“Expert verified” means that our Financial Review Board thoroughly evaluated the article for accuracy and clarity. The Review Board comprises a panel of financial experts whose objective is to ensure that our content is always objective and balanced.

Bankrate is always editorially independent. While we adhere to strict , this post may contain references to products from our partners. Heres an explanation for . Our is to ensure everything we publish is objective, accurate and trustworthy. Bankrate logo

Founded in 1976, Bankrate has a long track record of helping people make smart financial choices. We’ve maintained this reputation for over four decades by demystifying the financial decision-making process and giving people confidence in which actions to take next.

Bankrate follows a strict editorial policy, so you can trust that we’re putting your interests first. All of our content is authored by highly qualified professionals and edited by subject matter experts, who ensure everything we publish is objective, accurate and trustworthy.

Our mortgage reporters and editors focus on the points consumers care about most — the latest rates, the best lenders, navigating the homebuying process, refinancing your mortgage and more — so you can feel confident when you make decisions as a homebuyer and a homeowner. Bankrate logo

Bankrate follows a strict editorial policy, so you can trust that we’re putting your interests first. Our award-winning editors and reporters create honest and accurate content to help you make the right financial decisions.

We value your trust. Our mission is to provide readers with accurate and unbiased information, and we have editorial standards in place to ensure that happens. Our editors and reporters thoroughly fact-check editorial content to ensure the information you’re reading is accurate. We maintain a firewall between our advertisers and our editorial team. Our editorial team does not receive direct compensation from our advertisers.

Bankrate’s editorial team writes on behalf of YOU – the reader. Our goal is to give you the best advice to help you make smart personal finance decisions. We follow strict guidelines to ensure that our editorial content is not influenced by advertisers. Our editorial team receives no direct compensation from advertisers, and our content is thoroughly fact-checked to ensure accuracy. So, whether you’re reading an article or a review, you can trust that you’re getting credible and dependable information. Bankrate logo

Paying cash for your home’s closing costs seems like a smart financial move. After all, who doesn’t want to save on interest by avoiding a loan? However, financing closing costs isn’t always the wrong choice. Depending on your unique situation, it may make more sense to borrow the money rather than tie up your cash. In this article, we’ll analyze the pros and cons so you can make an informed decision.

What Are Closing Costs?

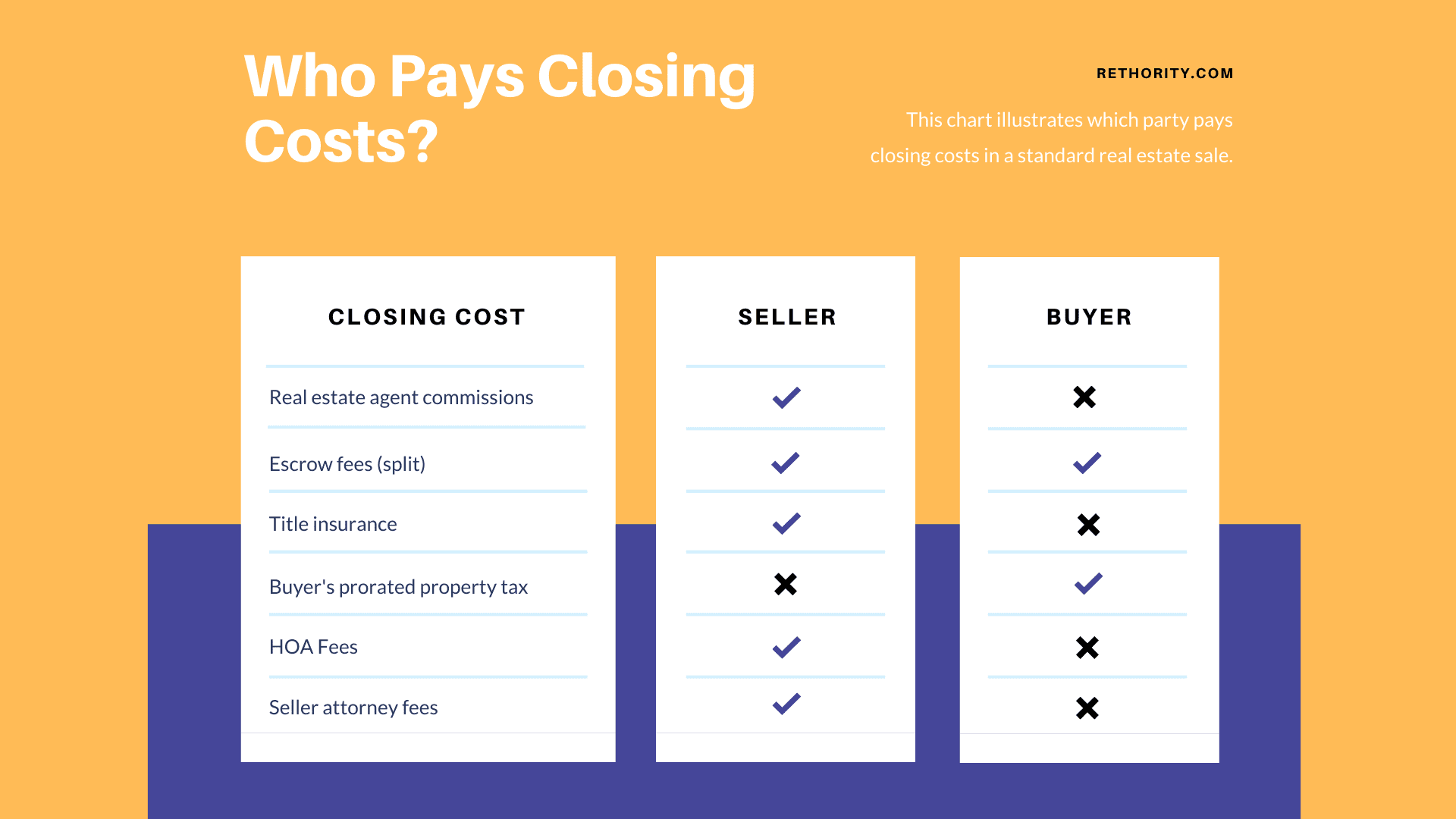

First let’s review what closing costs are. Closing costs are the various fees charged to complete a real estate transaction. They cover services like inspections, title insurance, recording documents transfer taxes, and more. While specific costs vary, buyers can expect to pay 2-5% of the purchase price in closing fees.

Even if you pay cash for the home itself you’ll still owe closing costs. These aren’t connected to financing the purchase price. Rather they facilitate the legal transfer of property ownership. Paying cash doesn’t exempt you from closing fees.

Cash Offers Still Have Closing Costs

A common misconception is that a cash purchase skips closing costs, This simply isn’t true, Here are some closing costs that cash buyers still face

- Title search and title insurance – Validates clean ownership

- Escrow fees – For the neutral third-party transaction manager

- Transfer taxes – Local government fees based on sales price

- Recording fees – To register the deed transfer

- Home inspection – Highly recommended for due diligence

While cash buyers avoid lender fees, costs like these remain. Understanding this prevents unpleasant surprises at closing.

How Much Are Closing Costs?

Closing fees for cash purchasers generally fall between 1-3% of the home’s price. However, specifics depend on factors like:

- Location – Regional regulations impact costs

- Property value – More expensive homes mean higher taxes/fees

- Services chosen – Inspections, surveys add costs

For a $400,000 home, estimate closing costs of $4,000-$12,000. Work with professionals to narrow down your specific expected costs.

Should I Pay Cash or Finance Closing Costs?

Now let’s analyze the decision: should you pay cash or finance closing costs? Here are key factors to weigh:

Cash Benefits

- Avoid interest charges – Paying cash saves money long-term

- Preserve liquidity – Keeping cash reserves provides flexibility

- Strengthen offer – Cash-funded costs appeal to sellers

Financing Benefits

- Conserve capital – Less cash needed at close conserves savings

- Lower down payment – Borrowing costs decreases upfront cash required

- Build credit – Handled properly, financing demonstrates fiscal responsibility

Tips for Deciding Which Approach is Best

With benefits on both sides, how do you decide? Here are some tips:

- Assess interest rates – Weigh cost of borrowing vs. investment returns on capital

- Consider seller incentives – Will cash convince sellers to offer closing help?

- Analyze credit impact – Will smart financing help your credit score?

- Review reserves – Ensure you have emergency funds after closing costs

- Seek professional guidance – Consult your lender, agent, and financial advisor

Thinking through these factors holistically will point you towards the smarter choice. There’s no one-size-fits-all answer.

Strategies to Reduce Closing Costs

Whether you pay cash or finance, minimizing closing costs is wise. Here are proven strategies:

- Negotiate with sellers for closing cost concessions

- Comparison shop service providers like title companies

- Opt out of optional fees like owner’s title insurance

- Seek discounts for bundling services through one company

- Pay property taxes directly rather than through escrow

- Contribute sweat equity for repairs rather than paying contractors

A little creativity goes a long way towards lowering your bottom line!

Consult the Experts

Navigating the decision of paying cash or borrowing for closing costs can be challenging. Don’t go it alone! The right professionals can offer guidance tailored to your unique situation.

- Real estate agents provide localized market insights

- Mortgage brokers analyze financing options and credit impacts

- Financial advisors assess your broader investment portfolio

- Title company representatives detail estimated costs

Armed with expert input, you can determine the optimal approach with confidence.

Weighing the Tradeoffs

Deciding whether to pay cash or finance closing costs demands a holistic outlook. While paying cash saves interest and appeals to sellers, smart financing properly builds credit while retaining capital.

Carefully assess your specific circumstances – credit needs, budget, reserves, and more. Minimize costs where possible. Input from professionals ensures you make the ideal choice to match your financial situation.

With a balanced viewpoint, you can handle closing costs in a way that sets your home purchase up for success!

How We Make Money

The offers that appear on this site are from companies that compensate us. This compensation may impact how and where products appear on this site, including, for example, the order in which they may appear within the listing categories, except where prohibited by law for our mortgage, home equity and other home lending products. But this compensation does not influence the information we publish, or the reviews that you see on this site. We do not include the universe of companies or financial offers that may be available to you.

- • Personal finance

- • Taxes

Allison Martin is a contributor to Bankrate covering personal finance, including taxes, mortgages, auto loans and small business loans. Martin’s work began over 10 years ago as a digital content strategist, and she’s since been published in several leading outlets, including The Wall Street Journal, MSN Money, MoneyTalksNews, Investopedia, Experian and Credit.com. Martin, a Certified Financial Education Instructor (CFE), also shares her passion for financial literacy and entrepreneurship with others through interactive workshops and programs.

- • Real Estate

- • Housing Market

Michele Petry is a senior editor for Bankrate, leading the site’s real estate content.

- • Credit cards

- • Debt management

Erin Lowry is the author of the four-part Broke Millennial series, including: Broke Millennial, Broke Millennial Takes On Investing, Broke Millennial Talks Money and Broke Millennial Workbook: Take Control and Get Your Financial Life Together.

At Bankrate, we take the accuracy of our content seriously.

“Expert verified” means that our Financial Review Board thoroughly evaluated the article for accuracy and clarity. The Review Board comprises a panel of financial experts whose objective is to ensure that our content is always objective and balanced.

Their reviews hold us accountable for publishing high-quality and trustworthy content.

Bankrate is always editorially independent. While we adhere to strict , this post may contain references to products from our partners. Heres an explanation for . Our is to ensure everything we publish is objective, accurate and trustworthy. Bankrate logo

Founded in 1976, Bankrate has a long track record of helping people make smart financial choices. We’ve maintained this reputation for over four decades by demystifying the financial decision-making process and giving people confidence in which actions to take next.

Bankrate follows a strict editorial policy, so you can trust that we’re putting your interests first. All of our content is authored by highly qualified professionals and edited by subject matter experts, who ensure everything we publish is objective, accurate and trustworthy.

Our mortgage reporters and editors focus on the points consumers care about most — the latest rates, the best lenders, navigating the homebuying process, refinancing your mortgage and more — so you can feel confident when you make decisions as a homebuyer and a homeowner. Bankrate logo

Bankrate follows a strict editorial policy, so you can trust that we’re putting your interests first. Our award-winning editors and reporters create honest and accurate content to help you make the right financial decisions.

We value your trust. Our mission is to provide readers with accurate and unbiased information, and we have editorial standards in place to ensure that happens. Our editors and reporters thoroughly fact-check editorial content to ensure the information you’re reading is accurate. We maintain a firewall between our advertisers and our editorial team. Our editorial team does not receive direct compensation from our advertisers.

Bankrate’s editorial team writes on behalf of YOU – the reader. Our goal is to give you the best advice to help you make smart personal finance decisions. We follow strict guidelines to ensure that our editorial content is not influenced by advertisers. Our editorial team receives no direct compensation from advertisers, and our content is thoroughly fact-checked to ensure accuracy. So, whether you’re reading an article or a review, you can trust that you’re getting credible and dependable information. Bankrate logo

Lower your long-term costs

Along with saving on upfront fees, paying in cash means you won’t be charged interest, which adds up to huge savings. For example, let’s say you’re comparing a $425,000 cash offer with a $340,000 30-year mortgage (a loan on the same home after 20 percent down) with a 6.5 percent interest rate. Over the course of that loan, Bankrate’s mortgage calculator shows you would pay nearly $433,651 in interest, for a total cost of $773,651.

Save Your Money: Tips for Making Sellers Pay Your Closing Costs

FAQ

Is cash acceptable for closing costs?

Though your lender may accept actual cash during your closing, it’s not a recommended payment method. Using paper money to pay for your closing may set off questions about where the money came from. Some title companies and mortgage providers have banned cash payments during closing.Mar 12, 2024

Do cash offers close faster?

How much are closing costs if you pay cash?

Even if you’re buying a home with cash, the one-time closing costs, or fees you’ll have to pay during the closing process, can be as much as 3% of the purchase price, according to Lee Dworshak, a real estate agent with Keller Williams LA Harbor Realty.

Is it better to pay for a house in cash or mortgage?

Key takeaways. Paying for a house in cash can speed up the buying process, lower your long-term costs and give you instant 100 percent home equity. Getting a mortgage, on the other hand, allows you to save that cash for other financial goals, offers tax deductions and can enhance your credit score.