So, you’re eager to pay off your mortgage early? That’s a great financial goal to set for yourself!

Not only is there huge freedom in being completely debt-free and living in a paid-for house, but it’s also a great way to build wealth—getting rid of your house payment leaves you with a ton of extra money each month to save for retirement. In fact, the average millionaire pays off their house in just 10.2 years.1

But even though you’re dead set on ditching your mortgage ahead of schedule, you probably have one major question on your mind: How do I pay off my mortgage faster? That’s why we’re going to walk through exactly how to pay off your mortgage early so you can reach your goal and become a debt-free homeowner.

Paying off a $300k mortgage in just 5 years may seem like an impossible feat, but with strategic planning and discipline, it is achievable for some homeowners.

Why Pay Off a Mortgage Early?

There are several benefits to paying off your mortgage early:

-

You’ll save a significant amount in interest payments On a $300k mortgage, you could potentially save over $100k in interest by paying it off in 5 years instead of 30 years

-

You’ll build home equity faster. With your mortgage paid off, 100% of your home’s value will be equity.

-

You’ll own your home free and clear. This gives you financial flexibility and peace of mind.

-

Your monthly cash flow will improve without a mortgage payment. This gives you more money to save or invest.

However, paying off a mortgage early isn’t for everyone. Make sure you have an emergency fund, are saving sufficiently for retirement, and don’t have higher interest debt before making extra mortgage payments.

How Much Will I Need to Pay Each Month?

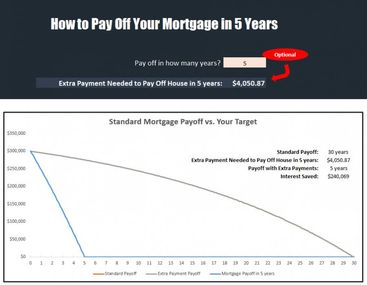

To pay off a $300k mortgage in 5 years, you’ll need to pay approximately $5,550 per month. This is calculated by taking the mortgage amount, dividing it by the number of months, and adding in the regular monthly payment.

For example, with a 30 year $300k mortgage at 5% interest, the monthly payment is around $1,610.

$300,000 mortgage / 60 months = $5,000

$5,000 + $1,610 regular payment = $5,550 total monthly payment

This is a significant increase from the normal payment. But it can be done by cutting expenses, increasing income, and making strategic sacrifices.

Steps to Pay Off a $300k Mortgage in 5 Years

Here is a step-by-step guide to paying off a $300k mortgage in 5 years:

-

Make a budget and cut discretionary spending

- Review expenses and cut back on dining out, entertainment, vacations, etc. Find an extra $500+ per month here if possible.

-

Increase your income

- Consider getting a side gig or asking for a raise at work. An extra $1,000 per month from a side hustle could make a big dent.

-

Make biweekly mortgage payments

- This results in 26 half payments per year rather than 12 monthly payments. Over 5 years, you’ll make 2-3 extra payments.

-

Pay half your annual bonus or tax refund toward the mortgage

- Any extra lump sums should be directed toward principal.

-

Downsize your home

- Consider selling your current home and downsizing to reduce the mortgage balance.

-

Refinance your mortgage

- See if you can refinance to a lower rate. This will allow more money to go toward principal.

-

Use windfalls wisely

- Put any money gifts, insurance payouts or legal settlements toward paying down principal.

-

Get an accountability partner

- Share your goal with a friend or family member. They can help you stay motivated and on track.

-

Celebrate small milestones

- Paying off $100k is an awesome achievement! Recognize your progress.

-

Visualize being mortgage free

- Keep your eye on the prize. In 5 years you’ll have financial freedom!

With extreme focus and discipline, paying off a $300k mortgage in 5 years is challenging but feasible. Follow the steps above to make steady progress each month. You’ll be mortgage free before you know it!

Refinance (or pretend you did).

Another way to pay off your mortgage early is to trade it in for a new loan with a lower interest rate or a shorter term (or both)—like a 15-year fixed-rate mortgage. Let’s see how this would affect our earlier example—a 30-year $240,000 mortgage with a 7% interest rate.

If you kept the 30-year mortgage and made all your payments on schedule for those three decades, you’ll pay about $335,000 in total interest over the life of the loan. But if you switch to a 15-year mortgage with a lower rate of 6.5%, you’ll save close to $200,000—and you’ll pay off your home in half the time!

Sure, a 15-year mortgage will come with a bigger monthly payment. But if you can comfortably fit it within your monthly budget (meaning the payment is at or below 25% of your take-home pay), it’ll totally be worth it. And don’t forget, you’ll likely have boosted your income or lowered your cost of living from the time you first took out your mortgage—in that case, you’d definitely be able to handle the bigger payment.

If you want to refinance to a mortgage you can pay off fast, talk to an expert at Churchill Mortgage. Our team at Ramsey has worked with Churchill Mortgage for years, and their mortgage experts will show you the true cost—and savings—of each loan option. They’ll also coach you to make the best decision based on your budget and goals.

If you already have a low interest rate on a 30-year loan, don’t worry about refinancing. Go ahead and treat your 30-year mortgage like a 15-year mortgage by upping your monthly payment.

Downsizing your house may sound like a drastic step. But if you’re determined to pay off your mortgage faster, consider selling your larger home and using the profits to buy a smaller, less expensive house.

With the profits from selling your bigger house, you may be able to pay 100% cash for your new home. But even if you do have to get a small mortgage, you’ll still reduce your debt and wind up with lower payments.

Remember though: Your goal is to get rid of that new mortgage as quickly as possible. So use the smaller balance and lower payments you get from downsizing to accelerate paying off your home. This isn’t an excuse to pocket money in the short-term and delay your payoff.

If you think downsizing your home makes sense for your situation and you’re ready to get the process started, your first step should be hiring a top-notch real estate agent who can help you sell your current house and buy a new one.

You can find one in your area through our RamseyTrusted program, which matches you with pros our team has vetted to make sure they understand how important it is to buy a home you can afford. They won’t pressure you to consider homes that’ll bust your budget.

Make extra room in your budget.

You may have read that last section and thought, But I don’t have any extra money to put toward my house payments! Hang on—you can probably find more money in your budget each month than you realize.

Now, if you aren’t already making a budget every month, start there. Write down your income, list your expenses, subtract your expenses from your income to make sure you aren’t overspending, then track your spending during the month to make sure you’re staying on target.

If you are living on a budget—or once you make your first one—here are some adjustments you can make to free up money for paying off your house early.

- Lower your grocery budget. Chances are, groceries are one of the biggest line items on your budget aside from housing—especially if you have a family. So think about some ways to cut back, like changing stores or shopping sales and in-season produce.

- Stop eating out so much. Okay, I’ll admit this is a tough one for me because I love eating out. But going to restaurants is always more expensive than cooking at home—sometimes a lot more expensive. Cooking at home just 2–3 more times per week can save you a ton in the long run.

- Do an insurance coverage checkup. An independent insurance agent who can shop rates from multiple providers may be able to get you a cheaper price than what you’re currently paying for your coverage. You can start that process by connecting with a RamseyTrusted pro.

- Cancel some subscriptions. These days, it’s super easy to rack up more subscription services than you actually use. Figure out which streaming services you can live without, cancel them, and put the extra cash toward your mortgage.

- Cut back on online shopping. I know, I know . . . Online retailers like Amazon are super convenient with two-day shipping and one-click ordering, but all those orders can add up fast. And if we’re really honest with ourselves, we probably know we don’t need all that stuff in our digital cart. (Dang it!) Cutting back will give you margin to make bigger payments on your mortgage each month.

How I Paid Off My Mortgage in 5 Years!

FAQ

How to pay off a $300,000 mortgage in 5 years?

- Setting a Target Date. …

- Making a Higher Down Payment. …

- Choosing a Shorter Home Loan Term. …

- Making Larger or More Frequent Payments. …

- Spending Less on Other Things. …

- Increasing Income.

Is it possible to pay off a mortgage in 5 years?

Paying off your mortgage in 5 to 7 years is possible with the right strategies and commitment. Making bi-weekly payments can significantly reduce your loan term. Refinancing to a shorter-term loan can accelerate payoff but may increase monthly payments.

What happens if I pay an extra $500 a month on my mortgage?

What is the average monthly payment for a $300000 mortgage?

Expect to pay about $1,798 to $2,201 per month for a $300,000 mortgage with a 30-year loan term, depending on your interest rate and other factors.