Bankrate is always editorially independent. While we adhere to strict , this post may contain references to products from our partners. Heres an explanation for . Our is to ensure everything we publish is objective, accurate and trustworthy. Bankrate logo

Founded in 1976, Bankrate has a long track record of helping people make smart financial choices. We’ve maintained this reputation for over four decades by demystifying the financial decision-making process and giving people confidence in which actions to take next.

Bankrate follows a strict editorial policy, so you can trust that we’re putting your interests first. All of our content is authored by highly qualified professionals and edited by subject matter experts, who ensure everything we publish is objective, accurate and trustworthy.

Our reporters and editors focus on the points consumers care about most — how to save for retirement, understanding the types of accounts, how to choose investments and more — so you can feel confident when planning for your future. Bankrate logo

Bankrate follows a strict editorial policy, so you can trust that we’re putting your interests first. Our award-winning editors and reporters create honest and accurate content to help you make the right financial decisions.

We value your trust. Our mission is to provide readers with accurate and unbiased information, and we have editorial standards in place to ensure that happens. Our editors and reporters thoroughly fact-check editorial content to ensure the information you’re reading is accurate. We maintain a firewall between our advertisers and our editorial team. Our editorial team does not receive direct compensation from our advertisers.

Bankrate’s editorial team writes on behalf of YOU – the reader. Our goal is to give you the best advice to help you make smart personal finance decisions. We follow strict guidelines to ensure that our editorial content is not influenced by advertisers. Our editorial team receives no direct compensation from advertisers, and our content is thoroughly fact-checked to ensure accuracy. So, whether you’re reading an article or a review, you can trust that you’re getting credible and dependable information. Bankrate logo

Look, I’ve been there – staring at my Roth IRA statement wondering if I could be doing more with my money. The question that kept popping into my head was simple “Can I buy and sell investments in my Roth IRA whenever I want?” If you’ve wondered the same thing you’re definitely not alone.

The short answer is yes, you absolutely can actively trade in your Roth IRA But should you? That’s where things get interesting. As someone who’s spent way too many hours researching this topic, I’m gonna break down everything you need to know about active trading in your Roth IRA account

What You’ll Learn in This Article

- Whether active trading in a Roth IRA is actually allowed

- The tax benefits (they’re pretty amazing)

- Important limitations you should know about

- Why passive investing might be better for most people

- Strategies that actually work for Roth IRA investing

Yes, You Can Actively Trade in Your Roth IRA

Let’s clear up a common misconception right away – there’s no rule from the IRS saying you can’t actively trade within your Roth IRA. You won’t get in any legal trouble for buying and selling investments frequently in your account.

The Roth IRA is basically just a tax wrapper around your investments. Inside that wrapper, you’re free to trade stocks, ETFs, mutual funds, and other investments as frequently as you want (with a few exceptions I’ll explain later).

However, there’s something important to note: while most brokers won’t charge you for trading stocks and ETFs frequently, many mutual fund companies will hit you with an early redemption fee if you sell a fund you’ve owned for less than 30 days. These fees can take a bite out of your returns if you’re frequently moving in and out of mutual funds.

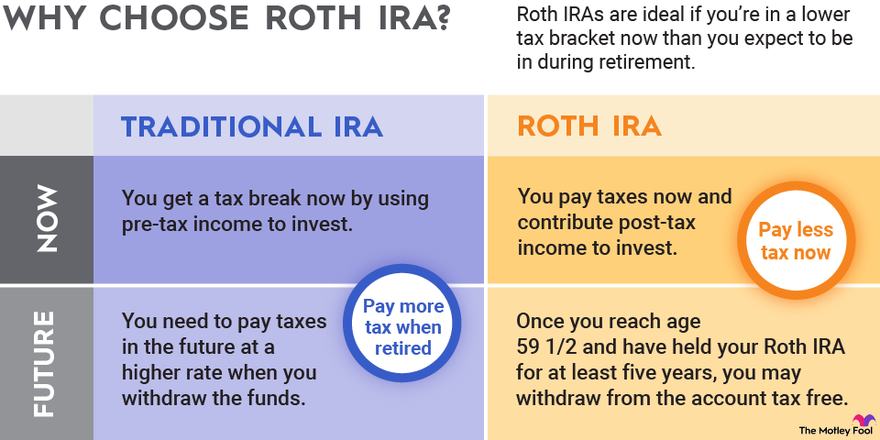

The Tax Superpowers of a Roth IRA

The biggest advantage of trading in a Roth IRA vs. a regular brokerage account is the incredible tax benefit. Any gains you make inside your Roth IRA are completely TAX-FREE… forever!

Think about that for a sec. In a regular account:

- You pay taxes on dividends every year

- You pay capital gains tax when you sell investments at a profit

But in your Roth IRA? None of that. Zero taxes on any of your investment gains, as long as you follow the basic rules.

To enjoy these benefits, you need to:

- Limit your contributions to $7,000 per year for 2025 ($8,000 if you’re 50+)

- Wait until you’re at least 59½ years old to withdraw earnings tax-free

- Have owned your Roth IRA for at least five years before taking earnings out

I should mention that you CAN withdraw your contributions (not earnings) at any time without taxes or penalties. But remember, you can’t put that money back in later beyond your annual contribution limits.

Important Limitation: No Margin Trading

Here’s where active traders might get disappointed. You cannot use margin in a Roth IRA. Margin is basically a loan from your broker that lets you invest more money than you actually have in your account.

For frequent traders, margin isn’t just about amplifying returns. It’s also super useful for being able to sell a position and immediately buy another without waiting for settlement.

In a cash account like a Roth IRA, when you sell something, you have to wait for the transaction to settle (typically one business day) before you can use that money to buy something else. With margin, you can make trades immediately without waiting.

This limitation can be frustrating if you’re trying to day trade or make quick moves in fast-changing markets.

The Uncomfortable Truth About Active Trading

OK, so you CAN trade actively in your Roth IRA, but SHOULD you? This is where I need to be straight with you.

Research consistently shows that passive investing beats active trading over time – and this applies to both individual investors like us and professional money managers.

The numbers don’t lie:

- About 57% of professional fund managers failed to beat their benchmarks in 2024

- Over a 20-year period, around 90% of pros underperformed their benchmarks

And these are professionals with teams of analysts, sophisticated tools, and years of training! If the pros struggle to beat the market through active trading, what chance do most of us have?

Instead, you can actually outperform most professionals by simply taking a passive approach with index funds. The S&P 500 has returned about 10% annually over long periods – but you need to stay invested to capture those returns.

One Big Downside: No Tax Loss Harvesting

Another disadvantage of active trading in a Roth IRA vs. a taxable account is that you can’t deduct losses.

In a regular brokerage account, if you sell an investment at a loss, you can use that loss to offset gains or even deduct up to $3,000 from your regular income. Some investors strategically use tax-loss harvesting to maximize this benefit.

But in a Roth IRA? Those losses simply disappear. Changes to the tax code in 2017 eliminated any ability to claim benefits from losses in IRA accounts.

So if your active trading leads to losses (which, statistically speaking, it probably will for most people), you won’t even get the consolation prize of a tax write-off.

The Best Roth IRA Strategy for Most People

Listen, I get the appeal of active trading. It’s exciting, and the idea of beating the market is tempting. But for most of us, the best strategy for a Roth IRA is much simpler:

- Invest in low-cost index funds

- Add money regularly (dollar-cost averaging)

- Hold for the long term

- Let compounding do its magic

Index funds passively track market indexes like the S&P 500 or Nasdaq 100. They don’t make active trading decisions – they just hold whatever the index holds.

This approach has several advantages:

- Lower costs (expense ratios of just a few dollars per $10,000 invested)

- Better performance than most active strategies over time

- Less time spent researching and monitoring investments

- Lower stress and emotional decision-making

A Simple 3-Fund Portfolio Strategy

If you want a specific strategy that’s easy to implement, consider the popular “three-fund portfolio”:

- A large-cap index fund (tracks biggest companies)

- A mid-cap index fund (medium-sized companies)

- A small-cap index fund (smaller companies)

Contribute regularly to these funds and resist the urge to trade in and out based on market news or short-term performance. This simple approach will likely outperform most active trading strategies over time.

Final Thoughts: Can vs. Should

To wrap this up – yes, you absolutely CAN buy and sell investments in your Roth IRA. There’s no rule against active trading, and the tax benefits make it an appealing place to do so.

However, for most people, active trading in a Roth IRA probably isn’t the best strategy. The limitations on margin, the inability to deduct losses, and the historical underperformance of active strategies compared to passive investing all suggest that a buy-and-hold approach with index funds is more likely to succeed.

Your Roth IRA is meant to fund your retirement – money you’ll need later in life. You can’t afford to lose it on speculative trading strategies. The boring approach might not be exciting, but it’s more likely to help you reach your long-term financial goals.

Have you tried active trading in your Roth IRA? I’d love to hear about your experiences in the comments. And if you have any questions about Roth IRA investing strategies, drop them below!

FAQs About Trading in a Roth IRA

Can I day trade in my Roth IRA?

Technically yes, but the lack of margin makes it difficult to trade frequently, and statistically, you’re unlikely to outperform the market.

How often can I buy and sell in my Roth IRA?

There are no limits on how frequently you can trade most investments, though some mutual funds may charge early redemption fees.

Will I pay taxes on trades within my Roth IRA?

No! All gains within your Roth IRA are tax-free, as long as you follow the rules for withdrawals.

What investments can I trade in my Roth IRA?

Most common investments like stocks, bonds, ETFs, and mutual funds. However, certain alternative investments may be restricted.

Can I withdraw money from my Roth IRA to cover trading losses?

You can withdraw your contributions at any time without penalty, but not earnings (before 59½). However, this reduces your tax-advantaged space, which is limited each year.

Yes, you can actively trade in a Roth IRA

Some investors may be concerned that they can’t actively trade in a Roth IRA. But there’s no rule from the IRS that says you can’t do so. So you won’t get in legal trouble if you do.

But there may be some extra fees if you trade certain kinds of investments. For example, while brokers won’t charge you for trading in and out of stocks and most ETFs on a short-term basis, many mutual fund companies will charge you an early redemption fee if you sell the fund. This fee is usually assessed only if you’ve owned the fund for fewer than 30 days.

You can’t use margin in an IRA

Many traders use margin in their accounts. With a margin loan, the broker extends your capital to invest beyond what you actually own. It’s a useful tool, especially if you’re trading frequently. Unfortunately, margin loans are not available in IRA accounts.

For frequent traders, the ability to trade on margin is not just about magnifying your returns. It’s also about having the ability to sell a position and immediately buy another. In a cash account (like a Roth IRA), you have to wait for a transaction to settle, and that typically takes a day. In the meantime, you may be unable to trade with that money even though it’s credited to your account.

A margin account allows you to buy and then trade immediately, as long as you have enough equity in the account. And that can be an advantage in fast-moving markets.