Understanding your debt-to-income (DTI) ratio is crucial when applying for a mortgage. This ratio compares your monthly debt payments to your monthly income and helps lenders determine how much house you can afford. But what exactly gets included in the DTI calculation? Specifically, does your escrow payment for taxes and insurance count?

The short answer is yes – escrow is part of your total monthly mortgage payment used to calculate DTI But the impact escrow has on your ratio depends on several factors Let’s take a closer look at how escrow accounts work and their effect on mortgage affordability.

What is an Escrow Account?

An escrow account is a special account setup by your mortgage lender to pay property taxes and insurance on your behalf.

Here’s how it works

-

A portion of your monthly mortgage payment goes into the escrow account

-

The lender uses these funds to pay your property taxes and homeowner’s insurance premiums when they are due

-

Your escrow payment amount is determined by estimating your annual tax and insurance costs, then dividing by 12 to get a monthly amount

Escrow accounts provide an convenient way to pay these essential homeownership costs. The lender manages the payments so you don’t have to worry about it.

Why Do Lenders Require Escrow?

There are a couple key reasons lenders require escrow accounts:

-

To protect their investment – By handling tax and insurance payments, the lender ensures these costs are paid on time. This prevents issues like tax liens or insurance lapses that could put their collateral (your home) at risk.

-

To determine affordability – Monthly escrow payments are factored into your DTI ratio. This gives the lender a more complete picture of your housing expenses when approving your loan.

-

To simplify homeownership – For borrowers, escrow provides a hassle-free way to pay property taxes and insurance. You don’t have to worry about tracking due dates or making separate payments.

Now let’s look at how escrow accounts specifically impact your DTI when applying for a mortgage.

How Escrow Affects Your DTI Ratio

Your DTI ratio compares your total monthly debt payments to your gross monthly income. Generally, lenders want to see your DTI below 36% to qualify for a mortgage. Escrow is included in the calculation as part of your total monthly housing expense.

Here are three ways escrow affects DTI:

1. Increases Total Housing Expense

Your escrow payment gets added to your mortgage principal/interest payment. The total is used as your “housing expense” portion of the DTI equation.

A higher escrow amount increases your total housing cost, resulting in a higher ratio.

2. Reduces Loan Eligibility

Since a higher escrow payment increases your DTI, it can impact the loan amount you qualify for. With a higher ratio, lenders may approve you for a smaller loan to keep your total monthly payments affordable.

3. Affects Interest Rates

Higher DTI ratios often mean paying higher mortgage interest rates. Lenders perceive you as a higher credit risk and charge more. Keeping your ratio low by minimizing escrow costs can help you score better rates.

What’s Included in Escrow Payments?

Standard escrow accounts include two items:

Property taxes – These vary by location and home value. Your lender will estimate taxes based on the annual property tax bill.

Homeowner’s insurance – Your lender requires a policy with adequate dwelling coverage to protect their investment. Monthly premiums depend on factors like home value, location, and coverage limits.

If you make a down payment under 20%, you may also have private mortgage insurance (PMI) included in your escrow payment. PMI protects the lender from default and typically ranges from 0.5% – 1% of the loan amount annually.

How Are Escrow Payment Amounts Determined?

Your lender will analyze your specific tax and insurance costs to estimate your escrow payment, usually following these steps:

-

Review your property tax assessment and annual insurance premium

-

Add a “cushion” to account for possible increases

-

Divide the total annual estimate by 12 to calculate the monthly escrow amount

Lenders re-evaluate your escrow each year and can adjust your payment if costs change. Having a sufficient cushion guards against payment spikes.

Can You Avoid Escrow?

Some lenders let you waive the escrow requirement, allowing you to pay taxes and insurance yourself. This avoids having the payments included in your DTI.

However, opting out has risks:

-

You must demonstrate discipline to make payments on time yourself

-

Increases can unexpectedly spike your housing costs

-

Falling behind could lead to costly penalties and damage to your credit

Overall, keeping an escrow account simplifies homeownership and provides stability to your housing budget.

Tips for Lowering Your Escrow Costs

While escrow is required, here are some tips to minimize its impact on your DTI:

-

Shop for lower insurance rates – Get quotes from multiple carriers to find the best premium. But don’t skimp on coverage.

-

Pay property taxes semi-annually – Making two smaller payments instead of one lump sum reduces your monthly escrow deposit.

-

Avoid PMI – Putting down over 20% lets you skip this additional escrow expense.

-

Ask lenders to re-calculate – Ensure your escrow payment accurately reflects your actual costs and doesn’t overestimate.

The Bottom Line

Escrow accounts are required by most lenders to pay your property taxes and homeowner’s insurance as part of your monthly mortgage payment. This convenient service simplifies homeownership, but also increases your total housing costs.

Since escrow is used to calculate your DTI ratio, minimizing its impact can help you qualify for better loan terms. Pay close attention to your tax and insurance costs during the home shopping process to keep your payments affordable.

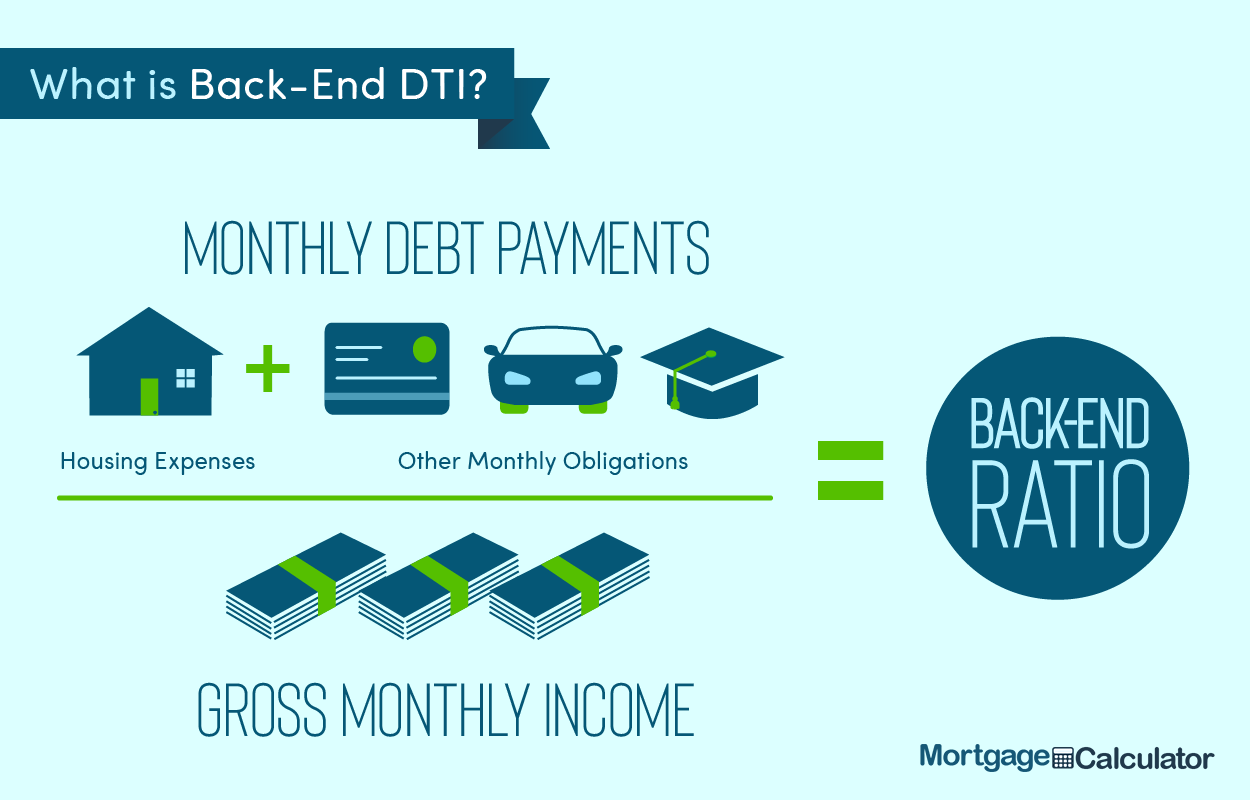

How is DTI calculated?

Lenders want to be sure you can repay your mortgage debt. So they look closely at several financial details, including your debt-to-income (DTI) ratio.

DTI is calculated by adding up your monthly debt payments and dividing them by your gross (pre-tax) monthly income.

Debts that count toward your DTI include things like:

- Home loan payments (including principal, interest, taxes, and insurance)

- Credit card debt

- Student loans

- Auto loans

- Personal loans

- Child support

- Alimony

- Any other monthly payment for debt, even if it is not listed on your credit report

This shows what percentage of your income is taken up by existing debts, and how large of a mortgage payment you could reasonably afford on top of your current obligations.

Note that non-debt payments like gas, electric, and cell phone bills are not counted toward DTI.

What DTI ratio do lenders want to see?

Lenders prefer a DTI ratio that’s within an acceptable range or below a particular threshold.

“Lenders often prefer a DTI of 43 percent or lower for conventional loans or FHA loans, and 41 percent for USDA and VA loans,” says Lawhorn.

“Some loan programs allow borrowers to exceed these limits if they meet certain qualifying criteria.”

In his experience, Trott has observed lenders being flexible with some of these limits.

“Fannie Mae and Freddie Mac back-end ratios often need to be less than 50 percent or even lower if your credit score is not as strong. FHA and VA loans can often go as high as 55 percent, depending on compensating factors such as credit, discretionary income, and liquid assets,” he says. “USDA loans usually require a 29 percent maximum on the front-end ratio and 43 percent on the back-end ratio.”

Note that a new qualified mortgage (QM) rule has resulted in lenders being more flexible about debt requirements.

“Previously, lenders were required to strictly stick to the 43 percent DTI limit,” says Lawhorn.

“But under the new QM rule, while lenders must still assess a borrower’s DTI they can take into consideration the types of debts the borrower has. And they can consider expected future income rather than sticking to a numerical calculation.”

Did your DTI come in higher than expected?

FAQ

Does DTI include escrow?

This will be your regular monthly payment if you escrow your taxes and insurance. If you don’t escrow, your lender will likely take your annual tax and insurance payments, divide them by 12, and include them as part of your mortgage payment for your DTI calculation.

What payments are not included in DTI?

- Utilities (water, garbage, electricity, gas)

- Car insurance.

- Cable and cell phone bills.

- Health insurance.

- Groceries and entertainment expenses.

Does escrow count as a mortgage payment?

An escrow account is funded through your monthly mortgage payment, making your monthly bill higher than it would be without escrow. However, this also means that you don’t have to pay your taxes or insurance in a lump sum when they’re due, so this is hardly a disadvantage when you think about it.

What counts towards DTI ratio?

A debt-to-income (DTI) ratio includes monthly recurring debt payments like mortgage, rent, car loans, student loans, credit card payments, and other loan obligations. It also includes legally obligated payments such as alimony or child support.