Wondering if your investment portfolio might be sending you to hell? You’re not alone! Many Christians struggle with this question, wondering if playing the stock market is just gambling in disguise or if God approves of growing wealth through investments. Let’s dive into what the Bible actually says about Christians and stock market investing.

The Big Question: Investing vs. Gambling

The main concern many believers have is whether buying stocks is essentially the same as gambling. After all, when you purchase shares, there’s no guarantee they’ll increase in value, right? This uncertainty makes some Christians uncomfortable.

But there’s actually a fundamental difference between gambling at a casino and investing in stocks

- Gambling: You risk money you’ll probably lose, hoping for a quick windfall based mostly on luck

- Investing: You purchase partial ownership in actual companies, planning for long-term growth based on sound decision-making

It really comes down to your intentions. When you invest wisely in the stock market with a long-term perspective, you’re not just rolling dice in Vegas—you’re making a prudent financial decision that can help secure your future.

What Does the Bible Say About Investing?

Surprise! The Bible doesn’t explicitly mention “stock markets” (probably because ancient Israelites weren’t trading Apple shares). However, Scripture does provide principles that apply to wealth management and investing.

Biblical Principles That Support Wise Investing

Proverbs 28 20 offers this wisdom “A faithful man will be richly blessed but one eager to get rich will not go unpunished.”

This verse warns against the “get-rich-quick” mentality. God isn’t against wealth, but He definitely has concerns about how we pursue it. Long-term investment planning? That’s good stewardship. Trying to make an overnight fortune through risky day-trading? That’s moving into questionable territory.

2 Corinthians 9:6 reminds us that “whoever sows sparingly will reap sparingly, and whoever sows generously will reap generously.”

While this passage is actually about our spiritual relationship with God, it demonstrates an important principle that applies to investing sometimes you must sacrifice now to gain later. This is precisely what long-term investing is all about!

Proverbs 3:9-10 states, “Honor the Lord with your wealth, with the first fruits of all your crops; then your barns will be filled to overflowing, and your vats will brim over with new wine.”

This passage suggests that when we honor God with our resources, He blesses our stewardship. This can certainly include wise investing!

When Stock Market Investing Becomes Problematic

Not all investing approaches align with Christian values. Here are some situations where stock market participation might conflict with biblical principles:

1. When It Resembles Gambling

Some investment strategies, particularly day-trading, look suspiciously like gambling. If your approach relies more on “luck” than on wisdom and patient planning, you might want to reconsider.

2. When You Trust Money More Than God

The Bible repeatedly warns against putting our trust in wealth rather than in the Lord. 1 Timothy 6:17-18 cautions the rich “not to be arrogant nor to put their hope in wealth, which is so uncertain, but to put their hope in God.”

If you find yourself obsessively checking your stock portfolio while your Bible collects dust, it might be time to reassess your priorities!

3. When It Harms Your Family Obligations

Ecclesiastes 5:13-14 warns about wealth being hoarded to the harm of its owners. If your investing comes at the expense of meeting your family’s needs, that’s a problem.

Practical Guidelines for Christian Investors

So how can a Christian invest in the stock market with a clear conscience? Here are some practical tips:

- Maintain proper perspective – Your ultimate security comes from God, not your investment portfolio

- Invest for the long-term – Avoid get-rich-quick schemes and day-trading

- Honor your commitments – Don’t neglect tithing, giving, or family needs

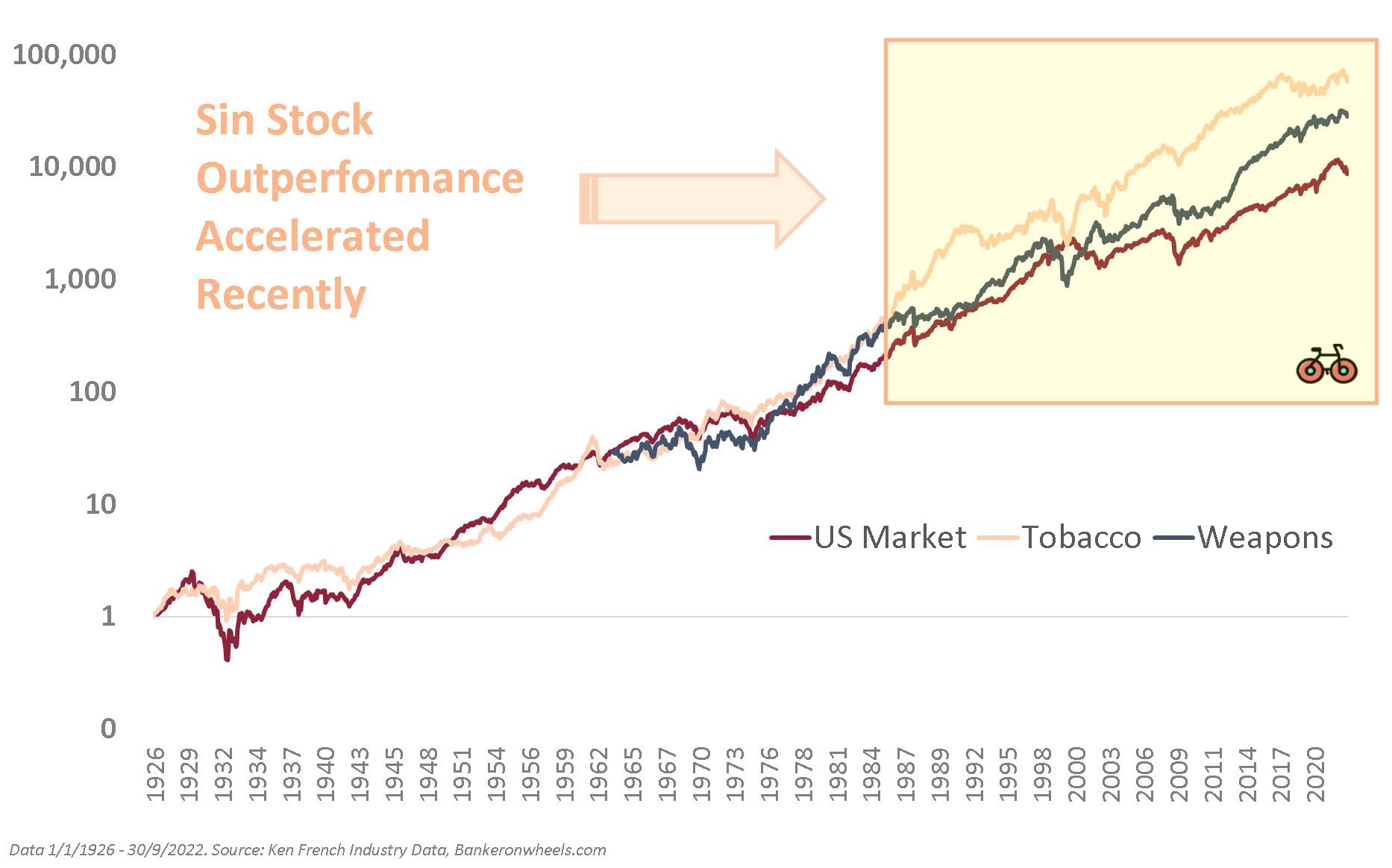

- Research ethical investments – Consider companies whose values align with your faith

- Maintain a spirit of generosity – Be willing to share your financial blessings with others

Types of Investments and Their “Spiritual Risk”

Not all investments are created equal from a Christian perspective. Here’s a quick rundown:

| Investment Type | “Spiritual Risk” Level | Why? |

|---|---|---|

| Long-term stock investing | Low | Based on sound planning and company performance |

| Day-trading | High | Often resembles gambling with emphasis on luck |

| Retirement accounts | Low | Responsible planning for future needs |

| Options trading | Medium to High | Can be speculative and risky |

| Mutual funds | Low | Diversified ownership in many companies |

Common Questions Christians Ask About Stock Market Investing

“Isn’t all investing just gambling in disguise?”

No! The key differences are:

- Gambling is a zero-sum game (for you to win, someone else must lose)

- Stock market investing can create value for everyone involved

- Wise investing is based on research and patience, not just luck

- Stock ownership represents actual partial ownership in real companies

“What if I invest in companies that do unethical things?”

This is a legitimate concern! Many Christians choose to:

- Invest in faith-based mutual funds that screen out certain industries

- Research company practices before investing

- Focus on companies with strong ethical track records

- Consider ESG (Environmental, Social, Governance) investments

“What about Jesus’s warnings about wealth?”

Jesus definitely warned about the dangers of wealth and materialism. However, he didn’t condemn wealth itself—only making it our god. The key is using wealth responsibly as stewards, not hoarding it selfishly.

Real-World Example: The Parable of the Talents

Jesus’s Parable of the Talents (Matthew 25:14-30) actually provides a biblical case for wise investing! In this story:

- A master gives his servants money (“talents”)

- Two servants invest and double the money

- One servant buries the money, afraid of losing it

- The master praises those who invested and rebukes the one who didn’t

While this parable has spiritual applications about using our gifts for God, it also shows that wise stewardship can include investing to grow resources—not just preserving them.

My Personal Experience with Faith-Based Investing

I’ve struggled with this question myself! When I first started investing, I worried if I was compromising my faith. But after studying Scripture and consulting with Christian financial advisors, I’ve found peace with a balanced approach.

For me, that means:

- Tithing comes first

- Long-term investing, not speculation

- Regular evaluation of where my money goes

- Maintaining generosity regardless of market performance

The Bottom Line: Is Stock Market Investing a Sin?

Based on biblical principles, stock market investing itself is not sinful. The sin potential lies in our approach, attitudes, and priorities.

When we invest with wisdom, patience, and proper perspective—maintaining generosity and keeping God first—investing can be a responsible way to manage the resources God has entrusted to us.

Remember what Proverbs teaches: faithful management can lead to blessing, but frantically chasing wealth leads to trouble. The key is our heart posture and motivations.

Final Thoughts

As Christians, we’re called to be good stewards of everything God gives us—including our finances. Stock market investing can be part of that stewardship when approached with biblical wisdom.

So go ahead and invest if you feel led to—just keep your priorities straight, invest wisely for the long term, and remember that your true treasure isn’t found in your portfolio but in heaven.

What’s your experience with investing as a Christian? Have you found ways to align your investment strategy with your faith? I’d love to hear your thoughts in the comments below!

From Shares to Dividends … and Beyond

Like the investors of the societas, modern stock owners become legal owners of the company whose stock they purchase. However, since the innovations of the DEIC, this “ownership” no longer entails a share in that company’s profits. The DEIC offered their investors dividends, which were not a percentage of the company’s profits (or losses) accrued at the conclusion of a venture—since those, under the terms of the contract, were automatically reinvested in the next venture—but an arbitrarily determined sum of money, regularly paid out to investors, capable of being increased or decreased by the company’s directors as time went on. The difference might seem slight—and indeed, in this early transition from percentages to dividends, the amount paid out in dividends was very high by today’s standards. But it was a radical break with the past and with any direct relationship between the success of an individual investor and the success of the venture in which he invested. Companies no longer needed to pay dividends that were proportional to profits, except by convention or as a way of incentivizing shareholders. In fact, as is the case with many modern companies, they no longer needed to pay dividends at all.[10] This legal sacrifice of one’s share in the profits is the most obvious difference between the company and the societas that preceded it, and it is this sacrifice that firmly separates the secondary market of stock trading from the actual activity of companies: if one has little or no share in the profits, then the only benefit one receives from this ownership is one’s ability to sell it to someone else.

Successful stock-trading is made possible by the profit-producing activity of a given company. But the legal sacrifice of sharing in these profits renders this relationship contingent rather than necessary. Owners of companies, who share in their profits, make more or less money according to the immediate success or failure of the company’s productive activities. Shareholders, who sacrifice their share in the profits, make more or less money to the degree that they can sell their stocks to others, and this ability to sell their place may be affected by the success or failure of the company—or it may not.

The owners of a company have an executive control of its operations and a legal right to the profits it produces. When a company “goes public,” its original owners surrender both of these, in a legal move (appropriately) called a “public offering.” They no longer have a right to the profits; instead, they are given a certain amount of stock. They no longer exert executive control over the company; they typically take part, instead, in a voting board of directors. This board is nothing other than a group of people who also own stock in the company, albeit often a larger amount than the general public. The board of directors has the responsibility of representing all shareholders of the company to ensure that the stock price increases.

The transformation is subtle, but profound: the immediate purpose of a company is no longer fulfilled in the goods it produces and the profits it earns except insofar as those goods and profits increase the capacity of stockholders to sell their stock to another person for more than they paid for it. If, for instance, the board of directors determined that this ability to maximize the future sale of their investment would be better served by a bakery ceasing to bake, and beginning to produce, say, plastic wrap—it could and would be done; Facebook could become Meta. “Going public” unties a company from any particular purpose outside of the production of a higher stock price.[11]

This problem of profits explains a phenomenon seen in companies such as Amazon: the founder and former CEO of the company, Jeff Bezos, received no more than $81,840 as his base pay for the last several years—with no bonuses at all. Elon Musk does not even receive a base salary from Tesla. These CEOs’ sole earnings are the rising prices of their stocks.[12] The person who holds a little Amazon stock and a little Tesla stock is in the same position as Bezos and Musk—just to a lesser degree.

Within economic jargon, the difference “going public” makes can be expressed by the difference between a company’s “book value” (its worth based upon its balance sheet) and its “market value” (the amount for which the company could be sold on the open market). Book value relies on profitability—how a company is performing in its actual production and sale of goods and services.[13] Market value relies on how much stock in the company can be sold for by one stockholder to another.

There is a common perception that a company’s market value is based upon its book value—in other words, that the gains that stockholders receive are related to the productivity of the company. Strictly speaking, this is not the case. Stock traders do speculate (that is, buy stocks) on the basis of the future book value of a company—but only so far as it is a useful data point for predicting its future market value. The underlying factors that the traders consider are possible future market expansion, or possible new products, etc. But this, again, is based on conjecture, and often has no relation to current profitability or even to future profitability, since the real concern of speculators is the future market value of the company. As a result of this, and the increase of people buying into the market and bidding up the price of stocks, a company’s market value can far outweigh its book value. Currently, Tesla’s market value is approximately 40 times larger than its real book value. In 2021, a group of people on Reddit agreed to buy stocks from the stockholders of GameStop—an all but failed video game company whose stock price was sitting around a few dollars. Because of this “demand” for GameStop’s stock, the stock price went up to nearly $500—after the company had just announced a $200 million loss in 2020. Now, in 2022, the stock price has settled around $100: five times its book value per share.[14] In the shoe company All Birds’ recent IPO filing, they disclosed that, “The value of a corporation’s assets can be measured in a number of ways and may not necessarily equal their book value.”[15] The connection between the profitability of a company and the popular perception of the company, between the real and the apparent, can be miles apart.

If the main source of individual monetary gain coming from a company is found in its market value and not its book value (that is, if it is run by stockholders who benefit by an increase in stock price, not by the profits of the company), then the company is going to make decisions based upon how it can increase its perceived value. Being a good company that makes good things and produces profits is still important, but only insofar as it contributes to this perception—only insofar as it leads someone to want to buy stock from the stockholders who control the company. As was obvious in the case of GameStop and Tesla, being a profitable company need not be a factor in producing this perceived value. The buying of stocks can produce this perceived value “all on its own.” Through the secondary market, the primary purpose of a company becomes the production of this perceived value—that is, the purpose becomes what we might call marketing. For the public company, production is simply another form of this marketing. A company might increase the value of its stock by making watches or by saying, via advertisement, that they will make watches.[16]

FROM THE PRINT MAGAZINE:

This essay was originally published in New Polity Issue 4.1 (Winter 2022). As there is a debate on this article in our next issue (4.2) we thought it wise to air our argument here, for further comment.

The majority of Americans own publicly traded stocks.[1] American workers generally depend on stocks for their retirement, through IRAs and 401(k)s. Every Catholic diocese and college in America invests funds in the stock market. Popular wisdom tells us to put our money in the market, saying that “if you’re not investing, you’re losing.” If we do not invest, we are not merely losing out on potential gains, but we are also losing the very value of our money through rampant inflation, which devalues every dollar that “just sits” in the bank. Stock trading is the common activity of the American rich and an increasing necessity for the middle class if they are to maintain their position in society. But what is it?

This is a difficult question to answer—and not merely because one must use economic jargon to do so. The trading of stocks is set up to appear like a straightforward, natural activity. In this way, it is like typing on a computer: one knows that it works, but who could really say how it works? One takes a certain sort of action (the same sort of action, no matter what the stocks in question are) and money comes out. Years of investments simply turn into a retirement payout, or we click “sell” on an app and receive cash in return. But it is necessary to understand the inner workings of this apparently natural process to be sure of what, precisely, is making us money.

Why should we care? First, as a matter of sociality: only by knowing what an activity is can we know what it is doing to the world. Second, as a matter of morality: it behooves us to know whether what is being done to the world, which results in money, involves delivering bagels to the hungry—or building sweatshops in the South Pacific. And finally, as a matter of theology: we praise stock-trading because it makes us money, but this rather leaves out the question of whether it makes us saints. We know what the world thinks of stock-trading: that it is prudent, clever, and increasingly necessary. But what does God think of it?