Have you been saving for retirement for what feels like forever? Yeah, me too After decades of squirreling away cash, the last thing any of us wants is to blow it all on avoidable mistakes. I’ve seen way too many people reach their golden years only to watch their nest egg shrink faster than a wool sweater in hot water

Today, I’m gonna share the biggest retirement money no-nos that could seriously derail your post-work life. Trust me, these aren’t just minor oopsies—these are the financial blunders that keep financial advisors up at night!

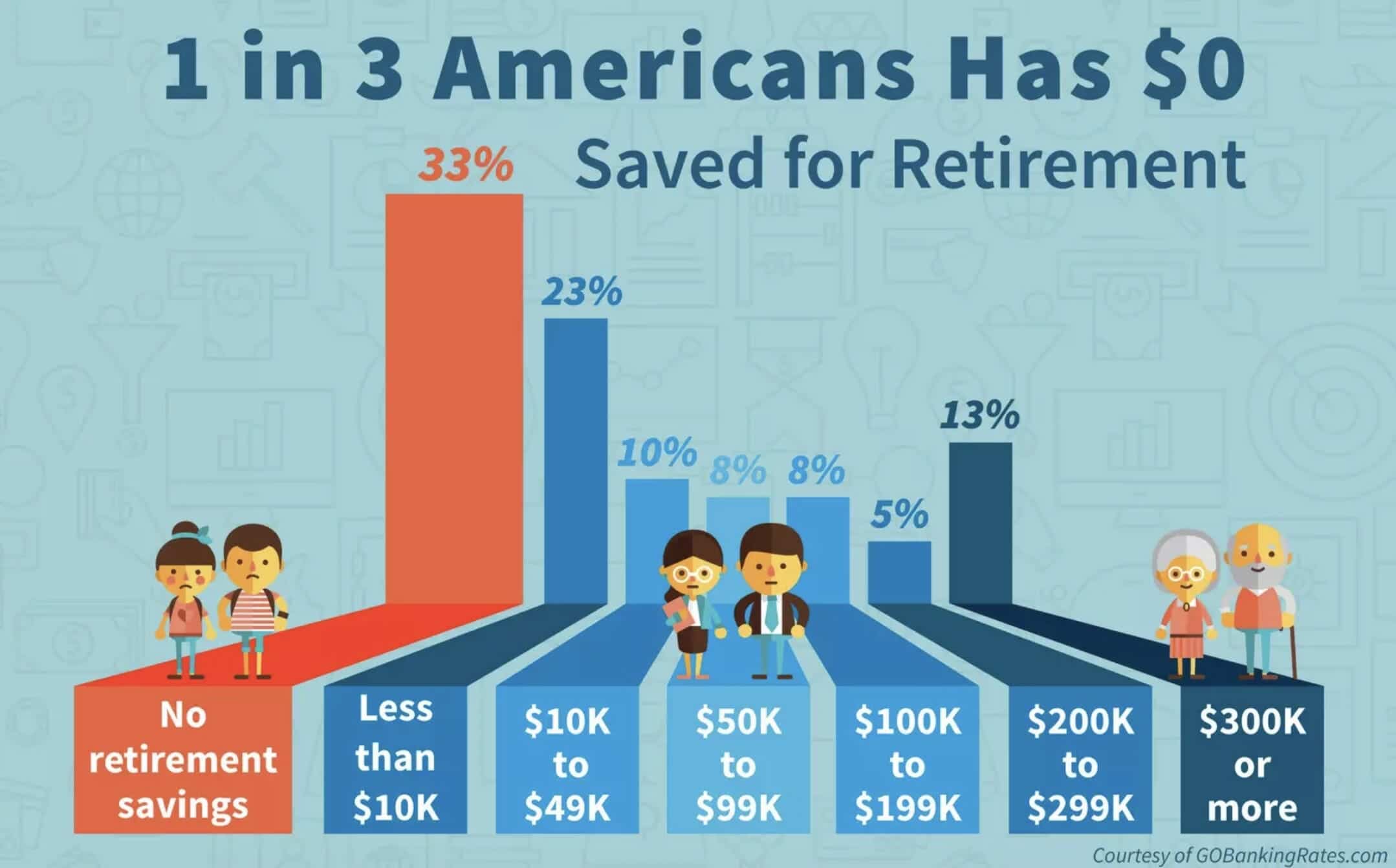

The Scary Truth About Retirement Money Management

Before we dive in, let’s be real about something: most retirees are terrified of outliving their savings. According to the resources I’ve studied, this fear is totally justified. With longer lifespans and rising healthcare costs, your retirement funds need to stretch further than ever before.

The average 65-year-old will need roughly $165,000 just for healthcare expenses in retirement, and a couple would need around $330,000! That’s not pocket change, folks

So let’s look at what you should absolutely NOT do with your retirement money.

Mistake #1: Selling Assets During Market Downturns

One of the most devastating mistakes retirees make is panic-selling during market slumps. Here’s the problem: if your first few years of retirement coincide with a market decline, you might feel pressured to sell more assets to maintain your income level.

This creates a dangerous snowball effect:

- You sell more shares when prices are low

- This leaves fewer shares in your portfolio to recover

- You permanently damage your portfolio’s ability to bounce back

Charles Schwab’s research shows this timing issue clearly. They compared two hypothetical retirees with identical $1 million portfolios, taking identical annual withdrawals starting at $50,000:

Investor 1: Faced a 15% market decline in the first two years, followed by 6% returns thereafter. Their money ran out after just 17 years!

Investor 2: Enjoyed 6% returns for the first eight years, then weathered a 15% decline in years 9-10, before returning to 6% growth. After 20 years, they still had more than $100,000 left!

The lesson? Timing is everything, and early retirement downturns can be devastating.

What to do instead:

- Keep a portion of retirement funds in cash or cash alternatives to cover near-term expenses

- Consider allocating some money to less volatile investments like high-quality, short-term bonds

- Stay flexible with your spending—be willing to reduce expenses during market downturns

Mistake #2: Claiming Social Security Too Early

I get it—the minute you become eligible for Social Security at 62, it’s tempting to start collecting those checks. But hold your horses! Taking benefits before reaching full retirement age (66-67 depending on birth year) means settling for smaller payments FOR LIFE.

Let’s look at the numbers:

- Starting at age 62: Monthly benefit of $1,706

- Waiting until full retirement age (67): Monthly benefit of $2,437 (that’s 30% more!)

- Delaying until age 70: Monthly benefit of $3,022 (a whopping 56% increase!)

Plus, unlike most retirement income sources, Social Security includes cost-of-living adjustments that help combat inflation. Those bigger checks become even more valuable over time.

And don’t worry about Social Security going bankrupt. According to the 2024 Trustees Report, Social Security will be fully funded until 2033. After that, even without Congressional action, it would still pay about 79% of benefits—not ideal, but not zero either.

Mistake #3: Creating an Inefficient Withdrawal Strategy

Many retirees don’t realize that HOW you take money out of your accounts matters just as much as HOW MUCH you withdraw. Poorly planned withdrawals can trigger unnecessary taxes that eat away at your savings.

Watch out for Required Minimum Distributions (RMDs) that kick in at age 73 (75 for those born in 1960 or later). These mandatory withdrawals from tax-deferred accounts like 401(k)s and traditional IRAs can push you into a higher tax bracket, potentially causing:

- Higher taxes on your regular income

- Taxes on your Social Security benefits

- Higher taxes on long-term capital gains and qualified dividends

Smarter withdrawal strategies:

- Consider taking some withdrawals from tax-deferred accounts BEFORE RMD age

- Look into Roth IRA conversions (though be aware you’ll pay taxes on converted amounts)

- Coordinate your withdrawal strategy with a tax professional

Mistake #4: Being Unrealistic About Retirement Expenses

Many folks seriously underestimate how much they’ll spend in retirement. I’ve seen this happen over and over—people assume their expenses will magically drop by 30% or more, but then reality hits.

“A lot of people are not honest with themselves about how much they will spend in retirement,” says Linda Bentley Gillespie, founder of Real World Financial Planning.

To avoid this trap:

- Track your current expenses carefully for at least 6 months

- Factor in new retirement expenses (more travel? new hobbies?)

- Consider which costs might decrease (commuting, work clothes, etc.)

- Don’t forget big-ticket items like healthcare!

Mistake #5: Ignoring the 4% Rule (Or Being Too Rigid With It)

The famous 4% rule suggests withdrawing 4% of your investment portfolio in your first year of retirement, then adjusting that amount for inflation each year after.

Example: With $1 million saved, you’d withdraw $40,000 in year one. If inflation was 3%, you’d take $41,200 in year two.

A November 2023 Morningstar study found that following this approach with a balanced portfolio gives you a 90% chance of having funds left after 30 years. Not bad odds!

But here’s the thing—the 4% rule is just a starting point. As financial advisor Sarah Behr puts it, “No one spends in a straight line.” Most retirees spend more at the beginning (hello, dream trips!) and end of retirement (healthcare), with less spending in between.

Be flexible and adjust as you go. Some years you might need to withdraw more, some years less.

Mistake #6: Paying High Investment Fees

Ok, this one makes me crazy! High investment fees silently drain your retirement savings like a slow leak in your tire. Over decades, even small fee differences can cost you tens or even hundreds of thousands of dollars.

Watch out for:

- Expensive annuities with hefty surrender charges

- Mutual funds with high expense ratios

- Financial advisors charging excessive management fees

Use FINRA’s Fund Analyzer tool to compare the cost of different funds and see how much fees will affect your investments over time. Sometimes the difference is shocking!

Mistake #7: Going on a Retirement Spending Spree

After decades of saving, it’s SO tempting to reward yourself with big purchases right when you retire. New RV! Vacation home! Luxury cruise! But these early splurges can seriously damage your long-term financial security.

Big purchases not only deplete your principal but also reduce the amount that can grow through compounding. Plus, many big-ticket items (boats, RVs, second homes) come with ongoing maintenance costs that drain your finances for years.

Instead of going on a spending spree, consider ways to enjoy retirement without breaking the bank:

- Travel during off-peak seasons for better deals

- Explore local attractions and experiences

- Try a side hustle doing something you enjoy

Speaking of side hustles, bringing in even a small amount of extra income ($10,000 a year) can significantly extend the life of your portfolio. Options include:

- Hosting exchange students

- Pet sitting

- Renting out your home on vacation rental sites

- Freelancing in your area of expertise

Final Thoughts: Your Retirement Money Deserves Better!

Your retirement savings represent decades of hard work and discipline. Don’t let avoidable mistakes undermine all that effort! By avoiding these seven deadly retirement money sins, you’ll dramatically improve your chances of maintaining financial security throughout your golden years.

Remember, it’s not just about how much you’ve saved—it’s about how wisely you manage and protect those funds once you retire.

Have you seen anyone make these retirement mistakes? Or maybe you’ve narrowly avoided one yourself? Drop a comment below—I’d love to hear your experiences!

What TO DO With Your 401k When You RETIRE (5 OPTIONS)

FAQ

What not to do with retirement money?

- Top Ten Financial Mistakes After Retirement.

- 1) Not Changing Lifestyle After Retirement.

- 2) Failing to Move to More Conservative Investments.

- 3) Applying for Social Security Too Early.

- 4) Spending Too Much Money Too Soon.

- 5) Failure To Be Aware Of Frauds and Scams.

- 6) Cashing Out Pension Too Soon.

What is the smartest thing to do with a lump sum of money?

- Keep Some Cash in the Bank. …

- Repay Debt. …

- Top Up Your Pension. …

- Invest for the Future. …

- Provide for the Next Generation.

What is the number one mistake retirees make?

A big common mistake retirees make is not understanding that Social Security benefits can be taxable, depending on a retiree’s total income. Stroup said, “Many retirees forget to account for how their Social Security income will be taxed, which can influence their retirement income strategy.”

What is the $1000 a month rule for retirement?