Worried that your retirement strategy might get turned upside down? With all the chatter about Roth IRAs possibly vanishing it’s no wonder many of us are feeling anxious about our future finances. But before you panic let’s dig into what’s really happening with Roth IRAs in 2025.

The Current Status of Roth IRAs and Conversions

Despite recurring rumors and legislative discussions, Roth IRAs are NOT going away in 2025. The same goes for Roth conversions, which remain a completely legal strategy under current federal tax law. This is great news for retirement savers who appreciate the tax-free growth and withdrawals these accounts offer.

What’s causing all the confusion? Previous legislative proposals—particularly those in the Build Back Better Act back in 2021—suggested limiting Roth conversions for high-income earners The proposal would have

- Prohibited Roth conversions for single taxpayers with taxable income over $400,000

- Banned conversions for married couples filing jointly with taxable income over $450,000

- Eliminated “backdoor” and “mega-backdoor” Roth IRA strategies

But here’s the important part these proposals never became law. People can move money from traditional retirement accounts to Roth IRAs without the federal government putting limits on their income after 2025.

Trump’s “Big Beautiful Bill” and Its Impact on Roth Conversions

In August 2025, President Trump’s “big beautiful bill” (officially called the One Big Beautiful Bill Act) made Roth conversions more complicated—but importantly, it didn’t eliminate them.

The legislation made lower federal income tax rates permanent, which is actually good news for those considering Roth conversions. It also introduced several new tax breaks that are temporary (available from 2025 through 2028):

- Deductions for older Americans

- Tax breaks for tipped workers

- Deductions for consumers with overtime pay and car loan interest

These tax breaks have varying earnings limits that could affect your Roth conversion strategy. For instance, the additional $6,000 deduction for older Americans starts to phase out once modified adjusted gross income exceeds $75,000 for single filers or $150,000 for married couples filing jointly.

According to financial experts, it might still make sense to convert funds at 22% or 24% tax rates now—even if it means skipping the $6,000 deduction—to avoid the 30% brackets that could apply to large pre-tax required withdrawals later.

Why Consider a Roth IRA or Roth Conversion?

To understand whether you should worry about Roth IRAs going away, it helps to know why they’re so valuable in the first place.

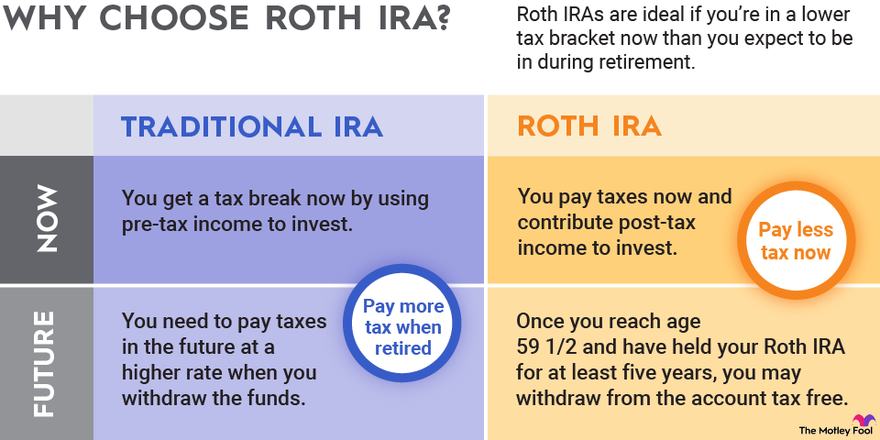

Traditional IRA vs. Roth IRA: The Key Differences

| Feature | Traditional IRA | Roth IRA |

|---|---|---|

| Contributions | Pre-tax money | Post-tax money |

| Withdrawals | Taxed in retirement | Tax-free in retirement |

| Required Minimum Distributions (RMDs) | Yes, starting at age 73 | No RMDs during your lifetime |

| Income Limits | No income limits for contributions | Yes, income limits apply |

One of the best things about Roth IRAs is that qualified withdrawals are tax-free. Also, you won’t have to make any Required Minimum Distributions while you’re alive. This gives you more freedom in retirement.

The “Backdoor” Roth IRA Strategy

If you’re a high-income earner above the Roth IRA contribution limits ($165,000 for individuals and $246,000 for married couples in 2025), the “backdoor” Roth IRA strategy offers a workaround:

- Fund a traditional IRA (which has no income limits)

- Convert those funds to a Roth IRA

- Pay income tax on the converted amount

This strategy remains legal in 2025 despite previous attempts to eliminate it.

When is the Best Time for a Roth Conversion?

If you’re considering a Roth conversion, timing matters. Here are some ideal scenarios:

During Market Downturns

When the market goes down, it can be a great time to convert to a Roth account. You’ll pay less in taxes on the conversion if the value of your traditional IRA is low. If the market goes up again, the money in your new Roth account will grow tax-free.

Before Age 73 (RMD Age)

While you can still do Roth conversions after age 73, it gets more complicated. You must take your Required Minimum Distribution (RMD) before converting any additional amounts to a Roth IRA. And no, a Roth conversion cannot count as your RMD.

When You’re in a Lower Tax Bracket

The ideal time for a conversion is when you’re in a lower tax bracket than you expect to be in during retirement. This often happens in years between retirement and when RMDs begin.

When You Have Cash to Pay the Tax Bill

Don’t forget that you’ll have to pay tax on the new amount in the year it was converted. It’s better to use cash from savings than money from the retirement account to pay this tax.

Strategic Planning Amid Legislative Uncertainty

While Roth IRAs aren’t going away right now, the possibility of future changes means you should approach financial planning with foresight. Here’s how to stay prepared:

- Regularly consult with financial advisors who stay updated on legislative developments

- Evaluate your personal financial situation including current and projected future income and tax rates

- Consider executing conversions sooner rather than later if you’re a high-income earner who might be affected by potential future restrictions

- Spread conversions over several years to avoid bumping into higher tax brackets

Important Roth Conversion Rules to Remember

If you decide to convert, keep these rules in mind:

Ways to Make a Conversion

- Indirect Rollover: Receive a check from your traditional IRA and deposit it into your Roth IRA within 60 days

- Same-Trustee Transfer: If both accounts are at the same institution, request an internal transfer

- Trustee-to-Trustee Transfer: Have your traditional IRA institution send funds directly to your Roth account at a different institution

The Five-Year Rule

You cannot withdraw converted funds before five years without a 10% early withdrawal penalty (unless you’re 59½ or older). Each conversion has its own 5-year clock, which starts on January 1st of the conversion year.

Irreversible Decision

Since 2018, the IRS no longer allows “recharacterization” to reverse your conversion. Once you convert, that decision is final for the tax year.

The Bottom Line: Should You Worry?

While legislative changes are always possible, there’s no immediate threat to Roth IRAs or Roth conversions in 2025. The current political and tax policy landscape suggests that while modifications may come, complete elimination is unlikely.

For most retirement savers, the bigger concern should be optimizing your strategy within the current rules—taking advantage of today’s tax rates and conversion opportunities while they exist.

We believe that with proper planning and the right guidance, Roth IRAs will continue to be a valuable tool in your retirement toolkit for years to come. Don’t let fear of potential changes prevent you from making the best financial decisions for your future!

Have you considered a Roth conversion recently? What factors are most important in your decision? We’d love to hear your thoughts in the comments below!

How to set up a backdoor Roth IRA

There are 2 ways to set up a backdoor Roth IRA:

Option 2: If your 401(k) plan allows, consider a mega backdoor Roth conversion

Some 401(k) plans permit automatic Roth conversions, allowing you to make after-tax contributions that automatically convert to Roth within your accounts.

A mega backdoor Roth IRA conversion takes advantage of the IRSs total 401(k) contribution limit. While your regular 401(k) contributions are capped at $23,500 in 2025 ($31,000 if you’re 50 or older), the IRS allows total annual contributions—including employee deferrals, employer matches, and after-tax contributions—of up to $70,000 total ($77,500 if 50 or older). 2.

This creates a “mega” opportunity because if your 401(k) plan allows it, you can make large after-tax contributions through payroll deductions that far exceed the $7,000 IRA limit. To take advantage of this strategy, your plan must allow after-tax contributions and conversions. Check with your plan administrator.

The Mega ‘Back Door’ Roth IRA is Going Away! What Are Some Alternatives?

FAQ

Are Roth IRAs being eliminated?

No, Roth IRAs are not going away, but there are significant planned changes coming in 2026 that will affect high-income earners by eliminating the “backdoor Roth IRA” strategy, which currently allows them to make Roth IRA contributions indirectly.

Will I lose my Roth IRA if the market crashes?

Given that the money in retirement accounts, including IRAs, is typically invested, the overall value of the account is subject to the whims of the market. That means that if the market experiences a downturn or correction, your Roth IRA balance is likely to decline as well.

What are the changes to the Roth IRA for 2025?

For 2025, individuals eligible for catch-up contributions can contribute an extra $1,000, raising their total contribution limit from $7,000 to $8,000. The increased limit applies to each individual meeting the age requirement, allowing them to accelerate their savings in their Roth IRA accounts.

What are the changes for Roth IRAs in 2026?

Starting in 2026, Americans aged 50 and older earning over $145,000 must make their 401(k) catch-up contributions to a Roth account. This new rule means high-earning older workers will pay taxes on their catch-up contributions upfront, but withdrawals in retirement will be tax-free.

Can a Roth IRA be withdrawn?

Because the money you put into a Roth IRA has already been taxed, you can take it out at any time without having to pay taxes or penalties. Withdrawals of your account’s earnings, however, will be subject to taxes and possible penalties unless you have had a Roth IRA account for at least five years and are at least age 59½ at the time.

Will the government end the Roth IRA program?

The Roth IRA program is growing rapidly, making ever-larger contributions to the nation’s economy. You can be sure that the government doesn’t want to end the program, which is what would happen if withdrawals were taxed. 4.

Are Roth IRA withdrawals taxable?

She has conducted in-depth research on social and economic issues and has also revised and edited educational materials for the Greater Richmond area. Today, they offer some of the best tax advantages of any retirement account. The fear exists, however, that Roth IRA withdrawals might somehow be taxed in the future.

Can you convert a traditional IRA to a Roth IRA?

That’s also why, a few years after the Roth IRA was made, Congress got rid of the rule that said people with incomes above $100,000 couldn’t switch from traditional IRAs to Roth IRAs. Congress wants people to switch from traditional IRAs to Roth IRAs so that taxes can be paid now instead of later.

Should a Roth IRA be taxed?

You already pay tax on your Roth IRA contributions in the year you make them. Taxing Roth IRA withdrawals would effectively kill a source of investment capital for the nation’s economy. Other retirement plans, like 401 (K)s, would be a much richer source of tax revenue. Even if the law were changed, current accounts would probably be exempted.

Will Trump’s new tax cuts make Roth conversions more attractive?

Roth conversions transfer pretax or nondeductible individual retirement account funds to a Roth IRA, which starts future tax-free growth. The trade-off is paying regular income taxes on the converted balance. Trump’s new tax cuts could make Roth conversions more appealing for some investors, experts say.