FICO Scores are calculated using many different pieces of credit data in your credit report. This data is grouped into five categories: payment history (35%), amounts owed (30%), length of credit history (15%), new credit (10%) and credit mix (10%).

Your FICO Scores consider both positive and negative information in your credit report. The percentages in the chart reflect how important each of the categories is in determining how your FICO Scores are calculated. The importance of these categories may vary from one person to another—well cover that in the next section.

Your FICO credit score is one of the most important numbers in your financial life. It’s used by lenders, creditors, insurers, and others to evaluate your credit risk and determine if you qualify for loans, credit cards, insurance policies, apartments, and more. But figuring out your exact FICO score can be confusing. Here’s a step-by-step guide to understanding and checking your FICO credit score.

What is a FICO Credit Score?

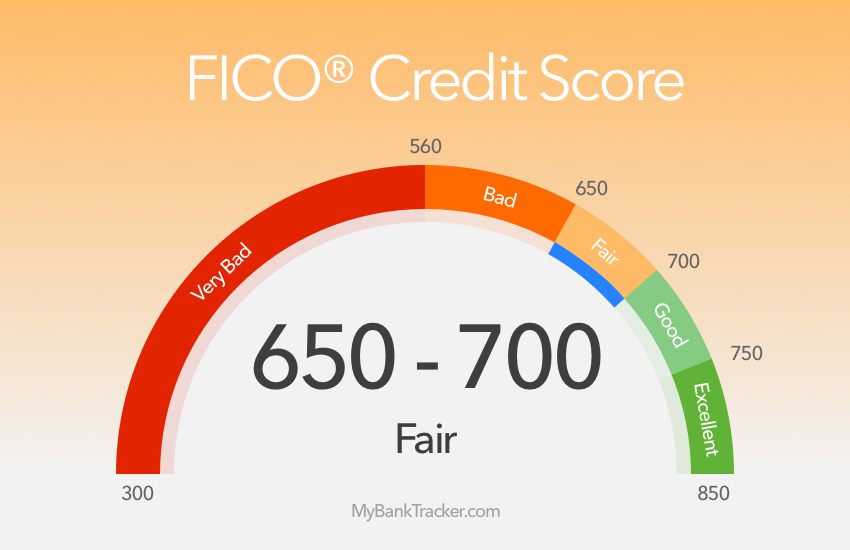

FICO is a data analytics company that created the FICO credit scoring model, which is used by the vast majority of lenders and creditors. FICO scores range from 300 to 850 – the higher the better. Generally, scores above 670 are considered good and scores above 740 are excellent The median FICO score in the U.S. is 716

Your FICO score is calculated based on information in your credit reports from the three major credit bureaus: Experian, Equifax, and TransUnion. It takes into account factors like your payment history, amounts owed, length of credit history, credit mix, and new credit inquiries. Each factor is weighted differently in terms of importance.

Why Your FICO Score Matters

FICO scores give lenders a consistent way to evaluate your creditworthiness The higher your score, the lower your perceived credit risk As a result, people with higher FICO scores tend to get approved for credit and qualify for lower interest rates.

For example someone with a score of 760 may get approved for a credit card with a 10% APR, while someone with a 620 score may only qualify for a card with a 20% APR. Over time that interest rate difference really adds up.

Checking Your FICO Score

Now that you understand what a FICO score is and why it’s important, here are some options for checking your score:

Get Your FICO Score from a Credit Card Company

Many credit card issuers like Bank of America, Chase, Citi, Discover, and Wells Fargo provide free FICO scores on monthly statements or online accounts. However, they may only provide the score used for credit card lending decisions, not mortgage or auto loan scores.

Order Your Credit Reports

You can get a free copy of your credit report from each bureau once per year at annualcreditreport.com. This is required by federal law. Your reports will not include credit scores, but you can pay around $20 per bureau to add your FICO scores.

Use a Free Credit Score Service

Some personal finance sites like Credit Karma and WalletHub offer free credit scores generated from your reports. But be aware these are typically VantageScores, not FICO scores. Lenders may use something different.

Buy Your FICO Scores Directly

For a one-time fee of around $40, you can purchase your FICO scores directly from myFICO.com. This will give you your most accurate, up-to-date FICO scores that lenders are most likely to use.

Sign up for a Credit Monitoring Service

Companies like IdentityForce, PrivacyGuard, and IdentityIQ provide full credit monitoring services for a monthly fee. Along with alerts for suspicious activity, most include access to updated FICO scores from all three bureaus.

5 Tips for Improving Your FICO Credit Score

If your goal is to increase your FICO score, here are some effective ways to do it:

-

Pay all bills on time. Payment history is the biggest factor in your FICO score. Set up autopay or reminders to avoid late payments.

-

Keep credit card balances low. High balances hurt your credit utilization ratio. Try to keep it below 30% on each card.

-

Avoid too many credit inquiries. Only apply for credit when needed to limit hard inquiries. Shop for mortgages or auto loans within a short period to minimize hits.

-

Increase your credit history. Keep old accounts open and maintain a mix of credit types. Getting a new card can help, but get only what you need.

-

Check for errors on your credit reports. Dispute any mistakes with the credit bureaus to keep your reports accurate.

Improving your credit takes time, but following these tips can help boost your FICO score so you get approved for the best loans and credit cards. Be patient, make smart financial decisions, and regularly check your progress.

The Bottom Line

Knowing your FICO credit score is key to managing your financial profile. Scores fluctuate frequently, so check your report and FICO at least every few months. Be wary of any site offering “free” credit scores—make sure they are giving you the FICO. Improving your number takes diligence, but a higher score can save you thousands on interest and open the door to great financial opportunities.

The importance of credit categories varies by person

Your FICO Scores are unique, just like you. They are calculated based on the five categories referenced above, but for some people, the importance of these categories can be different. For example, scores for people who have not been using credit long will be calculated differently than those with a longer credit history.

In addition, as the information in your credit report changes, so does the evaluation of these factors in determining your FICO Scores.

Your credit report and FICO Scores evolve frequently. Because of this, its not possible to measure the exact impact of a single factor in how your FICO Score is calculated without looking at your entire report. Even the levels of importance shown in the FICO Scores chart above are for the general population and may be different for different credit profiles.

Your FICO Scores only look at information in your credit report

Your FICO Score is calculated only from the information in your credit report. However, lenders may look at many things when making a credit decision, such as your income, how long you have worked at your current job, and the kind of credit you are requesting.

How to Get Your FICO Score for FREE

FAQ

How do you calculate your FICO Score?

A FICO score is calculated using information in your credit report, and it’s impossible to calculate it manually. However, you can understand the main factors that influence it.

Is your FICO Score different from your credit score?

Is credit karma your FICO Score?

Credit Karma’s credit scores are VantageScores, a competitor to the more widely used FICO scores. Those scores are based on the information in your credit reports from Equifax and TransUnion, two of the three major credit bureaus.

Where can I get my FICO Score for free?

- American Express.

- Bank of America.

- Capital One.

- Citi.

- Discover.

- Wells Fargo.