If youâre worried that pulling your credit will lower your credit scores, donât be. Checking your credit is a soft inquiry, which means it wonât cause your scores to drop. And actually, checking your credit reports and credit scores regularly can be a good idea.

If you monitor your credit, you could catch errors on your credit reports that might otherwise lower your credit scores. It could also help you spot potential fraud or identity theft.

Hey there friend! If you’re frettin’ over whether using CreditWise is gonna tank your credit score let me put your mind at ease right outta the gate it don’t hurt your score one bit. Nope, not even a tiny scratch. I’ve been down that road, stressin’ over every little thing that might mess with my credit, and I’m here to tell ya that CreditWise is a safe bet. It’s like checkin’ the oil in your car—ya just wanna know what’s up without breakin’ anything, right? So, stick with me, and let’s unpack this whole deal about CreditWise, credit scores, and why you shouldn’t be losin’ sleep over it.

What’s This CreditWise Thing Anyway?

Alright, lemme break it down real simple. CreditWise is a free tool offered by Capital One, and get this—you don’t even gotta be their customer to use it. It’s like a friendly neighborhood watch for your credit, keepin’ an eye on things so you don’t have to. They let you peek at your credit score and report whenever you want, no strings attached. And the best part? It’s all done with what they call a “soft inquiry,” which is just a fancy way of sayin’ it won’t mess with your score. Me and my pal were skeptical at first, thinkin’ “free” always comes with a catch, but nah, this one’s legit.

Here’s what CreditWise does for ya in a nutshell

- Shows your credit score: You can check it daily if you’re obsessed like I was.

- Keeps tabs on reports: It watches two of the big credit bureaus for changes or weird stuff.

- Alerts ya quick: If somethin’ funky pops up, like a new account or odd activity, you’ll get a heads-up.

- Plays “what if” games: They got a simulator to show how certain moves, like payin’ off debt, might change your score.

So, it’s like havin’ a little credit guardian angel sittin’ on your shoulder. But the big question still looms—does messin’ with it hurt your score? Let’s dive deeper.

Why CreditWise Ain’t the Credit Score Boogeyman

I get it. You’ve heard horror stories about how checkin’ your credit or applyin’ for stuff can ding your score. I used to think every little peek was gonna cost me points, like losin’ lives in a video game. But here’s the real deal: not all credit checks are created equal. There’s two kinds—soft and hard—and they’re as different as night and day.

- Soft inquiries: This is what CreditWise uses. It’s like sneakin’ a glance at your credit report without anyone carin’. It don’t affect your score at all. Zero. Zilch. Whether it’s you checkin’ through CreditWise or some insurance company quotin’ a policy, soft pulls are harmless. They might show up on your report for a couple years, but they’re invisible to your score.

- Hard inquiries: Now, these are the bad boys. When you apply for a credit card, a car loan, or a mortgage, lenders do a hard pull. That can knock off a few points—sometimes up to 10—but it’s usually temporary. These stick around affectin’ your score for about a year and stay on your report for two.

CreditWise sticks to the soft stuff, so you can check your score till the cows come home, and it won’t make a dent. I remember panickin’ before a big loan application, thinkin’ I’d already messed up by snoopin’ around with tools like this. Turns out, I was worryin’ for nothin’. It’s safe as houses, fam.

How CreditWise Works Its Magic Without the Hurt

Now, let’s chat about how CreditWise pulls this off When you sign up (and yeah, it’s free for realz), they link up with your credit profile usin’ a soft inquiry They keep an eye on two major credit bureaus—think of ‘em as the big dogs who track your credit history. CreditWise watches for any changes, like if someone tries to open an account in your name or if your score shifts. If somethin’s up, they ping ya with an alert, either through email or their app. It’s like havin’ a buddy who texts ya when they spot trouble.

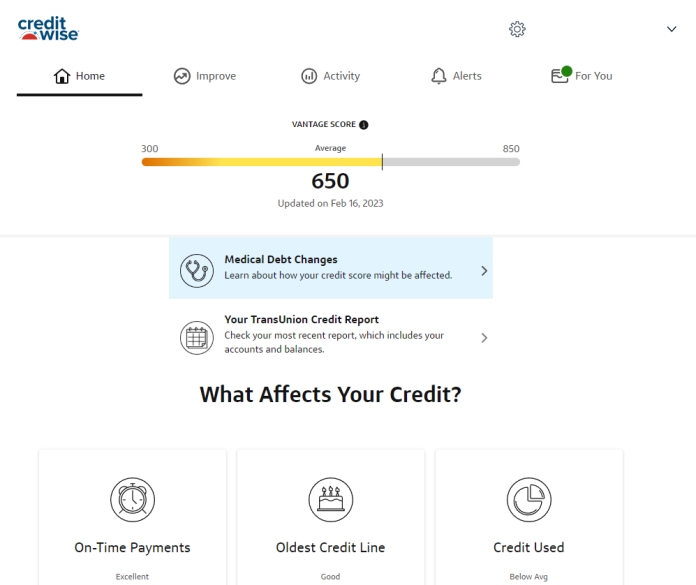

They also show ya your score usin’ a model called VantageScore 3.0. Now, I ain’t gonna bore ya with techy details, but just know it’s a legit way to measure your credit health. It might not be the exact same number a lender sees (they often use somethin’ called FICO), but it’s close enough to give ya a solid idea of where ya stand. I’ve used it to gauge if I’m ready to apply for stuff without gettin’ blindsided by a bad number.

One cool trick they got is a simulator. You can play around with “what if” scenarios—like, what happens if I pay off half my credit card balance? Or if I open a new card? It ain’t 100% accurate, but it’s a darn good way to see if a money move is gonna help or hurt. I tried it once before clearin’ a big chunk of debt, and it gave me the guts to go for it. No harm, no foul.

Why Checkin’ Your Score with CreditWise is Actually Smart

Here’s the kicker—usin’ CreditWise or any tool to check your score ain’t just safe; it’s a freakin’ good idea. Why? ‘Cause keepin’ tabs on your credit can save your bacon. I learned this the hard way when I ignored mine for years, only to find a weird error draggin’ me down. If I’d been checkin’ regularly, I coulda caught it sooner.

Here’s why monitorin’ matters:

- Spot mistakes early: Credit reports can have errors—like an account that ain’t yours or a late payment ya swear ya made. Catchin’ these quick can stop your score from takin’ a hit.

- Catch sneaky fraud: If some scumbag tries stealin’ your identity, you’ll see weird activity pop up, like new accounts ya didn’t open. CreditWise alerts help ya slam the brakes on that nonsense.

- Know where ya stand: Before applyin’ for a loan or card, checkin’ your score lets ya know if you’re in fightin’ shape or need to buff up first.

I used to think ignorin’ my credit was the safe play—outta sight, outta mind, right? Wrong. That’s like ignorin’ a leaky pipe till your house floods. Tools like CreditWise let ya stay ahead of the game without riskin’ a thing.

What Does Hurt Your Credit Score Then?

Since we’ve cleared up that CreditWise ain’t the villain, let’s talk about what actually can mess with your score. It’s worth knowin’ so you don’t trip over these landmines. Your credit score is kinda like a report card for your money habits, and a buncha things go into calculatin’ it. Here’s the breakdown in a handy lil’ table, based on how the big scoring folks figure it out:

| Factor | Impact on Score | What It Means |

|---|---|---|

| Payment History | 35% | Do ya pay bills on time? Missin’ payments is the fastest way to tank your score. |

| Credit Utilization Ratio | 30% | How much debt ya got compared to your limits? Keep it under 30% if ya can. |

| Credit History Length | 15% | How long ya been usin’ credit? Older accounts help, so don’t close ‘em willy-nilly. |

| New Credit | 10% | Applyin’ for lotsa new stuff quick looks risky. Hard inquiries fall here. |

| Credit Mix | 10% | Got a variety of credit—like cards and loans? Diversity looks good if managed well. |

Hard inquiries, like we talked about, are part of that “new credit” chunk. If you’re applyin’ for a buncha credit cards or loans in a short span, each one can ding ya a little. I made that mistake once, applyin’ for three cards in a month like a dope, and my score took a nosedive. But checkin’ your own score through CreditWise? That’s not even on the radar for this stuff.

Other baddies include missin’ payments (huge no-no), maxin’ out cards, or havin’ nasty marks like bankruptcies or collections. Those can haunt ya for years. I had a late payment stick on my report for way too long ‘cause I forgot about a tiny bill. Don’t be me—stay on top of it.

How to Boost Your Score Without Breakin’ a Sweat

Alright, now that we know CreditWise won’t hurt ya and what does, let’s flip the script. How do ya make that score shine? I’ve been workin’ on mine for a while now, and lemme tell ya, it’s not rocket science—just takes some steady grind. Here’s my go-to tips for pumpin’ up your credit game:

- Pay on time, every time: Set reminders or auto-payments if ya gotta. Late payments are the devil for your score. I started usin’ calendar alerts, and it’s been a lifesaver.

- Keep debt low: Don’t max out your cards. Aim to use less than 30% of your limit. I used to hover near the max, thinkin’ it was fine, but droppin’ it down made a big diff.

- Don’t apply for too much at once: Space out applications for new credit. One hard pull ain’t bad, but a bunch looks like ya desperate. Learned that one the hard way.

- Check for goofs: Use tools like CreditWise to peek at your report. If somethin’ looks off, dispute it with the credit bureaus. I found an old error once and got it wiped clean.

- Mix it up (carefully): If ya only got credit cards, maybe consider a small loan or somethin’—but only if ya can handle it. Variety helps, but don’t overdo it.

- Hang onto old accounts: Don’t close your oldest card, even if ya don’t use it much. The age of your credit history matters. I almost shut down my first card, but glad I didn’t.

Buildin’ credit is like growin’ a garden—takes time, care, and not yankin’ stuff out by the roots. I’ve seen my score creep up slow but sure by stickin’ to these basics. And usin’ CreditWise helped me track if my efforts were payin’ off without any downside.

Is CreditWise the Only Game in Town?

Now, you might be wonderin’, “Is CreditWise the only way to check my score safe-like?” Nah, it ain’t. There’s other free tools out there that also use soft inquiries, meanin’ they won’t hurt ya either. But I dig CreditWise ‘cause it’s got a slick app, updates quick, and throws in extras like alerts for sketchy stuff online. I ain’t sayin’ it’s perfect—it don’t watch all three credit bureaus, just two—but for a freebie, it’s hard to beat.

If you’re super paranoid about gettin’ the full picture, ya can grab free reports from all three bureaus at a certain government-approved site. Takes more effort than tappin’ an app, but it’s there if ya want it. I’ve done both—just depends on how deep ya wanna dig. Point is, checkin’ your own credit, no matter the tool, shouldn’t cost ya points if it’s a soft pull.

Any Catches with CreditWise I Should Worry About?

I know, I know—free stuff always feels like there’s a hidden “gotcha.” With CreditWise, I ain’t found one yet, but let’s be real for a sec. They’re a big company, and they might use your info for marketin’ or share it with partners unless ya tell ‘em not to. That’s pretty standard, though. Didn’t bug me much ‘cause I’m already gettin’ spam from everywhere else. Just read the fine print if ya worried about privacy.

Also, remember the score they show might not be the exact one a lender pulls. It’s close, but not always spot-on. I used it as a rough guide when shoppin’ for a car loan, and it was good enough to prep me. Ain’t no tool gonna predict every lender’s system, so don’t sweat it too hard.

Why I Keep Comin’ Back to CreditWise

Here’s my two cents: CreditWise is my go-to ‘cause it takes the guesswork outta credit checkin’. I used to avoid lookin’ at my score, scared I’d somehow mess it up just by glancin’ at it. Sounds dumb now, but that fear was real. This tool showed me I can stay in the know without riskin’ a thing. Plus, their alerts caught a weird change once that turned out to be nothin’, but havin’ that heads-up felt like a weight off my chest.

I’ve recommended it to fam and friends who’re just startin’ to figure out this credit nonsense. It’s a solid first step if ya new to the game or rebuildin’ after some rough patches. And since it don’t hurt your score, there’s no reason not to give it a whirl.

Final Thoughts: Stop Stressin’ and Start Checkin’

So, does CreditWise hurt your score? Hell nah, it don’t. It’s a safe, free way to keep an eye on your credit without playin’ with fire. I’ve been usin’ it for a while now, and it’s only helped me stay on top of things—spot errors, dodge fraud, and just feel less clueless about where I stand. Credit scores can feel like this big, scary mystery, but tools like this peel back the curtain without slappin’ ya with penalties.

If you’re sittin’ there, wonderin’ if ya should check your score but scared of the fallout, lemme tell ya—don’t wait. Get on it. Use CreditWise or whatever floats your boat, but know that peekin’ at your own credit ain’t gonna bite ya. What will bite is ignorin’ it till somethin’ goes wrong. I’ve been there, and it sucks. Take control, keep learnin’ about what bumps your score up or down, and you’ll be golden.

Got questions or still feelin’ iffy? Drop a comment or shoot me a message. I’m all ears, and I wanna help ya navigate this credit jungle. Let’s keep that score climbin’ together, alright?“`

Do I have to pay to check my credit score?

You can use paid services to check your credit score, but you donât have to. Apps like CreditWise are free for everyone. And it gives you access to your credit score with a tap, so you can check whenever you like.

How soft and hard credit inquiries impact your score

When it comes to credit reviews, there are two ways to request information:

- Hard inquiries

- Soft inquiries

Sometimes referred to as hard and soft pulls, the type of inquiry determines whether it will affect your credit scores.

Soft inquiries can appear on your credit report for up to two years, but they donât affect your credit scores because they arenât tied to lending.

Soft credit pulls are typically done by:

- Employers: to verify your credit

- Insurance companies: to give you policy quotes

- Credit monitoring companies: to check your activity

- Other companies: to promote a loan, insurance, credit card or credit limit increase

When a lender looks at your credit history to decide whether to lend you money or approve you for a credit card, thatâs considered a hard inquiry or hard pull.

Hard pulls might temporarily lower your credit scores by as much as 10 points. But that drop will likely be temporary. They typically affect your credit scores for a year, but they can stay on your credit reports for up to two years.

Hard inquiries generally happen when you apply for:

- Credit cards

- Car loans

- Mortgages

- Personal loans or lines of credit

Because applying for a lot of credit in a short amount of time can negatively affect your credit, you might want to consider waiting between credit applications.

One exception is when youâre looking for the best interest rate on a mortgage or auto loan and multiple lenders check your credit around the same time. Credit bureaus will usually consider these mortgage or auto loan inquiries as one inquiry if theyâre done in a short amount of timeâtypically 14 to 45 days. But multiple credit card applications will count as individual hard inquiries, even if theyâre done on the same day.

Keep in mind, credit inquiries can also be done when you apply for things like a new apartment or utilities. So itâs a good idea to ask the person doing the credit pulls whether or not they could affect your credit.

Will CreditWise Affect My Credit Score? – CreditGuide360.com

FAQ

Does CreditWise hurt your score?

Will using CreditWise hurt my credit score? It won’t. You can use all of CreditWise’s features without hurting your credit score.

How rare is a 700 credit score?

Does CreditWise show your actual credit score?

Know your credit score

CreditWise shows your recent FICO Score 8 from TransUnion. You’ll be able to keep tabs on your credit score and track how it changes over time.

How rare is an 800 credit score?

An 800 credit score is relatively rare, with approximately 23% of Americans achieving this “exceptional” FICO score range (800-850), according to The Motley Fool.