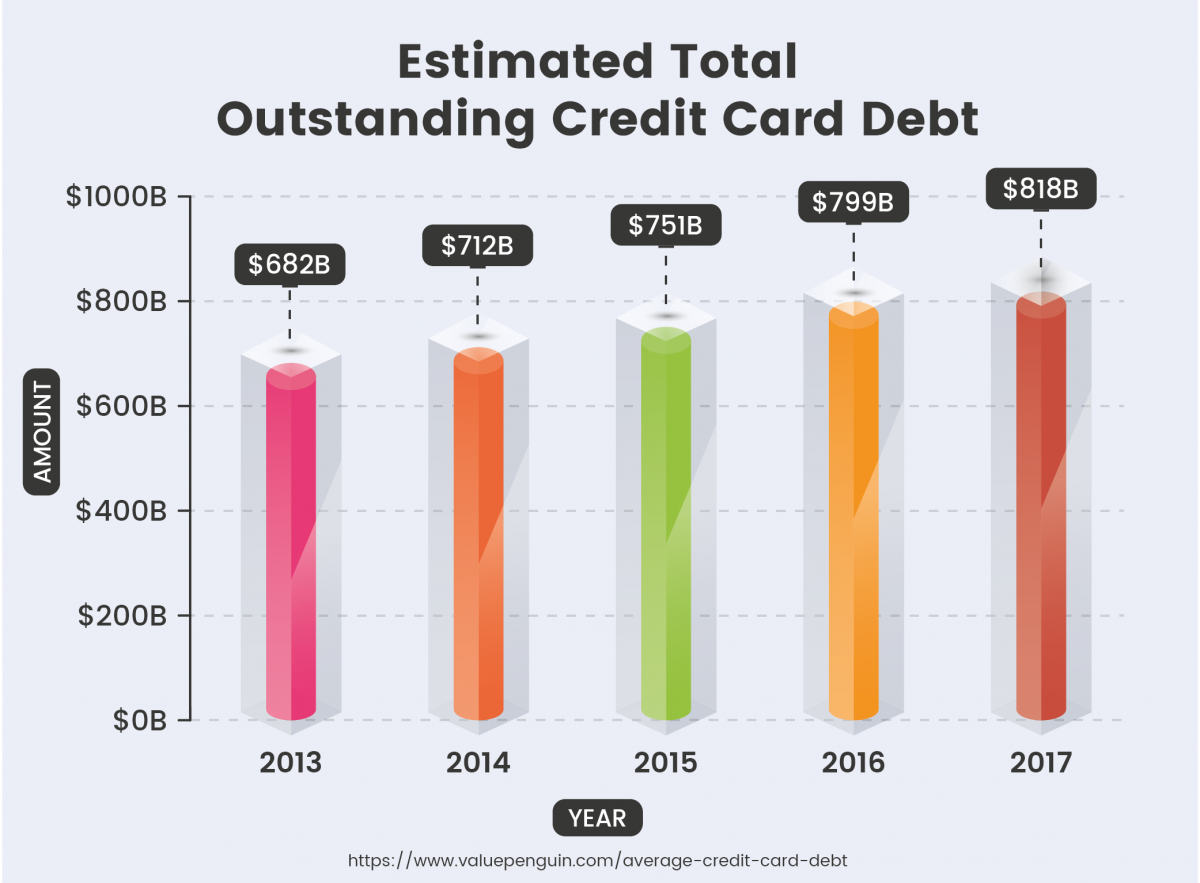

Credit card debt has become an increasingly burdensome issue for many Americans, especially over the last few years. One issue is that the average credit card interest rate is sitting at a record high of 22.76%, according to the latest data from the Federal Reserve. When interest charges are calculated at that high of a rate (or higher), any balance you carry tends to snowball quickly — which is part of why so many cardholders are struggling to manage their debt effectively right now.

If youre carrying a significant balance, like $20,000 in credit card debt, a rate like that could have even more of a detrimental impact on your finances. The longer the balance goes unpaid, the more the interest charges compound, turning what could have been a manageable debt into a hefty financial burden. And the current economic climate, one in which inflationary pressures persist, has only exacerbated this situation.

Thats why its important to pay off what you owe on your credit cards as soon as possible. By doing so, you can set yourself on a better financial path and avoid the many risks that come with letting your credit card debt compound. How long would it take to pay off $20,000 in credit card debt, though? Lets take a look.

Credit card debt is an increasingly common financial burden for many Americans. With high interest rates and easy access to credit, balances can quickly snowball out of control But at what point does your credit card debt become excessive? Is $20,000 a lot?

How Much Credit Card Debt is Considered “A Lot”?

There’s no single threshold that definitively indicates your credit card balances have become too high. However, financial experts generally agree that if your total revolving debt exceeds 10-15% of your annual income, it’s time to take action.

For example, if you earn $50,000 per year, you’d want to keep your credit card balances under $5,000 – $7,500 So for most households, owing $20,000 would be considered a high debt load

Other signs your credit card debt may be too much

- You’re only able to make minimum payments each month

- Your balances are increasing instead of decreasing

- You’re relying on credit cards to cover basic living expenses

- Your credit utilization ratio exceeds 30%

Basically, if your credit card debt feels unmanageable or keeps you from saving and investing, it’s likely time to make some changes.

Why High Balances Are Problematic

Carrying high credit card balances can negatively impact your finances in a few key ways:

-

Costly interest charges – Credit cards have some of the highest interest rates, frequently 19-25%. This can lead to hundreds of dollars per month in interest costs at higher balances.

-

Credit score damage – Increased credit utilization and high balances relative to limits will lower your credit score, making it harder to qualify for loans/credit.

-

Limited flexibility – More of your monthly income gets consumed by minimum payments, leaving less for other goals and expenses.

-

Reduced savings – Money that could have been saved/invested is redirected towards interest fees and debt repayment.

-

Stress and anxiety – Being in debt, especially at high levels, can negatively impact mental health and relationships.

The bottom line is high credit card debt makes it harder to get ahead financially. So what can you do if you find yourself with $20,000 or more in balances?

5 Ways to Tackle $20,000 in Credit Card Debt

If you have $20,000 or more in credit card debt, here are some proven strategies to help eliminate it:

1. Shift to a 0% APR balance transfer card

Balance transfer cards offer a 0% intro APR for 12-21 months, allowing you to pay down balances without accruing new interest. This can save hundreds per month, letting you pay more towards principal. Look for cards with no balance transfer fees.

2. Consolidate with a lower-rate personal loan

Personal loans have fixed rates as low as 5-10% APR. Consolidating credit card debt into a loan can reduce your interest costs and simplify repayment with a single monthly payment.

3. Enroll in a debt management plan

Non-profit credit counseling agencies can negotiate with your creditors to waive fees, reduce rates, and create a consolidated repayment plan. This can make balances more manageable.

4. Consider debt settlement

Debt settlement companies negotiate with creditors to settle accounts for less than what’s owed. This can immediately eliminate balances but may damage credit and have tax implications.

5. Develop a budget and spending plan

Carefully track where your money is going each month, identify areas to cut, and create a budget that frees up cash flow to accelerate debt repayment.

How Long Does it Take to Pay Off $20,000 in Credit Card Debt?

It will take 47 months to pay off $20,000 with payments of $600 per month, assuming the average credit card APR of around 18%. The time it takes to repay a balance depends on:

- The size of your monthly payments

- The interest rate charged

- Whether you take steps to reduce APR

Making just the minimum payments would take nearly 17 years to eliminate $20,000 in credit card debt! That’s why it’s essential to pay more than the minimums and explore strategies to save on interest.

Stay Motivated on Your Debt Repayment Journey

When you owe $20,000 or more, it can feel daunting and hopeless. But numerous Americans have successfully conquered similar debt amounts. You can too with focus and discipline. Here are some tips:

- Celebrate small milestones like paying off your smallest balance

- Envision how you’ll use the extra monthly cash flow once debt-free

- Tell close friends/family about your repayment goals for support and accountability

- Reward yourself occasionally for sticking to your payment plan

- Chart your progress to see balances visibly decreasing each month

Paying off a large credit card debt takes time, but continuing to make payments moves you closer to the finish line each day. Stick with your debt repayment strategy, and you could be debt-free faster than you may think!

Key Takeaways: Is $20,000 in Credit Card Debt a Lot?

- Balances over 10-15% of your income are generally considered excessive

- High balances lead to costly interest, credit score damage, and financial inflexibility

- It will take nearly 4 years to pay off $20,000 making $600 monthly payments at 18% APR

- Shift to 0% cards, consolidate into loans, enroll in DMPs, or try debt settlement

- Stay focused on your repayment goals and celebrate small wins along the way

Owing $20,000 on credit cards may seem overwhelming but it’s still very possible to eliminate this debt through commitment and smart repayment strategies. The sooner you take action, the faster you can regain control of your finances.

A fixed $600 monthly payment

If you increase your monthly payment to $600, heres what you can expect:

- Time to pay off: Approximately 52 months

- Total interest paid: $11,192.20

- Total amount paid: $31,192.20

How long will it take to pay off $20,000 in credit card debt?

Here are a few different repayment scenarios for a $20,000 credit card balance at the current average rate of 22.76%:

I’m $20,000 Behind On 8 Credit Cards!

FAQ

How long does it take to pay off 20k in credit card debt?

How bad is $20,000 in debt?

Being $20,000 in credit card debt doesn’t automatically mean you need to file for bankruptcy but it does mean you should take your situation seriously. Bankruptcy can offer a clean break, but it also comes with long-term consequences for your credit and finances.

What amount is considered a lot of credit card debt?

If your total balance is more than 30% of the total credit limit, you may have too much debt.Dec 19, 2024

How many people have $20,000 in credit card debt?

44% say inflation has “caused them to carry a larger monthly credit card balance.” Of those respondents, 39% have at least $10,000 to $20,000 of credit card debt. That includes 26% of Millennials.