Quick Summary

Wondering if your trust can shield assets from the IRS? The short answer is yes, but with significant limitations. While irrevocable trusts offer some protection, their effectiveness depends entirely on structure, administration, and compliance with tax laws. This article breaks down when trusts work as shields against the IRS, when they fail, and how to create the strongest possible protection for your assets.

The Reality of Trust Protection Against the IRS

Let me be straight with you – I’ve seen many clients come to us believing their trust makes their assets completely “untouchable” by the IRS. Unfortunately that’s not quite how it works.

The truth is that while trusts can create important legal barriers, the IRS has special powers that other creditors don’t. They’re basically the financial equivalent of a determined honey badger – they have ways to get what they want if they believe you owe taxes.

But don’t worry! This doesn’t mean trusts are useless for tax protection. It just means we need to understand exactly how they work and their limitations.

Irrevocable vs. Revocable Trusts: A Critical Distinction

When it comes to IRS protection not all trusts are created equal

Revocable Trusts

- Offer zero protection from the IRS

- You retain control of assets

- Assets are still considered part of your personal estate

- The IRS treats these assets as if you still own them directly

Irrevocable Trusts

- Offer potential protection from the IRS

- You permanently transfer ownership away from yourself

- Assets are legally separated from your personal estate

- The IRS has limited ability to reach these assets (with exceptions)

The key difference? With an irrevocable trust, you’ve given up ownership and control. That separation creates the legal foundation for asset protection against the IRS.

When Can the IRS Break Through Trust Protection?

Even with an irrevocable trust, the IRS has several ways to reach assets. Here are the situations where your trust protection might fail

1. Grantor Retains Too Much Control

If you (as the grantor) keep certain powers or benefits, such as:

- The ability to revoke the trust

- The power to control or direct distributions

- The right to receive trust income

The IRS may classify it as a “grantor trust” for tax purposes, making those assets fair game for tax collection.

2. The Trust Is Considered a Facade (Nominee or Alter Ego)

The IRS has special legal doctrines they use when they believe a taxpayer is playing games:

Nominee Doctrine: This applies when assets are technically in the trust’s name, but you’re still:

- Using the property personally

- Paying expenses related to it

- Maintaining a close relationship with the trust

Alter Ego Doctrine: Used when you and the trust are basically indistinguishable because:

- You’ve mixed personal and trust finances

- There’s no truly independent trustee

- You continue controlling trust assets in practice

If the IRS successfully applies either doctrine, they can treat the trust as a sham and seize assets.

3. Fraudulent Transfers

If you transfer assets to a trust:

- With existing tax debt

- To avoid paying taxes you know you’ll owe

- Without receiving fair market value

The IRS can pursue these as fraudulent transfers and potentially void them.

4. Spendthrift Provisions Don’t Block the IRS

This one surprises many clients. Those fancy “spendthrift” clauses that block normal creditors? They don’t stop the IRS. Federal tax liens trump state-level protections, meaning if a beneficiary has rights to receive distributions, the IRS can intercept them.

Creating Effective IRS Protection With Trusts

Now that we understand the limitations, here’s what actually works to maximize protection:

1. Choose the Right Trust Structure

Different situations require different trust structures. Some options to consider:

- Offshore Trusts in jurisdictions like the Cook Islands, Nevis, or Belize provide the strongest protection

- Domestic Asset Protection Trusts (DAPTs) in states like Wyoming, Nevada or South Dakota

- Irrevocable Life Insurance Trusts (ILITs) for specific insurance-based planning

2. Timing Is Everything

The most important factor? Setting up your trust before tax problems arise. The IRS can challenge transfers made:

- After a tax assessment

- When you knew tax issues were likely

- When you were already under investigation

Creating your trust as part of long-term planning rather than reactive protection makes it much stronger.

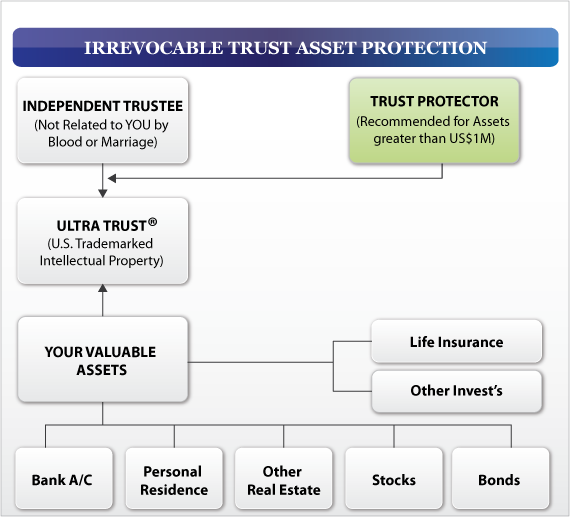

3. Use a Truly Independent Trustee

I can’t stress this enough – having your brother-in-law or best friend as trustee won’t cut it. You need:

- A professional, independent trustee

- Someone with no personal relationship to you

- A trustee who makes independent decisions

This separation helps prevent “alter ego” challenges from the IRS.

4. Maintain Proper Trust Administration

Many trusts fail because people create them but don’t operate them correctly. You must:

- Keep trust assets completely separate from personal assets

- Maintain proper accounting records

- Follow all trust formalities

- File appropriate tax returns for the trust

Sloppy administration is the fastest way to lose protection.

5. Understand the Tax Consequences

There’s often a tradeoff between asset protection and tax benefits. For example, under IRS Revenue Ruling 2023-2, assets in certain irrevocable trusts excluded from your taxable estate don’t receive a step-up in basis – potentially creating capital gains tax issues for your heirs.

Real-World Example: The Step-Up in Basis Trade-Off

Let me show you how this works with a practical example:

Imagine you put $1 million in stock into an irrevocable trust. You originally bought that stock for $200,000. If your trust keeps the stock outside your taxable estate, and your beneficiary sells it after your death, they’ll owe capital gains tax on the $800,000 gain.

But if your trust had been structured differently to include the stock in your estate, the basis would reset to $1 million at death, eliminating that tax liability.

This highlights a crucial planning decision:

- Excluding assets from your estate provides better creditor protection

- Including assets in your estate preserves tax benefits for your heirs

Common Trust Protection Mistakes to Avoid

In my years helping clients, I’ve seen these frequent mistakes destroy trust protection:

- Setting up a trust reactively – after tax problems begin

- Continuing to treat trust assets as personal property

- Naming yourself as trustee or using a close family member

- Failing to file proper tax returns for the trust

- Using cookie-cutter trust documents instead of customized planning

Who Benefits Most from IRS-Protected Trusts?

Trust protection strategies work best for:

- High net-worth individuals (typically $2+ million)

- Business owners with significant personal liability

- Those in high-risk professions (doctors, lawyers, etc.)

- People with complex estate planning needs

- Anyone concerned about future tax policy changes

The Bottom Line on Trust Protection from the IRS

So, does a trust protect assets from the IRS? It can – with proper planning, structure, and administration. But it’s not automatic, and not all trusts provide equal protection.

The strongest protection comes from:

- Well-designed irrevocable trusts

- Created well before tax issues arise

- With independent trustees

- Maintained with strict separation

- Structured with both protection and tax efficiency in mind

Remember, asset protection isn’t about hiding assets or evading taxes – it’s about legally organizing your affairs to minimize risk while fulfilling all your tax obligations.

Next Steps for Protecting Your Assets

If you’re serious about protecting assets from potential IRS claims, I recommend:

- Consulting with an experienced asset protection attorney

- Creating a comprehensive protection plan, not just a single trust

- Evaluating both domestic and offshore options

- Balancing protection with legitimate tax planning

- Implementing your plan before problems arise

With the right approach, you can create significant legal barriers between your hard-earned assets and potential IRS collection efforts, while still staying on the right side of the law.

Trust protection isn’t about hiding from legitimate obligations – it’s about creating legal separation that respects your right to preserve wealth while following the rules.

Q: Do trusts have a requirement to file federal income tax returns?

A: Trusts must file a Form 1041, U.S. Income Tax Return for Estates and Trusts, for each taxable year where the trust has $600 in income or the trust has a non-resident alien as a beneficiary. However, if the trust is classified as a grantor trust, it is not required to file a Form 1041, provided that the individual grantor reports all items of income and allowable expenses on his own Form 1040 or 1040-SR, U.S. Individual Income Tax Return. Thus, the grantor/individual would pay the total tax liability upon the filing of his return for that taxable year.

Q: What is a trust?

A: A trust is an entity created and governed under the state law in which it was formed. A trust involves the creation of a fiduciary relationship between a grantor, a trustee, and a beneficiary for a stated purpose. A trust may be created by any of the following methods:

- A declaration by the owner of property that the owner holds the property as trustee;

- A transfer of property by the owner during the owners lifetime to another person as trustee;

- A transfer of property by the owner, by will or by other instrument taking effect upon the death of the owner, in trust, to another person as trustee or

- An exercise of a power of appointment to another person as trustee or an enforceable promise to create a trust.

Does a Trust Protect From the IRS?

FAQ

Can the IRS go after assets in a trust?

Generally, the IRS cannot seize assets held in a properly structured irrevocable trust. A properly structured trust is one where the grantor fully relinquishes ownership, control, and beneficial interest, and the trust is administered independently in compliance with applicable laws.Jun 7, 2025

What are the disadvantages of putting your assets in a trust?

What assets cannot be seized by the IRS?

The IRS can’t seize certain personal items, such as necessary schoolbooks, clothing, undelivered mail and certain amounts of furniture and household items. The IRS also can’t seize your primary home without court approval. It also must show there is no reasonable, alternative way to collect the tax debt from you.

What trust can the IRS not touch?

The IRS and Irrevocable Trusts

When you put your assets into an irrevocable trust, they no longer belong to you, the taxpayer (this is different from a revocable trust, where they do still belong to you). This means that generally, the IRS cannot touch your assets in an irrevocable trust.