Buying stock for kids is an excellent way to jump-start their investment portfolio and save for their future.

One of the best ways to set children up for financial success is to introduce and teach important money lessons from an early age. This may mean helping them manage a bank account, explaining the wonders of compound interest, or teaching them about family budgeting.

But while the majority of parents do talk to their kids about money, a much smaller percentage introduce the idea of investing money in the stock market. When you consider how valuable the growth of an investment portfolio could be over a childs lifetime, though, its easy to see why investing with your child might be a great decision.

Lets talk about the different ways you can invest on a minors behalf, where to start, and exactly how to buy stock for a child when youre ready.

Are you thinking about securing your little one’s financial future before they even say their first word? You’re not alone! As a new parent myself, I’ve been researching ways to invest for my baby’s future, and buying stocks is one of the smartest moves we can make Let’s dive into how you can start building wealth for your baby that could potentially grow into something substantial by the time they’re adults

Why Buying Stock for Your Baby Makes Financial Sense

Before we jump into the “how,” let’s talk about the “why” Time is literally the most powerful advantage your baby has when it comes to investing Think about this if you had invested just a few hundred dollars in Amazon when it was $4 a share (like the example in our research), that investment would be worth hundreds of thousands today!

Your baby has:

- Decades of growth potential ahead of them

- Time to ride out market fluctuations (no panic selling!)

- A chance to learn about investing as they grow up

- The benefit of compound interest working its magic

5 Ways to Buy Stock for Your Baby in 2025

Let’s look at the different options available for parents who want to invest on behalf of their little ones:

1. Open a Custodial Brokerage Account (UTMA/UGMA)

This is probably the most popular choice for parents looking to buy stocks for their babies

What it is: A custodial account acts as an irrevocable trust that allows your baby to own assets like stocks, ETFs, or mutual funds while you (the parent or guardian) manage them until your child reaches adulthood (usually 18 or 21, depending on your state).

Popular platforms:

- Stash – Allows purchasing whole or fractional shares starting at just $1. You’ll need their Stash+ plan at $9/month to manage custodial accounts.

- Acorns – Their Early Invest option offers automated investing with ETF-based portfolios (requires Acorns Gold at $12/month)

- UNest – A beginner-friendly option specifically designed for parents building savings for kids

Important note: These accounts are considered your child’s asset, which could potentially impact financial aid eligibility for college later.

2. Gift Individual Stocks

Want to make birthdays and holidays more meaningful? Consider gifting stocks instead of toys that’ll be forgotten in a few months!

How it works: Companies like Stockpile let you purchase gift cards for stocks ranging from $1 to $2,000. You can choose popular companies that might interest your child when they’re older – like Disney, Apple, or Nike.

Your child can track their stocks as they grow and even make approved stock purchases when they’re old enough to understand. When they reach adulthood, the account transfers fully to them.

3. Open a Roth IRA (If Your Baby Has “Income”)

This one’s a bit tricker but worth mentioning.

Requirements: Your baby needs earned income to qualify (yes, really). This could come from modeling, acting, or even “working” in your family business (though be prepared to document this income properly).

Benefits:

- Contributions up to $7,000 in 2024 (or the amount earned, whichever is lower)

- Tax-free growth and withdrawals in retirement

- Can withdraw contributions penalty-free for education or first-home purchase

Since most babies are in a very low tax bracket (ha!), a Roth IRA makes more sense than a Traditional IRA.

4. Try Dividend Reinvestment Plans (DRIPs)

If you want something that’ll grow steadily without much intervention, DRIPs are worth considering.

How they work: You purchase shares directly from a company, and any dividends earned are automatically reinvested to buy more shares. It’s like planting a money tree that grows more branches over time!

DRIPs can be held in a custodial account and transferred to your child when they reach adulthood.

5. Set Up a 529 Plan (Specifically for Education)

If your primary concern is saving for your baby’s future education, a 529 plan is worth exploring.

What it is: A tax-advantaged savings account specifically designed for education expenses (K-12 and college).

Benefits:

- Tax-free growth

- Tax-free withdrawals when used for qualified education expenses

- Available in every state plus DC (though you can choose any state’s plan)

- Can be used for tuition, books, supplies, and more

Consideration: These funds are counted as parental assets on the FAFSA, and some plans are designed for in-state school attendance.

How to Choose the Right Stocks for Your Baby

When selecting investments for your little one, here are some things to consider:

1. Clarify Your Investment Goals

Ask yourself:

- Are you investing primarily for college?

- Do you want to teach your child about investing?

- Are you building long-term wealth beyond education?

Your goals will help determine which investment method makes the most sense.

2. Look at Your Budget Realistically

- Small budget? Platforms like Stash allow fractional shares starting at $1

- Monthly investment? Consider the platform fees versus what you’ll contribute

- Lump sum gift? A DRIP might be more cost-effective than monthly account fees

3. Choose Investments That Might Interest Your Child

If you want to get your child excited about investing as they grow, consider companies they’ll recognize:

- Disney (entertainment they love)

- Apple (tech products they’ll use)

- Nike or other brands they might connect with

- Companies making products for kids (Hasbro, Mattel)

This approach makes the concept of stock ownership more tangible when they’re old enough to understand.

Common Questions About Buying Stock for Babies

Can I really gift stocks to my baby?

Absolutely! You can gift up to $18,000 in 2024 without triggering gift taxes. This can be done through a custodial account, direct stock gifts, or contributions to investment funds on their behalf.

Will I need to pay taxes on stock gifts?

As long as you stay under the annual gift tax exclusion ($18,000 per recipient in 2024), you won’t need to pay gift taxes. However, be aware that any dividends or capital gains in a custodial account may have tax implications that should be reported on your child’s tax return.

What’s the absolute best stock to buy for my baby?

There’s no one-size-fits-all answer here. The “best” stock depends on:

- Your risk tolerance

- Your time horizon (how long before they’ll need the money)

- Your personal values and investment style

Generally, a diversified approach through ETFs or a mixture of stable blue-chip stocks and growth-oriented companies makes sense for most families. Remember, your baby has time on their side, so you can afford to be a bit more aggressive than you might be with your own retirement investments.

My Personal Take on Investing for Babies

When I started investing for my own baby, I decided to go with a combination approach:

- I opened a custodial account where I invest small amounts monthly into a diversified ETF

- For birthdays and holidays, our family gifts individual stocks of companies my child might find interesting when older

- We have a separate 529 plan specifically earmarked for education expenses

This way, we’re covering multiple bases without putting all our eggs in one basket. Plus, I’m excited to use these accounts as teaching tools when my child is older.

Final Thoughts

Investing for your baby is one of the most meaningful financial gifts you can give them. The power of compound interest combined with decades of growth potential means even modest investments could grow substantially by the time they reach adulthood.

Whether you choose a custodial account, gift individual stocks, or opt for education-specific investments, the most important thing is to start. Even small, consistent contributions can add up to significant wealth over your child’s lifetime.

Remember that like any investment, there’s always risk involved. Markets go up and down, and past performance doesn’t guarantee future results. But with a long-term perspective and consistent approach, you’re giving your baby a tremendous head start on their financial journey.

What investment approach are you considering for your little one? I’d love to hear your thoughts!

How to choose a stock for your child

Picking the right investment vehicle (and stocks) for your child depends on a number of personal factors. The best choice may be different from one parent to the next. Here are our recommendations for how to choose a stock for your child.

Are you hoping to foster an interest in investing? Do you want to begin building wealth for your childs future? Or do you hope to fund an education savings vehicle that will grow over time?

Maybe the answer is all three.

Take some time to decide why you want to invest for your child in the first place, and what you primarily hope to gain from the experience. That will help you choose the best investment method.

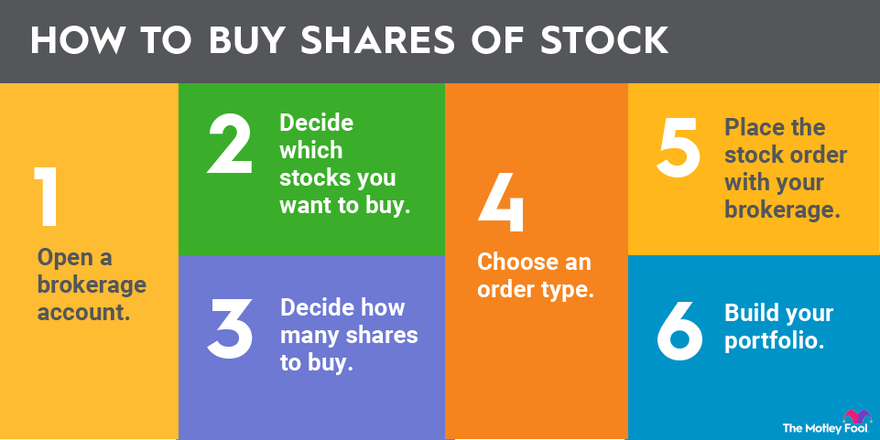

How to buy stock for a child: 5 options

There are a few options to choose from if you are looking to buy stock for a child, whether he or she is your own child or a grandchild, sibling, niece/nephew, etc. Here are five investment routes to consider.