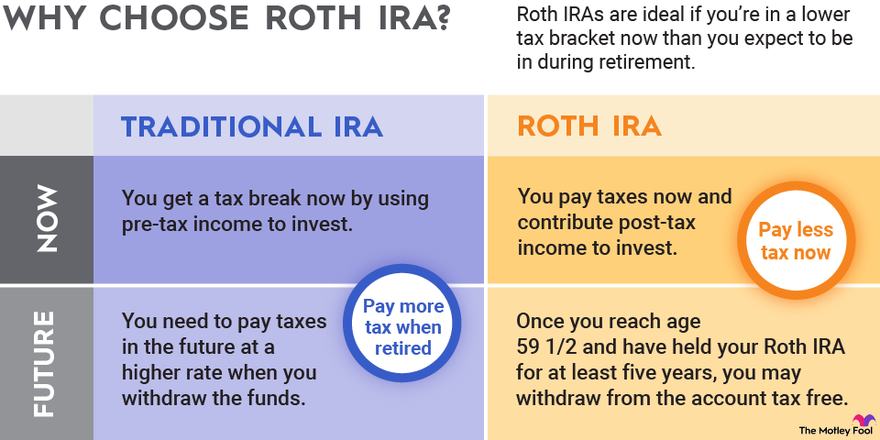

The main difference between a traditional and Roth IRA is how and when your money is taxed.

The products shown on this page are mostly or entirely from our advertising partners. They pay us when you click on one of their links and then do something on our site. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and heres how we make money.

The investing information provided on this page is for educational purposes only. NerdWallet, Inc. does not provide advisory or brokerage services, and it does not tell investors whether to buy or sell certain stocks, bonds, or other investments.

An IRA is one of the most common retirement savings accounts, but some people may need to decide between two types: the Roth IRA and the traditional IRA.

If youre not sure which one is right for you, consider your age, annual income, tax brackets in retirement and whether you want a deduction for contributing this year.

Are you torn between opening a Roth IRA or traditional IRA? Maybe you’re wondering if having both is overkill or actually a smart move? Well you’re not alone in this financial conundrum!

As a spoiler, I’ve spent a lot of time researching this subject and it does make sense to have both types of IRAs. But it ain’t a one-size-fits-all situation, folks. Let’s look at why tax diversification might be the best thing you can do for your retirement.

The Basic Differences: Roth vs. Traditional IRA at a Glance

What makes these two retirement accounts different? Let’s go over them again before we talk about whether it makes sense to have both:

| Feature | Roth IRA | Traditional IRA |

|---|---|---|

| Tax benefits | No immediate tax break; tax-free withdrawals in retirement | Potential tax deduction now; taxable withdrawals in retirement |

| Income limits | Phases out at higher incomes (2025: $150,000-$165,000 single) | No income limits for contributing, but deductibility may be limited |

| Required distributions | No RMDs during your lifetime | RMDs required at age 73 (increasing to 75 in 2033) |

| Early withdrawals | Contributions can be withdrawn anytime tax-free | Withdrawals before 59½ typically face taxes plus 10% penalty |

| 2025 contribution limits | $7,000 ($8,000 if 50+) combined across all IRAs | $7,000 ($8,000 if 50+) combined across all IRAs |

Why Having Both IRAs Isn’t Crazy Talk

1. Tax Diversification is a Real Thing

Having money in both pre-tax (traditional) and after-tax (Roth) accounts gives you options in retirement. It’s like not putting all your eggs in one tax basket.

“Being able to draw money from both types of accounts can give you more freedom in managing withdrawals and may even lower your tax bill in retirement,” says Walter Updegrave of RealDealRetirement.com.

2. Hedge Against Future Tax Uncertainty

None of us has a crystal ball to predict future tax rates. Will they be higher or lower when you retire? Who knows!

- If taxes go UP: Your Roth IRA withdrawals stay tax-free

- If taxes go DOWN: Your traditional IRA withdrawals get taxed at lower rates

By having both, you’re essentially making a split bet on future tax policy. Smart, right?

3. Flexibility in Retirement Income Planning

When I reach retirement, I want options. With both accounts, I can take money out of either one strategically, depending on how my taxes look that year.

For example, if I have a year with unusually high income from other sources, I might take tax-free withdrawals from my Roth. In a lower-income year, I might pull from my traditional IRA and pay taxes at a lower rate.

When Does Having Both IRAs Make the Most Sense?

Your Income Fluctuates

If your income bounces around from year to year, you might benefit from contributing to different accounts in different years.

- In high-income years: Focus on traditional IRA (if deductible) to reduce your current tax bill

- In lower-income years: Pump money into your Roth when you’re in a lower tax bracket

You’re Mid-Career With Decent Savings Already

If you already have substantial money in one type of account, diversifying into the other type can be strategic. Many folks have been contributing to traditional 401(k)s for years, so adding a Roth IRA brings balance to their retirement portfolio.

You Like Tax Optimization

Let’s be honest – if you’re the type who gets excited about tax planning (no judgment!), having both accounts gives you more levers to pull during retirement.

The Math: Is a Roth Really Better?

Many articles claim the Roth IRA is almost always the better choice, but that’s not necessarily true.

A NerdWallet study found that while Roths often come out ahead, traditional IRAs can win in many scenarios too. It all depends on:

- Your current tax bracket vs. your retirement tax bracket

- Whether you invest the tax savings from traditional IRA contributions

- How efficiently you invest in taxable accounts

Here’s where things get interesting. If you contribute $5,500 to a Roth IRA versus $5,500 to a traditional IRA, you’re not making an equal comparison! Why? Because the Roth contribution costs you more in pre-tax dollars.

If you’re in the 25% tax bracket, that $5,500 Roth contribution actually costs you $7,333 in pre-tax income ($7,333 minus $1,833 in taxes = $5,500). That’s why the Roth often appears to win in oversimplified comparisons.

Practical Strategy: How to Use Both IRAs Effectively

1. Keep Track of Contribution Limits

Remember, the 2025 IRA contribution limit is $7,000 ($8,000 if you’re 50+) COMBINED across all your IRAs. So if you put $4,000 in your traditional IRA, you can only put $3,000 in your Roth that year.

2. Consider Your Current vs. Future Tax Brackets

- If you expect to be in a HIGHER tax bracket in retirement → Favor the Roth IRA

- If you expect to be in a LOWER tax bracket in retirement → Favor the traditional IRA

- Not sure? → Split your contributions between both!

3. Watch Income Limits

For 2025, Roth IRA contributions phase out between:

- $150,000-$165,000 (single filers)

- $230,000-$246,000 (married filing jointly)

Traditional IRA deductibility (if covered by a workplace plan) phases out between:

- $79,000-$89,000 (single filers)

- $126,000-$146,000 (married filing jointly)

4. Start Early if Possible

The sooner you start contributing to either type of IRA, the more time your money has to compound and grow. If you’re young, you might initially focus more on Roth contributions since your tax rate is likely lower now than it will be later in your career.

Common Questions People Ask Me About Having Both IRAs

“Can I really have both types of IRAs at the same time?”

Absolutely! The IRS has no problem with you maintaining both a traditional and Roth IRA simultaneously. Just remember that your total contributions across all IRAs can’t exceed the annual limit.

“Won’t it be confusing to manage two different accounts?”

It’s definitely something to consider. If you open both with the same broker, they’ll typically appear under the same login, which helps. But you’ll need to keep track of which is which, especially when making contributions or withdrawals.

“Should I convert my traditional IRA to a Roth?”

This is a whole other topic! Conversions can make sense in certain situations (like years with unusually low income), but you’ll owe taxes on the converted amount. Talk to a tax professional before making this move.

Real Talk: The Downsides of Having Both IRAs

I wouldn’t be giving you the full picture if I didn’t mention some potential drawbacks:

- More accounts to manage – Some folks prefer simplicity

- Potentially higher fees – Two accounts might mean double the maintenance fees

- More complex tax planning – You’ll need to be more strategic at tax time

For some people, these downsides might outweigh the benefits, and that’s totally fine! If you prefer simplicity, picking one type of IRA and sticking with it is perfectly reasonable.

My Personal Take

In my experience helping folks with retirement planning, I’ve found that having both types of IRAs makes the most sense for people who:

- Are uncertain about future tax rates

- Want maximum flexibility in retirement

- Have varying income levels throughout their career

- Enjoy optimizing their tax situation

But it’s definitely not for everyone. If you’re just starting out, focus on getting the maximum match from your employer’s 401(k) first, then consider adding an IRA (either type) to the mix.

Bottom Line: Is It Worth Having Both?

So, does it make sense to have both a Roth and traditional IRA? For many people, yes! The tax diversification and flexibility you gain can be powerful tools for retirement planning.

But remember:

- Don’t exceed annual contribution limits

- Consider your current and future tax situations

- Weigh the added complexity against the benefits

- If in doubt, consult with a financial advisor

At the end of the day, having some retirement savings is way better than none, regardless of which account type you choose. The most important thing is to start saving and investing consistently.

Disclaimer: This article is for informational purposes only and is not financial advice. Please consult with a qualified financial professional before making investment decisions.

Roth IRA vs. traditional IRA: Which one should you choose?

Most advice on the Roth IRA vs. traditional IRA topic begins with a question: Do you think your tax rate will be higher or lower in the future?.

If you know the answer to that question for sure, you should be able to pick the type of IRA that will save you the most money on taxes. If you expect to be in a higher tax bracket in retirement, consider a Roth IRA and its delayed tax benefit. If you expect lower rates in retirement, consider a traditional IRA and its upfront tax advantage.

But its hard to anticipate what your tax rate will be in retirement, particularly if youre decades away from leaving the workforce. Fortunately, there are other ways to determine whether a Roth or traditional IRA is best for you.

The biggest factor may be your eligibility: The IRS rules on contributions may make the decision for you. Your income will determine:

- If youre eligible to contribute to a Roth. At higher incomes, you may not be. (View the current Roth IRA contribution and income limits. ).

- When you file your taxes this year, you can deduct the amount you put into a traditional IRA. You or your spouse can only deduct income from a traditional IRA if they have access to a workplace savings plan like a 401(k). (See the current limits on how much you can deduct from your traditional IRA income.) ).

Remember that you can put money into both a traditional and a Roth IRA in the same year, as long as the total amount doesn’t go over the maximum contribution limit, which for 2025 is $7,000 ($8,000 for people age 50 and up).

» Want a Roth but don’t qualify? How a backdoor Roth IRA might allow you to get one anyway.

The key difference between Roth and traditional IRAs

The main difference between a Roth IRA and a traditional IRA is how and when you get a tax break.

Contributions to traditional IRAs are tax-deductible in the year they are made, but withdrawals in retirement are taxable as ordinary income. In comparison, contributions to Roth IRAs are not tax-deductible, but qualified withdrawals in retirement are tax-free.

While you can have both types of IRAs, deciding whether to contribute to a traditional IRA or a Roth IRA might come down to other differences between the accounts.