re guaranteed by the federal government. Mortgage insurance is technically not required, but you do have to pay an upfront “guarantee fee” of 1% and an annual fee of 0.35% of your total loan.

It’s important to note that the maximum size of a USDA loan in most areas of the country may be well under $400,000 due to income and debt-to-income (DTI) ratio limits. This means you may need to put money down to buy a $400k house with a USDA mortgage.

Ways to Reduce Closing Costs

Thankfully, several strategies can help alleviate the burden of paying for closing costs if youre already struggling to put together a sizable down payment.

Seller concessions are credits that a property seller agrees to give to you at closing. While a seller could grant concessions in any scenario, youre more likely to find them in a buyers market or with properties that are more difficult to sell.

You can use seller concessions to cover your closing costs, including lender discount points, but they cannot be applied toward your down payment or reserves.

Some lenders may be willing to offer you lender credits — funds that can be used for your closing costs — in exchange for charging a slightly higher interest rate on your mortgage. Lender credits are the opposite of discount points.

You cant use lender credits for your down payment or required reserves. Still, they can be an excellent tool for freeing up cash that you’d otherwise need to spend on the fees associated with closing.

Lenders will typically allow you to use funds gifted to you from a family member or other related individual to cover the costs of purchasing a home. These gifts can be applied to your closing costs or down payment and can even be used to satisfy required reserves.

Down payment gifts differ from gifts of equity, which involve a relative gifting you a portion of the home’s equity in lieu of cash. A gift of equity can count toward your down payment.

How Much Income You Need for a 400k Home (Mortgage Broker Insider) #mortgage #realestate

FAQ

How much do I need down for a 400k house?

| Loan Type | Minimum Down Payment (%) | Minimum Down Payment ($) |

|---|---|---|

| Conventional 97/HomeOne Loan | 3% | $12,000 |

| HomeReady/Home Possible Loan | 3% | $12,000 |

| FHA Loan | 3.5% | $14,000 |

| Conventional Loan (5%) | 5% | $20,000 |

What income do you need for a 400k house?

To afford a $400,000 house, you typically need an annual income between $100,000 to $125,000, which translates to a gross monthly income of approximately $8,333 to $10,417. However, this is a general range, and your specific circumstances will determine the exact income required.

How do people afford 400k houses?

It’s certainly conceivable that with a large enough down payment, someone with a $100,000 annual income could afford a $400,000 home according to the 28% rule. A caveat here is that the 28% rule dictates taking your full housing payment into account, meaning principal, interest, taxes, and insurance.

How much would a payment be on a $400,000 home?