Your credit utilization ratio is important even if you pay your bills in full. You could have a high credit utilization if your card issuer has already reported your cardâs balance to the credit bureaus prior to your payment.

You wont accrue interest on your purchases if you pay your credit card bill in full each month, and the on-time payments can help improve your credit score. However, paying in full doesnt guarantee youll have a low credit utilization ratio, and a high utilization ratio could hurt your credit scores. If you want to be sure youll have a low utilization ratio, you may need to pay down your balance before the end of each billing cycleâgenerally, about three weeks before the bill is due.

Hey there folks! If you’re like me you’ve probably thought, “If I pay off my credit card every month, I’m golden, right?” Well, lemme hit ya with a hard truth credit utilization still counts, even if you pay it off in full. Yeah, it’s a sneaky lil’ gotcha in the credit game that can mess with your score without you even realizing. So, does credit utilization count if you pay it off? Abso-freaking-lutely, and I’m gonna break it down for ya in simple terms, no fancy jargon, just straight talk.

At our lil’ corner here at [Your Company Name], we’ve seen how this trips up so many peeps. You swipe that card, pay the bill on time, and still get dinged on your credit score. Sucks, don’t it? In this post, I’m diving deep into what credit utilization is, why it matters even when you clear your balance, and how to outsmart this pesky rule. Plus, I’ll toss in some extra tips to boost your credit game. Let’s get started!

What the Heck Is Credit Utilization Anyway?

Alright, let’s keep this basic. Credit utilization is just a fancy way of saying how much of your available credit you’re using It’s figured out by dividing your credit card balance by your credit limit, then turning that into a percentage Say you got a card with a $5,000 limit and you’ve racked up $2,500 on it. That’s 50% utilization. Easy peasy, right?

Now, why does this matter? ‘Cause this number is a big deal for your credit score. It’s like 30% of your FICO score—that’s huge! Them scoring folks think if you’re using a ton of your credit, you might be in a financial pickle and could miss payments. So, a high utilization ratio can drag your score down, even if you ain’t struggling one bit.

Here’s the kicker: even if you pay off that $2,500 balance every single month, that 50% utilization might already be reported to the credit bureaus. And that’s where the trap lies, my friend.

Why Paying in Full Don’t Always Save Ya

You might be scratching your head, thinking, “But I pay my bill in full, so my balance should be zero!” Well, not quite. See, credit card companies don’t report your balance the second you pay it off. They usually send that info to the credit bureaus at the end of your billing cycle—ya know, when they send you your statement. Your bill ain’t due for another few weeks after that, usually 21 to 25 days.

So, here’s what happens:

- You use your card all month, maybe rack up a big balance.

- Billing cycle ends, and the card company reports that balance to the bureaus.

- Then you pay it off in full when the bill comes, avoiding interest like a boss.

But guess what? The credit bureaus already got that high balance on record. And your credit utilization is based on what’s in their report, not what’s in your bank account right now. So, even if you pay every penny, a high utilization ratio could still hurt your score. Ain’t that a punch to the gut?

Oh, and one more thing—unless you ain’t used the card at all since the last cycle ended, your current balance won’t be zero anyway. Them new charges keep piling up, don’t they?

How High Utilization Messes With Your Score

Let’s get real for a sec. High credit utilization can knock your credit score down a peg or two, and that’s a problem if you’re tryna get a loan, rent a place, or even snag a better interest rate. Like I said, it’s about 30% of your FICO score, under the “amounts owed” category. Another scoring model, VantageScore, also weighs it heavy, callin’ it “total credit usage and balance” or somethin’ like that. Point is, it’s a big player.

The logic behind it? If you’re maxing out your cards, or close to it, you look risky to lenders. They think, “This person might not be able to handle their bills.” Now, I know plenty of us use cards for rewards or convenience and pay ‘em off like clockwork. But the scoring system don’t care about your good intentions. It just sees that high percentage and dings ya.

So, How Do You Keep Utilization Low?

Alright, enough of the bad news. Let’s talk solutions. If you wanna keep your credit utilization low and your score high, even while paying in full, here’s some tricks I’ve picked up over the years at [Your Company Name]. These are straight-up practical, no fluff.

- Pay Down Your Balance Early, Like Real Early: Don’t wait for the bill to come. Pay off some or all of your balance before the billing cycle ends. That way, the balance reported to the bureaus is lower. You can even make multiple payments during the month to keep it down. I do this myself—every payday, I toss a chunk at my card just to keep things tidy.

- Ask for a Higher Credit Limit: If you got a decent payment history, call up your card issuer and ask for a bigger limit. If they bump it up, your utilization drops without changing how much you spend. Say your limit goes from $5,000 to $10,000, and you still got $2,500 on there. Boom, you’re at 25% instead of 50%. Sweet, right?

- Keep Old Cards Open, Even If You Don’t Use ‘Em: Every card adds to your total available credit. Closing an old card shrinks that number, which can spike your utilization. I got a dusty old card I ain’t touched in years, but I keep it open just for this reason. Just watch out for annual fees—if it’s costing ya, might not be worth it.

- Get a New Card, But Only If It Makes Sense: I ain’t sayin’ apply for credit just to game the system, ‘cause that’s a risky move. But if you spot a card with a dope bonus or perks you want, grabbing it can boost your total credit limit and lower utilization. Just don’t go wild opening a bunch at once—too many applications can hurt your score.

Here’s a lil’ rule of thumb we swear by: try to keep your utilization under 30%. But honestly, if you’re paying in full anyway, aim for under 10%. Heck, some utilization is better than none—zero percent can look weird to lenders, like you ain’t using credit at all. So, maybe leave a tiny balance, just a couple percent of your limit, before the cycle ends, then pay the rest off when the bill’s due to dodge interest.

Check this quick table for a glance at good vs. bad habits:

| Habit | Good Move | Bad Move |

|---|---|---|

| Payment Timing | Pay before billing cycle ends | Wait until bill is due |

| Credit Limit | Request increase if possible | Stick with low limit |

| Old Cards | Keep ‘em open for more credit | Close ‘em and lose available credit |

| Utilization Target | Under 10-30% | Above 30%, ouch! |

Other Ways to Boost Your Credit Score (While You’re At It)

Since we’re talkin’ credit, let’s not stop at utilization. There’s a bunch of other stuff you can do to make your score shine. I’ve been down this road, messin’ up and learnin’, so lemme share what works.

- Pay Them Bills on Time, No Excuses: Your payment history is even more important than utilization. It’s like the king of credit score factors. Miss a payment, and it’s a black mark for years. Set reminders, auto-payments, whatever it takes. I got burned once by forgetting a bill—never again!

- Mix Up Your Credit Types: Utilization only looks at revolving credit, like cards. But havin’ different kinds—like a car loan or personal loan—shows you can handle all sorts of debt. It’s called credit mix, and it helps. Just don’t take on debt you can’t manage, ya hear?

- Clear Out Old Collection Accounts: If you got stuff in collections from way back, try to pay it off. Some newer scoring systems ignore paid collections, which can give your score a lil’ bump. I had an old medical bill haunting me, paid it, and felt a weight lift off.

- Check Your Credit Report for Screw-Ups: Errors happen, tho they ain’t common. Grab your free credit report and look it over. If somethin’ ain’t right, dispute it. I found a weird charge once that wasn’t mine—got it fixed and my score ticked up.

Why Timing Is Everything With Payments

Lemme double down on this timing thing ‘cause it’s a game-changer. Most card companies report your balance at the end of the billing cycle, but when’s that exactly? Check your statement or call ‘em up to find out. Once you know, plan to pay a big chunk a few days before that date. That reported balance will be lower, and your utilization looks better. I started doin’ this a couple years back, and it’s made a real difference in keepin’ my score steady.

If you’re super on top of things, pay multiple times a month. Got a big purchase? Pay it off right after. Got a regular subscription hittin’ the card? Toss some cash at it weekly. It’s extra work, but it keeps that balance tiny when the reportin’ happens.

The Mental Game of Credit Utilization

Here’s somethin’ people don’t talk about enough—the headspace this stuff puts ya in. It’s frustratin’ as heck to do everything “right” and still get a lower score ‘cause of utilization. I’ve been there, feelin’ like the system’s rigged. But once you get how it works, you can play the game smarter. Think of it like a challenge: “I’m gonna beat this utilization trap!” Turn that annoyance into action by tweakkin’ your payment habits.

Also, don’t stress too much if your score dips a lil’ from high utilization one month. It’s one of them factors you can fix quick. Pay early next time, and it usually bounces back. I’ve had months where I overspent for a vacay or somethin’, saw my score drop, but got it back up in a couple cycles. Just stay consistent.

Common Myths About Credit Utilization

There’s a lotta bunk floatin’ around about this topic, so lemme clear up a few myths I’ve heard while helpin’ folks at [Your Company Name].

- Myth: Paying in full means zero utilization. Nope, like I been sayin’, it’s about what’s reported, not what you pay later.

- Myth: Utilization don’t matter if you got a high score already. Wrong! It’s always a factor, no matter how good your score is. A high ratio can still pull it down.

- Myth: You should never use your card to keep utilization low. Nah, some usage is good. Shows you’re active with credit. Just keep it low, under that 10-30% sweet spot.

How Much Utilization Is Too Much?

I touched on this, but let’s hammer it home. Under 30% is the general guideline for “safe” utilization. But if you’re tryna max out your score, shoot for under 10%. Why? ‘Cause the lower, the better—lenders see you as super low-risk. I aim for around 5-8% myself. Use just enough to show activity, but not so much it looks like I’m leanin’ hard on credit.

If you’re over 30%, it’s not the end of the world, but it’s a red flag. Over 50%? Yikes, that’s gonna hurt. And if you’re pushin’ 80-100%, lenders might think you’re in deep trouble, even if you pay off every month. So, keep an eye on them percentages.

Tools to Track Your Utilization

Wanna know where you stand? There’s ways to check your utilization without guessin’. Sign up for a free credit account somewhere (no names, just sayin’ it’s out there). They often show your overall utilization ratio and break it down by card. I check mine monthly to make sure I ain’t creepin’ up too high. Some even let ya see the key stuff draggin’ your score down, so you know if utilization’s the culprit.

Or, do the math yourself. Add up all your card balances, add up all your limits, divide, and multiply by 100 for the percentage. It’s a pain, but it works if you’re old-school like that.

A Personal Story to Drive It Home

Lemme tell ya ‘bout a time I got bit by this utilization nonsense. A few years back, I was usin’ my card for everything—groceries, gas, you name it—‘cause I wanted them reward points. Paid it off religiously every month, felt like a financial genius. Then I checked my credit score to apply for a car loan, and it was lower than I expected. I was like, “What the heck?!” Turns out, my utilization was sittin’ at 60% ‘cause I was rackin’ up big balances before the cycle ended. Started payin’ early, got it down to under 15%, and my score climbed back up. Lesson learned, and now I’m passin’ it on to you.

Wrappin’ It Up With a Bow

So, does credit utilization count if you pay it off? Hell yeah, it does, ‘cause it’s all about that reported balance at the end of your billing cycle, not what you pay later. It’s a sneaky rule, but now you know how to beat it. Pay early, bump up your limits, keep old cards open, and aim for under 10-30% utilization. Toss in on-time payments and a mix of credit types, and you’re buildin’ a score that’ll make lenders drool.

At [Your Company Name], we’re all about helpin’ ya navigate this financial maze. Got questions or a weird credit sitch? Drop a comment below—I’m all ears. Let’s keep this convo goin’ and get your credit where it needs to be. Catch ya later!

How to Lower Your Credit Utilization Ratio and Improve Credit

If you want to lower your credit utilization ratio to improve your credit score, but dont want to use your credit card less often, here are a few things you can do:

- Pay down the balance early. Rather than waiting until your bill is due, you can pay down your balance before the end of each billing cycle. Or, you can make several payments throughout the month to bring down the balance that gets reported.

- Ask for a credit limit increase. A higher credit limit can also lead to a lower utilization if you maintain the same spending habits. You may be able to call your card issuer or ask for a credit limit increase through your online account.

- Dont close old credit cards. Every credit card contributes to your total available credit, which is one reason keeping credit cards open can be helpful. However, it might not be worth paying an annual fee for a card you dont use.

- Open a new credit card. Generally, applying for credit solely to improve your credit score isnt a good idea. However, if you see a card that has a good intro bonus or enticing benefits, you could get a new credit card and also benefit from the increased available credit.

A general rule of thumb is to keep utilization under 30%, but lower is even better. If youre paying off your credit card in full each month anyway, try to keep your overall utilization under 10% instead.

Additionally, some utilization is actually better than 0% utilization. Instead of paying off your entire balance early, you may want to pay down your balance until youre using only a couple of percentage points of your cards credit limit. Then, pay off the remaining balance before your bills due date to avoid interest charges.

Other Ways to Improve Your Credit Score

Credit utilization can be an important scoring factor, and its one of the few scoring factors that you may be able to quickly change to improve your credit score. But there are lots of other things you can do to build and maintain a good credit score.

- Pay your bills on time. Your payment history is even more important than your credit usage, and having a history of on-time payments is important for improving your credit.

- Use Experian Boost®ø. Experian Boost is a free feature you can use to add on-time payments for several types of accounts to your Experian credit report, including eligible rent, utility and streaming service bills. These usually arent part of your credit report, so the new accounts might instantly boost your credit score.

- Use different types of credit accounts. Your credit utilization ratio only considers revolving credit accounts. But having open installment loans, such as an auto, student, home or personal loan, can add to your credit mix and help your scores.

- Pay off collection accounts. If youve had accounts sent to collections, try to pay them off. Newer scoring models may ignore paid-off collections, which could increase your scores.

- Review your credit reports for errors. Although its not common, credit reports sometimes have errors that could be hurting your credit score. Closely review your credit report; you have the right to dispute erroneous information if you find any.

Credit utilization doesn’t matter

FAQ

Does credit utilization matter if I pay it off?

Yes, your credit utilization still matters even if you pay your bills in full. Since there is no standard date or time credit card companies report to agencies, it’s hard to prepare your balance in advance. It’s often best to try and keep your credit usage below 30% with some experts suggesting even lower.

Does credit utilization reset after payment?

If you make a large purchase but pay it off fairly quickly, your utilization will go down once that payment hits your credit report.Apr 9, 2025

How do I raise my credit score 100 points in 30 days?

For most people, increasing a credit score by 100 points in a month isn’t going to happen. But if you pay your bills on time, eliminate your consumer debt, don’t run large balances on your cards and maintain a mix of both consumer and secured borrowing, an increase in your credit could happen within months.

Does 0% utilization hurt credit score?

Yep, having 0% utilization can sometimes cause a small score drop because credit scoring models like to see some activity. It’s weird, but they prefer you to use credit rather than have a $0 balance reported.

Will my credit utilization be zero if I pay my bill?

Your credit utilization won’t necessarily be zero, even if you pay your credit card bill in full every month. To understand why, consider how scoring models calculate utilization —which is essentially your account’s balance divided by its credit limit and displayed as a percentage.

Does credit utilization affect your credit score?

If you don’t want your credit utilization to negatively affect your credit scores, consider your spending habits. Factors such as your credit history and the number of cards in your wallet matter, too. High utilization on a single credit card could especially hurt your credit scores if you have a short credit history and only one card.

Why is your credit utilization ratio important?

Your credit utilization ratio is important even if you pay your bills in full. You could have a high credit utilization if your card issuer has already reported your card’s balance to the credit bureaus prior to your payment.

How do I calculate credit utilization?

Calculating credit utilization requires adding up the outstanding balances on your revolving credit accounts and dividing the total by the overall credit limit across all those accounts. Note that you should not divide the cumulative balance by the remaining available credit, but rather by the total credit limit.

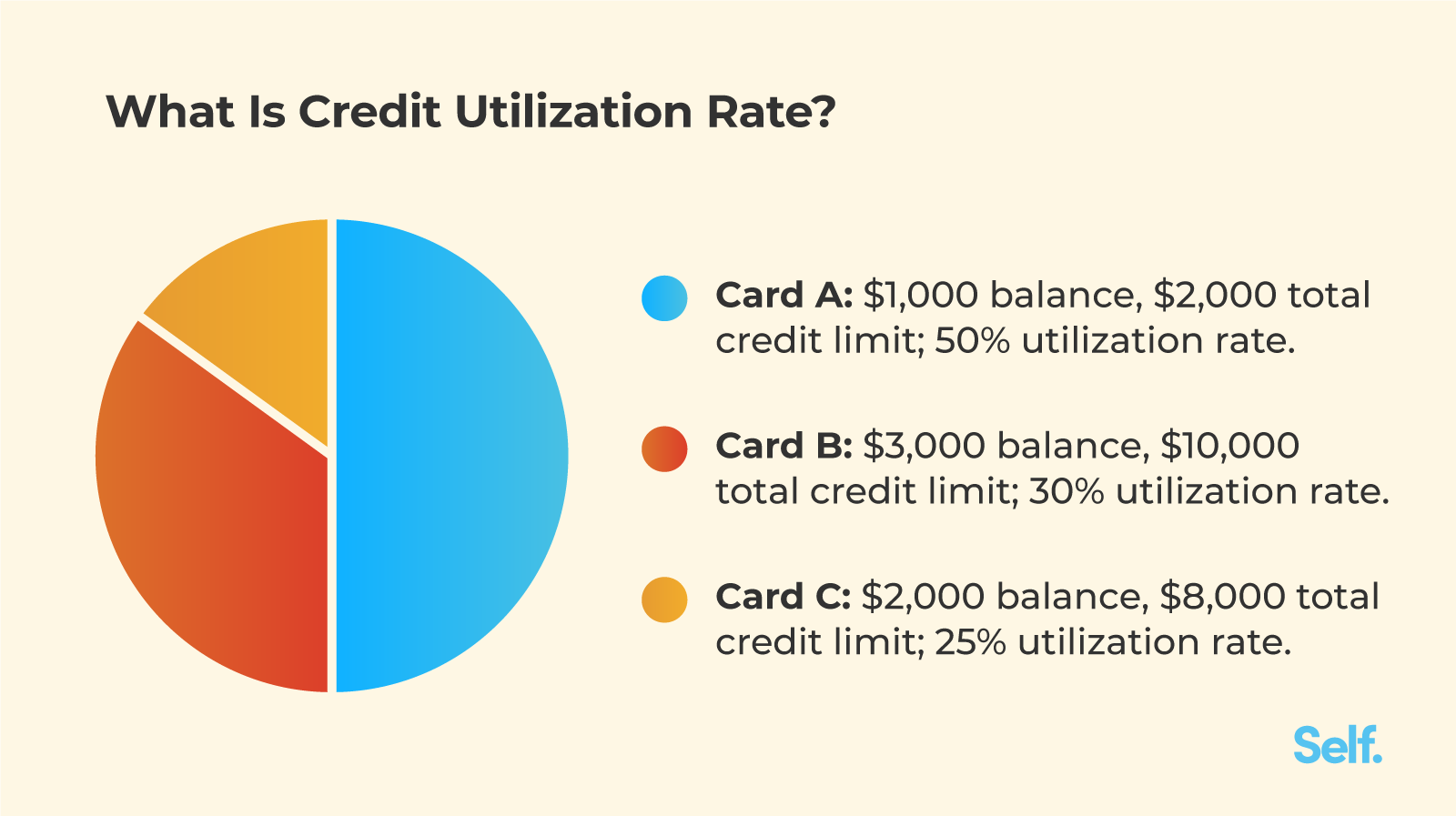

What is credit utilization?

Credit utilization is a credit scoring factor that makes up 30 percent of your FICO credit score and is also considered “highly influential” to your VantageScore. It looks at how much you owe across all open revolving lines of credit (such as credit card accounts and home-equity lines of credit) and compares that to your total credit limit.

What percentage should credit utilization be?

Experts suggest keeping credit utilization at less than 30 percent to maintain good credit, but those with excellent credit keep it below 10 percent. Lower your credit utilization by paying off revolving debt, requesting a higher credit limit, performing a balance transfer or applying for a new credit card.