Coming up with a down payment is one of the most challenging parts of buying a home. The typical homebuyer puts down 15% at the closing table, according to the National Association of Realtors (NAR), which often translates to tens of thousands out of pocket. For a $350,000 home, that’s a $52,500 down payment.

But can you get a loan for a down payment if you don’t have the cash? The answer is yes, and your options include tapping your existing home equity, borrowing from your retirement savings or asking a relative or friend for a private loan.

Getting enough money for a down payment is one of the biggest hurdles for many prospective homebuyers. With home prices continuing to rise across the country, coming up with even just 3-5% down can mean saving tens of thousands of dollars. For first-time homebuyers especially, this can feel like an impossible task.

But there are many options for securing down payment funds beyond just saving over time Here are some of the most common ways to get money for a home down payment

Tap Home Equity

If you currently own a home and have built up equity, you may be able to tap into it for your next home’s down payment. A cash-out refinance or home equity loan converts your equity into cash that can then be used to fund a down payment. Just be sure you can afford the additional monthly payment this would require.

Borrow from Retirement Savings

You can take out a loan or even make a withdrawal from certain retirement accounts, like a 401(k) or IRA, to use for a home down payment. This does put your retirement savings at some risk, so be sure to understand the rules, limitations, and payback requirements before borrowing from retirement funds

Ask Family for a Gift

It’s common for first-time homebuyers to get down payment support from family. As long as it is documented as a gift with a gift letter, this money does not need to be repaid. Be transparent with your lender so they know where the funds are coming from.

Take Out a Personal Loan

Unsecured personal loans can provide funds that you can use for whatever you want, including a home down payment. However, this will increase your debt obligations so be sure you can manage the additional monthly payment. Personal loans for down payments may also raise eyebrows with some lenders.

Use Down Payment Assistance Programs

State and local governments, along with some private organizations, offer down payment assistance in the form of grants, forgivable loans, or tax credits. Eligibility requirements vary but these programs aim to help first-time and lower-income buyers overcome the down payment hurdle.

Get a Lender-Funded Grant

Some mortgage lenders offer grants and low or no interest second loans, funded out of their own marketing budgets, that act as down payment and closing cost assistance. These are essentially giveaways aimed at winning new mortgage business, so be sure to shop lenders and ask about these types of programs.

Delay Purchasing

If your savings are falling short, waiting and saving longer may be your best option. This allows you to build up a down payment, pay off debts, and improve your credit – all of which will put you in a better position when you do buy. Down payment savings grow faster once you have a set monthly amount automatically deposited.

Consider Low or No Down Payment Loans

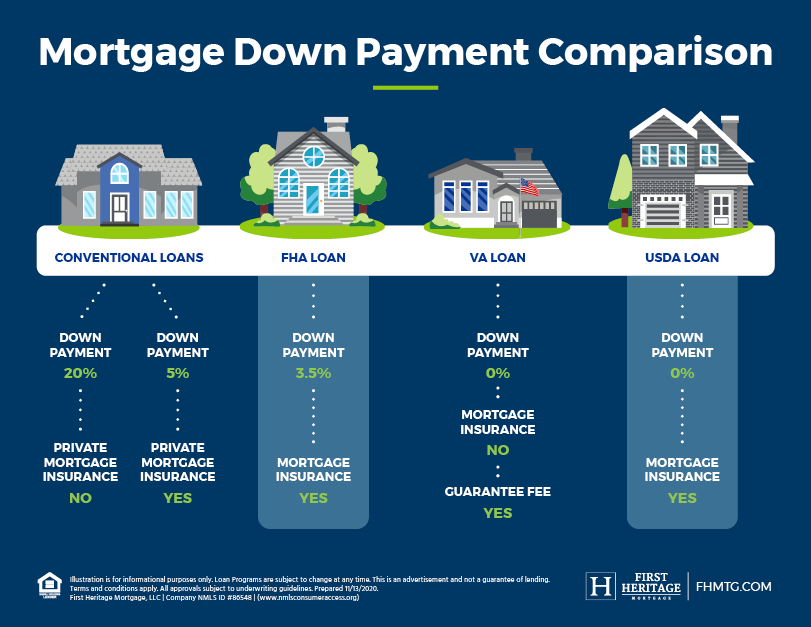

VA and USDA loans allow qualified buyers to purchase with 0% down. FHA loans only require 3.5% down. Conventional 97 loans from Fannie Mae and Freddie Mac allow 3% down. These can be great options if you have limited savings but be aware you’ll pay higher monthly mortgage insurance until you reach 20% equity.

Move to a Cheaper Area

While not ideal for everyone, purchasing a home in a lower-cost region can significantly reduce the down payment funds needed. Even different zip codes in the same metro area can have dramatic price differences. Widening your home search radius can open up more affordable opportunities.

Negotiate with the Seller

In some cases, buyers are able to negotiate with the seller to have certain closing costs covered or get the sales price lowered to decrease the down payment amount needed. This works best in buyer’s market conditions, but it never hurts to make an offer and ask.

Hold a Down Payment Fundraiser

Crowdsourcing down payment funds from friends and family is something many first-time buyers are now doing. By making the request public and structured, rather than just asking relatives, this can widen the net for contributions. Just be sure to document funds are gifts, not loans.

The most important thing is having a solid savings habit and budget that allows you to steadily build up your down payment fund over time. But if your timeline necessitates a quicker path to down payment funds, utilizing one or more of the options above can help you achieve homeownership sooner. Be sure to consult trusted financial and real estate professionals to determine the best approach for your unique situation. With persistence and a prudent plan, the down payment funds you need will be within reach.

6 ways to borrow money for a down payment

If you haven’t saved up enough to make a down payment on a new home, consider choosing from one of the six borrowing options below. But first, check your budget to ensure that an extra monthly payment wouldn’t put a strain on your finances.

Tap your retirement savings

Your retirement savings should never be used to bankroll big-ticket purchases. However, if your path to the golden years includes homeownership, you may want to use some of your savings to buy a house.

If you have a 401(k), you may be able to take out a 401(k) loan for your down payment. You repay the loan over time, and you can typically borrow up to 50% of your vested account balance or $50,000 (whichever is less), according to the IRS. However, if you were to leave your job for any reason, you may have to pay back the outstanding balance in a short amount of time. Your financial planner or accountant can help you determine if taking a 401(k) loan or distribution is right for your situation.

What’s the Best Way to Save for a Mortgage Downpayment?

FAQ

Can I borrow money for a down payment?

How do I gather money for a down payment?

- Traditional Savings. …

- 401(k) Loans or Withdrawals. …

- Gifts from Family or Friends. …

- Income Tax Refunds. …

- Grant Programs and Assistance. …

- Refinancing an Auto Loan. …

- Lender-Paid and Seller-Paid Costs. …

- Other Creative Strategies.

What if I don’t have enough money for a down payment?

The two most popular options are FHA loans and VA loans, both of which allow you to finance your home without making a down payment. A USDA loan is one that is guaranteed by the US Department of Agriculture. USDA construction loans and USDA loans are available to support development in rural and suburban regions.

How to find money for a downpayment?

Sometimes local non-profit or government organizations can offer you a second mortgage on special terms to replace a down payment. Some federal programs are also available. For eligible servicemembers or family members, Department of Veterans Affairs (VA) loans do not require a down payment.

How do I save for my down payment?

Tips and Tricks to Save for Your Down Payment 1. Determine Your Expected Down Payment and Timeframe 2. Shrink Your Required Down Payment With a Special Loan 3. Take Advantage of National Down Payment Assistance Programs 4. Look Into State-Specific Down Payment Assistance and Resources 5. Pay Off Outstanding Credit Card Debt 6.

How do I get Down Payment Assistance?

Your real estate agent, mortgage broker or lender are also great resources for finding down payment assistance programs. Get pre-qualified for a home loan to get your budget conversation started. 3. Formally apply for down payment assistance

How do I get enough money for a down payment?

To gather enough money for a down payment, consider saving consistently in a high-yield savings account, exploring down payment assistance programs available in your area, receiving a financial gift from family, or tapping into retirement accounts if applicable.

How can I reduce my down payment?

1. Determine Your Expected Down Payment and Timeframe 2. Shrink Your Required Down Payment With a Special Loan 3. Take Advantage of National Down Payment Assistance Programs 4. Look Into State-Specific Down Payment Assistance and Resources 5. Pay Off Outstanding Credit Card Debt 6. Round Up and Save Your Change 7.

Where can I get a home loan for a down payment?

Most states and many counties and cities offer grants and no-interest loans to help home buyers pay for down payments and closing costs. Down payment assistance most commonly comes through state housing finance agencies. It can also come from cities, counties, nonprofits, lenders and even some employers.

How do I qualify for down payment assistance?

There are also lenders that specialize in down payment assistance programs who work with state or local housing agencies, or they may offer their own down payment assistance programs. To qualify for down payment assistance, you must have not owned a home in the past three years.