“Expert verified” means that our Financial Review Board thoroughly evaluated the article for accuracy and clarity. The Review Board comprises a panel of financial experts whose objective is to ensure that our content is always objective and balanced.

Bankrate is always editorially independent. While we adhere to strict , this post may contain references to products from our partners. Heres an explanation for . Our is to ensure everything we publish is objective, accurate and trustworthy. Bankrate logo

Founded in 1976, Bankrate has a long track record of helping people make smart financial choices. We’ve maintained this reputation for over four decades by demystifying the financial decision-making process and giving people confidence in which actions to take next.

Bankrate follows a strict editorial policy, so you can trust that we’re putting your interests first. All of our content is authored by highly qualified professionals and edited by subject matter experts, who ensure everything we publish is objective, accurate and trustworthy.

Our banking reporters and editors focus on the points consumers care about most — the best banks, latest rates, different types of accounts, money-saving tips and more — so you can feel confident as you’re managing your money. Bankrate logo

Bankrate follows a strict editorial policy, so you can trust that we’re putting your interests first. Our award-winning editors and reporters create honest and accurate content to help you make the right financial decisions.

We value your trust. Our mission is to provide readers with accurate and unbiased information, and we have editorial standards in place to ensure that happens. Our editors and reporters thoroughly fact-check editorial content to ensure the information you’re reading is accurate. We maintain a firewall between our advertisers and our editorial team. Our editorial team does not receive direct compensation from our advertisers.

Bankrate’s editorial team writes on behalf of YOU – the reader. Our goal is to give you the best advice to help you make smart personal finance decisions. We follow strict guidelines to ensure that our editorial content is not influenced by advertisers. Our editorial team receives no direct compensation from advertisers, and our content is thoroughly fact-checked to ensure accuracy. So, whether you’re reading an article or a review, you can trust that you’re getting credible and dependable information. Bankrate logo

Having a ding on your credit report from a late payment or missed payment can feel like a dark cloud hanging over your financial future. It can negatively impact your ability to get approved for loans, rent an apartment, or even land your dream job. But what if there was a simple way to get those negative marks removed and give your credit score an instant boost? Enter the goodwill letter – a humble plea sent to creditors asking them to remove derogatory marks from your credit report as a gesture of goodwill.

But do goodwill letters actually work? Can a few politely worded paragraphs really erase years of credit damage? I decided to dig into this credit repair tactic to find out if and when goodwill letters are effective. Here’s what I learned after extensive research.

What Exactly is a Goodwill Letter?

A goodwill letter, sometimes called a “goodwill adjustment letter,” is a letter you send to a creditor or collection agency requesting that they remove a legitimate but negative mark from your credit report This could be a late payment, missed payment, or even an account that was sent to collections

You are essentially asking the creditor to forgive your mistake and “wipe the slate clean” by deleting the derogatory mark from your credit history. It’s called a goodwill letter because you are asking the creditor to do this as an act of goodwill not because you are claiming the information is inaccurate.

Goodwill letters are not the same as disputes. With a dispute, you are saying the negative information is factually incorrect. With a goodwill letter, you are admitting fault for the late or missed payment and asking for mercy.

When Are Goodwill Letters Most Effective?

Goodwill letters tend to work best in specific situations:

-

You have an otherwise excellent credit history If the late payment is a one-off blip in an otherwise spotless credit history, playing up your long track record of responsible credit use may sway the creditor.

-

It was an honest mistake: Everyone slips up occasionally. Explaining that the late payment was due to a one-time issue like a lost payment or incorrect autopay setup can help your case.

-

You’ve fixed the problem: Assuring the creditor that you’ve addressed the root cause of the late payment shows you’ve learned from the experience.

-

There was an extenuating circumstance: Health issues, job loss, or family emergencies are often valid reasons for a late payment. Documentation helps.

-

Smaller credit lines: Local credit union and small bank credit lines may be more open to goodwill letters than large national lenders.

-

Collections accounts: Collectors purchase debt for pennies on the dollar, so you may have luck negotiating directly with them.

When Are Goodwill Letters a Long Shot?

While it never hurts to try a goodwill letter, don’t get your hopes up if:

-

You have a history of late payments and credit issues. Patterns of irresponsible behavior are red flags.

-

The late payment was recent. Let some time pass to show you’ve turned over a new leaf.

-

You have no backup documentation. Letters with proof of medical bills, etc. have more credibility.

-

It’s a large national lender. Big banks often have policies against goodwill adjustments.

-

The debt has been charged off. At that point, the creditor has given up on collecting.

-

You already have a high credit score. One late payment may not impact your scores enough to matter.

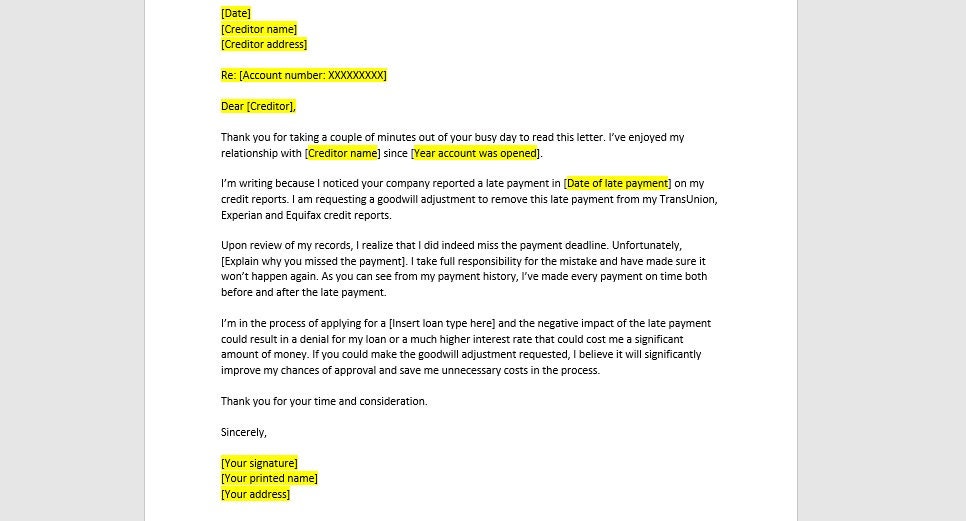

Tips for Writing a Goodwill Letter

If you decide a goodwill letter is worth a shot, here are some tips to make your letter as effective as possible:

-

Highlight your responsible credit history – Remind the creditor that the late payment was an anomaly for you, not the norm. Provide examples of past on-time payments.

-

Keep it short and simple – A brief, polite letter has a better chance of being read than a verbose sob story. Stick to the facts.

-

Take responsibility – Admit fault and acknowledge you understand the late payment was your responsibility. Don’t make excuses.

-

Note the hardship – You can explain extenuating circumstances briefly but don’t dwell on blaming external factors.

-

Emphasize it was a one-time error – Assure the creditor it was an isolated incident that won’t happen again.

-

Be appreciative and complimentary – A little flattery and gratitude for past service can’t hurt your chances.

-

Request a goodwill removal – Politely ask for the specific action of removing the late payment from your credit report.

-

Follow up if necessary – If you don’t receive a response within a month, call or write again. Politely reiterate your request.

How to Send Your Goodwill Letter

You’ll typically have a choice between sending a goodwill letter by email or postal mail.

Email tends to be faster and includes a paper trail of your correspondence. Make sure to send from an email address associated with your account.

Snail mail can take longer but may receive more attention. Send by certified mail so you have delivery confirmation.

Check with the creditor first to see if they have a preference between email or mail. Include your name, account number, and contact information in the letter.

Alternatives if Your Goodwill Request is Denied

Unfortunately, there is no guarantee your goodwill letter will work. The creditor is within their rights to deny your request. Don’t get discouraged if that happens. You still have options, like:

-

Asking again after some time has passed – Six months to a year later, you can try sending another goodwill letter, especially if your credit has improved.

-

Negotiating with collections agencies – Collectors buy debts for pennies on the dollar, so a pay-for-delete agreement is sometimes possible. Get any deal in writing first.

-

Using credit repair services – Legitimate credit repair companies have experience negotiating with creditors on your behalf. Make sure they employ ethical tactics.

-

Focusing on adding positive information – Opening new accounts responsibly and maintaining perfect payment history helps counteract old mistakes.

The Bottom Line – Exercise Cautious Optimism

While certainly not a magic wand, a well-crafted goodwill letter can sometimes convince a creditor to make a “goodwill adjustment” and remove a negative mark from your credit history. This can help boost your credit scores.

But temper your expectations, as creditors are under no obligation to honor your request. Those with otherwise solid credit histories tend to have better luck. Focus on the credit basics – responsible usage, low balances, and flawless payment history – and a goodwill letter may help clean up an old blunder.

How we make money

You have money questions. Bankrate has answers. Our experts have been helping you master your money for over four decades. We continually strive to provide consumers with the expert advice and tools needed to succeed throughout life’s financial journey.

Bankrate follows a strict editorial policy, so you can trust that our content is honest and accurate. Our award-winning editors and reporters create honest and accurate content to help you make the right financial decisions. The content created by our editorial staff is objective, factual, and not influenced by our advertisers.

We’re transparent about how we are able to bring quality content, competitive rates, and useful tools to you by explaining how we make money.

Bankrate.com is an independent, advertising-supported publisher and comparison service. We are compensated in exchange for placement of sponsored products and services, or by you clicking on certain links posted on our site. Therefore, this compensation may impact how, where and in what order products appear within listing categories, except where prohibited by law for our mortgage, home equity and other home lending products. Other factors, such as our own proprietary website rules and whether a product is offered in your area or at your self-selected credit score range, can also impact how and where products appear on this site. While we strive to provide a wide range of offers, Bankrate does not include information about every financial or credit product or service.

- A goodwill letter is a formal written request asking a creditor to remove a negative mark, like a late payment, from your credit report.

- Goodwill letters are most effective if your payment history and credit is generally in good standing.

- Lenders are more likely to respond positively to the letter if the late payment was a one-time incident like an auto payment mix-up or family emergency.

- Lenders aren’t required to reply to a goodwill letter or may have policies against doing so.

Sometimes, despite all of your efforts to pay bills on time, life’s busyness can cause you to miss a payment. That’s always bad news for your credit score, since payment history carries the most weight for how high – or low – your credit score is.

A goodwill letter may allow you to correct a one-time mistake, reversing the damage done to your credit by a missed payment. While there’s no guarantee or requirement for a lender to respond, they may be willing to make a correction if you have a history of paying your bills on time.

How We Make Money

The offers that appear on this site are from companies that compensate us. This compensation may impact how and where products appear on this site, including, for example, the order in which they may appear within the listing categories, except where prohibited by law for our mortgage, home equity and other home lending products. But this compensation does not influence the information we publish, or the reviews that you see on this site. We do not include the universe of companies or financial offers that may be available to you.

- • Mortgage Loan Originator (MLO)

Ribbon Icon

- • Personal loans

- • Debt management

Denny Ceizyk joined the Bankrate Loans team as a Senior Writer in 2023, providing 30 years of insight from his experience in loan sales and as a personal finance writer to help consumers navigate the lending landscape on their financial journeys.

- • Credit cards

- • Debt management

Erin Lowry is the author of the four-part Broke Millennial series, including: Broke Millennial, Broke Millennial Takes On Investing, Broke Millennial Talks Money and Broke Millennial Workbook: Take Control and Get Your Financial Life Together.

At Bankrate, we take the accuracy of our content seriously.

“Expert verified” means that our Financial Review Board thoroughly evaluated the article for accuracy and clarity. The Review Board comprises a panel of financial experts whose objective is to ensure that our content is always objective and balanced.

Their reviews hold us accountable for publishing high-quality and trustworthy content.

Bankrate is always editorially independent. While we adhere to strict , this post may contain references to products from our partners. Heres an explanation for . Our is to ensure everything we publish is objective, accurate and trustworthy. Bankrate logo

Founded in 1976, Bankrate has a long track record of helping people make smart financial choices. We’ve maintained this reputation for over four decades by demystifying the financial decision-making process and giving people confidence in which actions to take next.

Bankrate follows a strict editorial policy, so you can trust that we’re putting your interests first. All of our content is authored by highly qualified professionals and edited by subject matter experts, who ensure everything we publish is objective, accurate and trustworthy.

Our banking reporters and editors focus on the points consumers care about most — the best banks, latest rates, different types of accounts, money-saving tips and more — so you can feel confident as you’re managing your money. Bankrate logo

Bankrate follows a strict editorial policy, so you can trust that we’re putting your interests first. Our award-winning editors and reporters create honest and accurate content to help you make the right financial decisions.

We value your trust. Our mission is to provide readers with accurate and unbiased information, and we have editorial standards in place to ensure that happens. Our editors and reporters thoroughly fact-check editorial content to ensure the information you’re reading is accurate. We maintain a firewall between our advertisers and our editorial team. Our editorial team does not receive direct compensation from our advertisers.

Bankrate’s editorial team writes on behalf of YOU – the reader. Our goal is to give you the best advice to help you make smart personal finance decisions. We follow strict guidelines to ensure that our editorial content is not influenced by advertisers. Our editorial team receives no direct compensation from advertisers, and our content is thoroughly fact-checked to ensure accuracy. So, whether you’re reading an article or a review, you can trust that you’re getting credible and dependable information. Bankrate logo

Goodwill Letters: Do They Work? // Delta Credit Tip

FAQ

How do I send a goodwill letter to my creditor?

- List your account number and address.

- Briefly explain the situation that caused the error.

- Explain the steps you took to correct the issue and ensure it wouldn’t happen again.

- Mention how it’s negatively affecting you, like if it’s hindering your ability to qualify for a mortgage.

Do creditors respond to goodwill letters?

Lenders aren’t required to reply to a goodwill letter or may have policies against doing so.Apr 21, 2025

Can creditors remove late payments?

Has a goodwill letter ever worked?

If a creditor accepts your goodwill letter, it can help you improve your credit score. But the majority of goodwill letters are unsuccessful. This is especially true if you have a payment history with late or missed payments.