Buying a house is an exciting milestone in life. With median home prices hovering around $200000 in many parts of the country, a $200,000 house is a common target for first-time homebuyers. However, coming up with a down payment can be a major hurdle, especially for buyers on a budget. So how much of a down payment do you really need to purchase a $200,000 house? Let’s break it down.

Why a Down Payment Matters

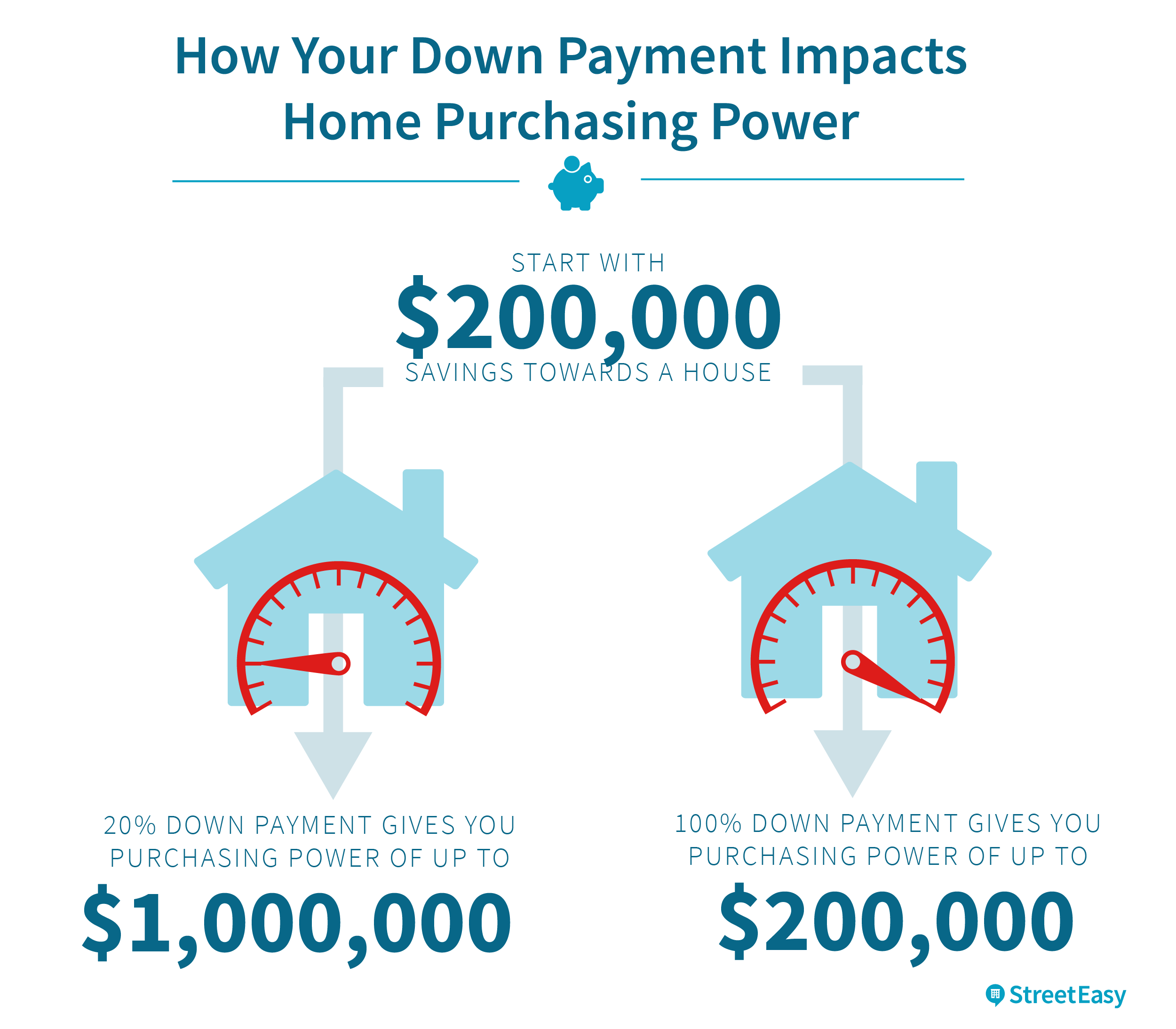

A down payment is the portion of the home’s purchase price that you pay upfront, with the remainder financed through a mortgage loan. Down payments typically range from 3% to 20% of the purchase price.

Making a sizable down payment is important for several reasons:

-

Lower monthly payments A larger down payment means you have to borrow less money This results in lower monthly mortgage payments

-

Avoid PMI If you put down less than 20% you’ll have to pay private mortgage insurance (PMI). This adds to your monthly costs. A 20% down payment lets you avoid PMI.

-

Improve loan eligibility: Lenders view borrowers who make large down payments as lower risk. You’ll have better chances of qualifying for a competitive interest rate.

-

Build equity: More equity in your home right off the bat helps you build wealth faster through appreciation.

Now let’s look at common down payment options for a $200,000 home.

Conventional 20% Down

For a conventional loan with a 20% down payment, you would need $40,000 ($200,000 x 0.20) upfront. This down payment percentage is ideal if you can swing it because:

-

You won’t have to pay PMI, saving you over $100 per month.

-

You’ll get the best interest rates, potentially saving thousands over the loan term.

-

Your monthly mortgage payment will be lower.

However, many buyers struggle to come up with a 20% down payment. Alternatives are available.

FHA 3.5% Down

One popular option is an FHA loan, which only requires a minimum down payment of 3.5%. On a $200,000 home, that equals $7,000 ($200,000 x 0.035).

The benefits of a low 3.5% down FHA loan include:

-

Low barrier to entry for first-time buyers.

-

Smaller impact on your savings.

The tradeoffs are:

-

Monthly mortgage insurance premiums.

-

Slightly higher interest rate than conventional loans.

-

Must pay closing costs out of pocket.

While very low, a 3.5% down payment still gets your foot in the door. You can always refinance to a conventional loan later to eliminate PMI.

10% or 15% Down

If you can save more than 3.5% but less than 20%, a 10% or 15% down payment may be a “Goldilocks” option.

For a $200,000 home:

- 10% is $20,000

- 15% is $30,000

Here are some benefits of 10-15% down:

- Decent monthly payment.

- Lower PMI than 3.5% down.

- Balance of low payment yet substantial equity.

The median down payment in 2020 was 12% according to data from the National Association of Realtors, so 10-15% is a practical target for many.

What if You’re Short on Cash?

Limited savings needn’t stop you from buying if you:

-

Use gift funds – Family gifts can fund part of your down payment.

-

Apply for grants – First-time buyer grants through state/local programs or non-profits. Can get up to $10,000 or more.

-

Borrow against your 401(k) – You can take a loan against your 401(k) for the down payment. Must repay over 5 years.

-

Ask seller for closing cost assistance – Sellers can provide a credit to cover closing costs.

-

Take out a piggyback loan – An 80-10-10 or 80-15-5 loan combines a first and second mortgage, helping reduce down payment needs.

How Much Down Payment Do You Need?

When buying a $200,000 home, the down payment amount that works best depends on your financial situation:

-

Ideally: 20% down keeps your costs lowest long-term.

-

Minimum: 3.5% down with an FHA loan to get in with least savings.

-

In-between: 10-15% down balances equity and savings.

Whichever option you choose, make sure your monthly payment fits comfortably within your budget. Shop around among lenders and brokers to find the best all-around mortgage deal. With smart planning and a moderate down payment, you can make your $200,000 home dream a reality!

Estás ingresando al sitio de U.S. Bank en español Algunos materiales y servicios podrían estar disponibles solamente en inglés. Los enlaces incluidos en esta comunicación podrían dirigirte a sitios web en inglés.

This down payment calculator provides customized information based on the information you provide. But, it also makes some assumptions about mortgage insurance and other costs, which can be significant. It will help you determine what size down payment makes more sense for you given the loan terms.

See how much you might be able to borrow.

A down payment is a portion of the cost of a home that you pay up front. It demonstrates your commitment to investing in your new home. Generally, the more you put down, the lower your interest rate and monthly payment. There are also low or no-down payment options available on certain types of mortgage products, to qualified home buyers. Use this down payment calculator to help you answer the question “how much should my down payment be?”.

Estimated monthly payment and APR example: A $225,000 loan amount with a 30-year term at an interest rate of 3.875% with a down-payment of 20% would result in an estimated monthly payment of $1,058.04 with an Annual Percentage Rate (APR) of 3.946%.1

How much Income do I need to buy a $200k house? #200k #realestate #realestateinvesting

FAQ

How much should I put down for a $200,000 house?

To purchase a $200,000 house, you need a down payment of at least $40,000 (20% of the home price) to avoid PMI on a conventional mortgage.Apr 24, 2025

How much deposit is needed for a $200,000 mortgage?

For a home purchase, you normally need to put down at least 5% or 10% of the total amount. Let’s say you want to buy a property valued at £200,000, your lender may ask for a 10% deposit. This means you would need a deposit of £20,000.

What is the minimum income to buy a 200K house?

To afford a $200,000 house, you typically need an annual income between $50,000 to $65,000, depending on your financial situation, down payment, credit score, and current market conditions.

How much are closing costs for a 200K house?

For example, if your home costs $200,000, you may pay between $4,000 and $10,000 in closing fees.

How much down payment do you need on a house?

There’s no hard-and-fast rule for how much down payment you need on a house. Twenty percent down used to be the norm, but these days you can buy a house with as little as 0-5% down. The down payment you’ll need depends on the type of loan you qualify for and how much you plan to spend on your new home.

How much is the down payment for a 200k house?

A typical down payment is 20% but this really depends on many factors. Speak with a mortgage broker. The amount required to put down is usually determined by the credit worthiness of the borrow as well as the type of property, and the requirements of the lending bank.

Is a 20% down payment required for a home?

A higher down payment can also lower your monthly mortgage payment, reduce the amount of interest paid over time, and potentially improve your chances of loan approval. However, 20% is not a required amount. What is the minimum down payment for a home?

What if I put less than 20% down on a mortgage?

Keep in mind some programs require a minimum credit score. Note: If you put less than 20% down on a conventional loan, you may be required to pay private mortgage insurance (PMI), which can increase your total monthly payment or interest rate. How does my down payment affect my monthly mortgage payments?

What is a 10% down payment on a 350,000 home?

Down payments are usually shown as a percentage of the price. A 10% down payment on a $350,000 home would be $35,000. When applying for a mortgage to buy a house, the down payment is your contribution toward the purchase and represents your initial ownership stake in the home. The mortgage lender provides the rest of the money to buy the property.

Should you use a down payment calculator before buying a home?

The down payment calculator is a good jumping off point; it’ll help you figure out whether you have enough cash saved to start thinking seriously about home buying. But before you start house hunting, you’ll need to check your mortgage eligibility by getting pre-approved for a home loan.