This is a great question, and it’s good to hear that you’re taking steps to get your finances in order and take care of these collection accounts. Unfortunately, I don’t think what the collector is suggesting will work. The credit bureaus are unlikely to remove the paid collection account if it is legitimately incurred. They will only remove an item from your credit report if it cannot be verified accurately.

How To Negotiate A Pay To Delete Contract

Negotiating a pay to delete contract with a debt collector can help remove negative items from your credit report However, it is important to understand what pay to delete is, why it rarely works, and how to try negotiating a pay to delete agreement properly This comprehensive guide will explain everything you need to know about pay to delete contracts.

What Is A Pay To Delete Contract?

A pay to delete contract is an agreement between a consumer and a debt collector. The consumer agrees to pay a portion or all of the debt owed to the collector. In exchange, the collector agrees to remove the debt from the consumer’s credit report. This can help improve credit scores quickly by eliminating negative items.

Pay to delete contracts provide a fast way to boost credit. Unpaid debts stay on credit reports for 7 years. Settling through pay to delete can erase the negative mark years earlier. Many consumers pursue pay to delete arrangements to avoid waiting out the 7-year period.

Why Pay To Delete Rarely Works

While pay to delete seems ideal in theory, it rarely works in practice. The Fair Credit Reporting Act (FCRA) requires credit bureaus to report information accurately. Debts legally incurred and sold to collectors are considered accurate information. Removing legitimate negative items violates the FCRA.

Most collectors avoid blatantly violating the FCRA. If caught, they face severe penalties, including losing access to credit reports. Few collectors are willing to risk their business by deleting valid debts. Many instead make vague verbal promises they don’t intend to fulfill.

Some collectors may temporarily remove accounts, hoping consumers won’t notice when they reappear. Others string consumers along by falsely promising the consumer can dispute the item later. In most cases, debts properly validated and paid will remain on credit reports regardless.

The only accounts typically deleted are those that cannot be verified and validated by the collector. If you dispute a debt’s validity and the collector cannot prove it’s yours, it may get removed. However, collectors rarely agree upfront to delete validated debts in writing.

How To Try Negotiating Pay To Delete

While pay to delete rarely succeeds, you can still try negotiating with ethics and realistic expectations. Here are some tips for attempting to negotiate a pay to delete agreement:

-

Get any proposed agreement in writing. Verbal promises often go unfulfilled.

-

Negotiate only with original creditors you trust or confirmed debt owners. Avoid shady collectors with no proof of debt ownership.

-

Make sure the debt is valid by requesting validation before paying anything. Never pay an unverified debt.

-

If the debt is valid, start by asking for goodwill deletion based on financial hardship. Some creditors may empathize with your situation.

-

Propose a reasonable lump sum settlement if goodwill deletion is refused. Avoid lowball offers that may offend collectors.

-

Make your request politely yet firmly. Explain how the negative mark hurts your financial recovery efforts.

-

If the collector agrees, get the arrangement in writing before paying. Include specifics like payment timeline and deletion date.

-

Only make agreed payments after the item gets deleted, not before. Verify deletion by checking your credit reports.

-

If the collector reneges, complain to the Consumer Financial Protection Bureau and their state regulator. But expect no recourse.

What To Do If Pay To Delete Fails

More often than not, pay to delete negotiations fail. Collectors typically refuse deletion requests yet demand full payments. Consumers who expected deletions often feel cheated and frustrated.

If your attempts to negotiate deletion fail, you still have options:

-

Paying in full shows as “paid” on your credit report and stops collections calls. The account remains but no longer shows an outstanding balance.

-

Settling for less than owed also displays as “settled” on your report. The status update helps slightly, though not as much as deletion.

-

If the statute of limitations has expired, request the collector stop contacting you. Time-barred debts remain on reports but become uncollectible.

-

Dispute unverified debts that collectors cannot validate. Debts proven fraudulent get removed.

-

Wait out negative items. Accounts fall off reports approximately 7 years from the first delinquency date.

-

Build positive credit history to offset old debts. Consistent on-time payments show you now manage credit well.

Alternatives To Pay For Delete Agreements

As pay to delete often fails, it’s best to consider alternatives that provide guaranteed improvements:

-

Goodwill letters request account closure or forgiveness based on extenuating circumstances. Creditors sometimes grant them if you explain financial hardships.

-

Debt validation requires collectors prove account ownership. Unverified debts get deleted.

-

Debt settlement pays a lump sum equaling a percentage of the balance owed. You save money while closing accounts.

-

Debt management plans enroll accounts with creditors to secure lowered interest rates and reduced monthly payments.

-

Consumer credit counseling offers budgeting assistance and negotiates resolutions tailored to your financial situation.

-

Bankruptcy eliminates or discharges eligible debts entirely in exchange for liquidating assets.

-

Waiting for negative items to fall off reports takes patience but costs nothing.

-

Continually paying current obligations on time builds your credit score back up over time.

Key Takeaways

-

Pay to delete contracts exchange payment for credit report deletion but rarely succeed due to collector risks.

-

Validated debts legally have to remain on credit reports when paid, limiting deletion agreements.

-

Alternatives like goodwill letters, debt settlement, and credit counseling provide reliable improvements.

-

If your pay to delete request gets denied, focus on repayment plans, credit building, and letting time pass.

Pay to delete agreements seem alluring but have major limitations in practice. Arm yourself with realistic expectations before approaching collectors with deletion requests. With patience and perseverance, you can rebuild credit without relying on unlikely deletions. Carefully weigh all your options and understand your rights when seeking solutions.

Why pay for delete rarely works for debt collections

Pay for delete is a relatively old practice in the world of debt collection. The collector agrees to remove a collection account from your credit report in exchange for full or partial payment. In theory, that eliminates the credit damage caused by having that account on your report. You get immediate relief instead of waiting seven years for the account to fall off your credit report after the penalty expires.

The problem is that this practice technically violates federal law under the Fair Credit Reporting Act. That law requires that a consumer’s credit history must be reported accurately, for better or worse. Credit bureaus are required to ensure that consumer reports are accurate. An item can only be removed if it’s an error or mistake.

What is pay for delete?

Pay for delete results from a negotiation between a debtor and debt collector. The latter agrees to a partial payment of the overall debt from the former in exchange for having the debt collection account removed from the debtor’s credit report.

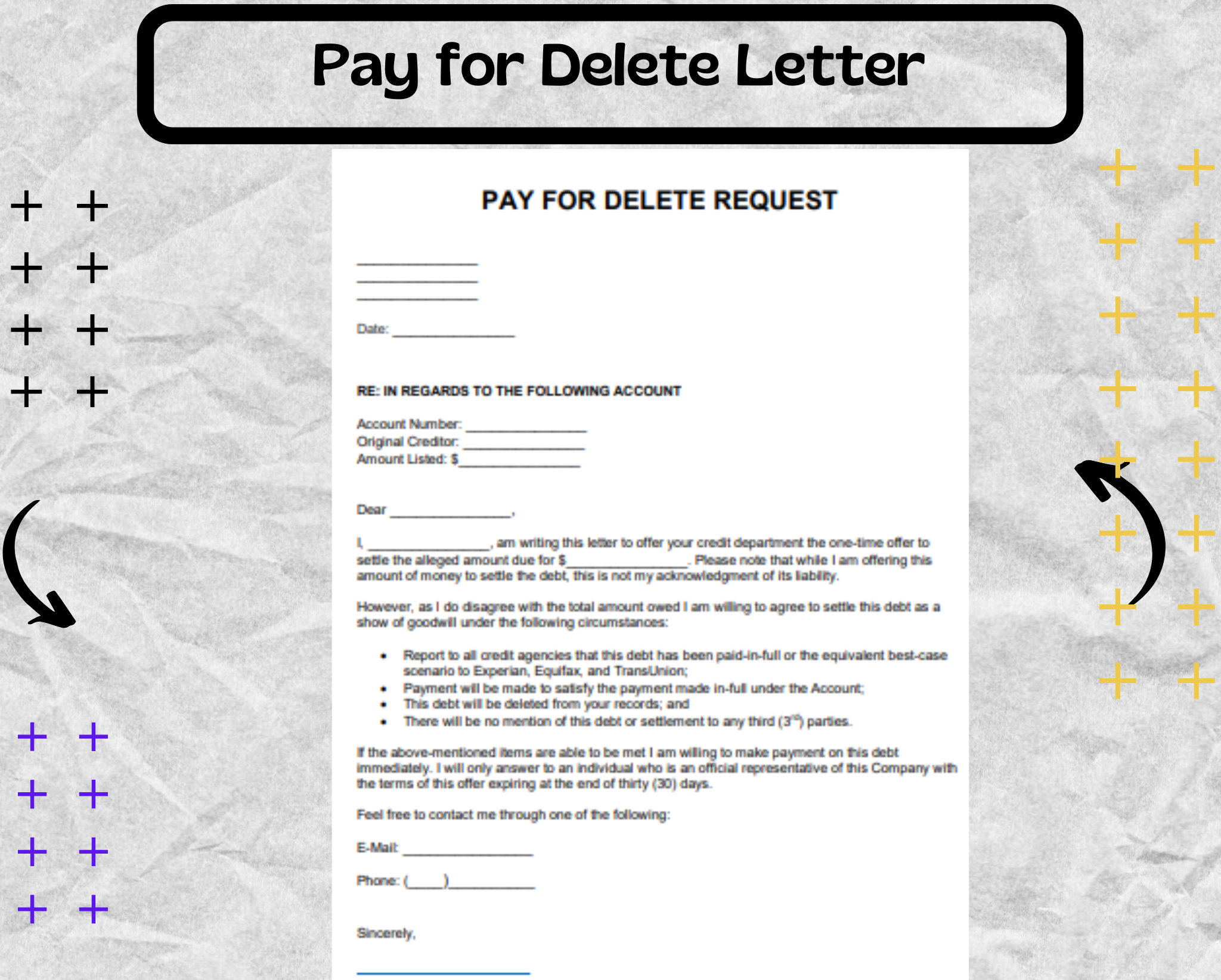

It’s imperative to have the request and debt collector’s response in writing. Debt collectors may deny the pay-for-delete request, demanding the amount be paid in full before removing the negative item from your credit report. Pay for delete is possible, in theory, but there may be some caveats.

5 things a debt collector will tell you when you ask for a “pay for delete” agreement

FAQ

How do you negotiate a pay to delete?

I am (your full name), and I have an account with you (account number). I am reaching out today with a request to pay (dollar amount) in exchange for removing the debt from all credit reporting agencies. If an agreement is reached, I will pay this amount by (date of payment).

Do pay to delete letters actually work?

Pay-for-delete letters are legal, but creditors are not obligated to accept them. While the practice isn’t illegal, it is discouraged by credit reporting agencies, and creditors may refuse to remove accurate negative information due to agreements with credit bureaus.

What percentage should I offer to settle debt?

Does a pay for delete hurt your credit?

In turn, these agencies widely discourage pay-for-delete practices, as the approach can compromise the integrity and accuracy of credit reporting.Jan 2, 2025