Your credit score is one of the most important factors that lenders consider when deciding whether to approve you for a loan. It provides a snapshot of your creditworthiness and allows lenders to evaluate the risk of lending to you. If you have a credit score of 680, you may be wondering how much you can borrow. In this article, we’ll break down what a 680 credit score means and how it impacts the loan amounts you may qualify for.

What Does a 680 Credit Score Mean?

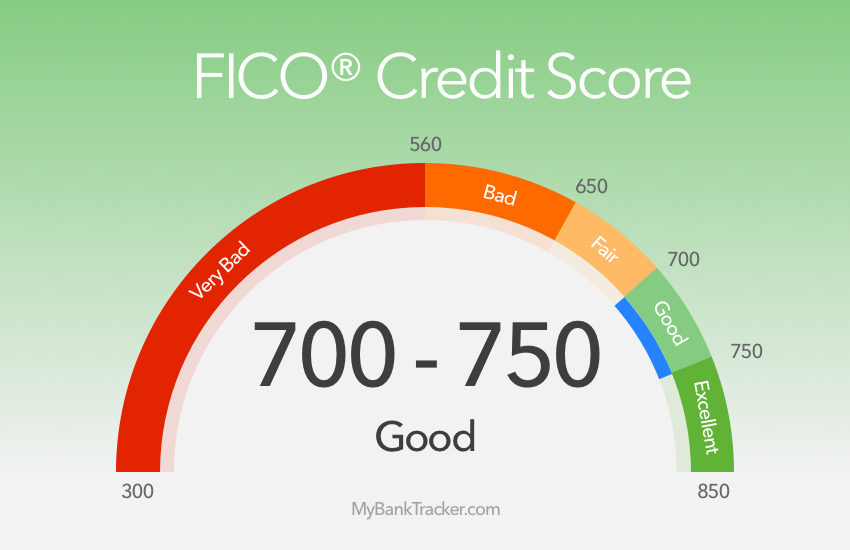

A 680 credit score is considered to be in the fair credit range. Here is a breakdown of the credit score ranges according to FICO one of the main scoring models

- 800-850: Exceptional

- 740-799: Very Good

- 670-739: Good

- 580-669: Fair

- 300-579: Poor

So a 680 score puts you on the higher end of the fair credit range While it’s not an excellent score, it’s still decent With some work, you can likely improve it to good or very good over time.

Credit scores are calculated based on the information in your credit reports from the three major credit bureaus – Equifax, Experian, and TransUnion. Key factors that influence your score include:

-

Payment history – Have you paid your bills on time? Late payments can negatively impact your score.

-

Credit utilization – What percentage of your available credit are you using? The lower the better.

-

Credit history length – In general, a longer credit history with good standing is better.

-

Credit mix – Having different types of credit (credit cards, installment loans, mortgages, etc) can help.

-

New credit – Opening a lot of new credit accounts in a short period can lower your score.

So a 680 credit score indicates you likely have a fair mix of credit accounts with a reasonable payment history. But you may have some late payments or a high balance on your credit cards. There’s room for improvement, but a 680 is still a decent score for qualifying for loans.

Loan Amounts You May Qualify For

The exact loan amount you can qualify for depends on several factors:

-

Your income – Lenders want to see you have enough income to afford the monthly payments.

-

Your existing debts – The higher your existing debts and monthly obligations, the lower the new loan amount you may qualify for.

-

Type of loan – Requirements vary based on whether it’s a mortgage, auto loan, personal loan, etc.

-

Down payment – For mortgages and auto loans, a larger down payment increases the amount you can borrow.

-

Lender requirements – Each lender sets their own credit score and debt-to-income requirements.

That said, here are some general guidelines on loan amounts associated with a 680 credit score:

Mortgages

-

Conforming loan – Up to $647,200. Conforming loans meet the loan limits set by Fannie Mae and Freddie Mac.

-

Jumbo loan – Over $647,200. May be more challenging with a 680 score.

-

FHA loan – Up to $420,680. FHA has more flexible credit requirements.

With a 10-20% down payment, you may qualify for a mortgage 2-3 times your annual income with a 680 score. The exact amount depends on your location, existing debts, and the lender.

Auto Loans

-

New car – $15,000 – $50,000. A 680 score is generally sufficient for most new car loans.

-

Used car – Up to $20,000. Used car loans have lower maximums.

With a 680 credit score, you can likely get approved for an auto loan amount equal to 30-50% of your annual income.

Personal Loans

- $1,000 – $50,000. Many lenders offer personal loans up to $50,000 with minimum scores between 620-680.

With good income and low existing debts, you may qualify for a personal loan up to 30% of your annual salary with a 680 credit score.

Student Loans

Most federal and private student loans don’t require a credit check. Loan amounts are based on school costs, expected family contribution, and other aid received.

Ways to Potentially Increase Your Loan Amount

If you need to borrow more than what your 680 credit score will qualify you for, here are some tips:

-

Shop around – Compare quotes from multiple lenders. Each will have their own requirements.

-

Ask for exceptions – Some lenders may grant exceptions for strong payment history or income.

-

Add a cosigner – Adding a cosigner with better credit can help you qualify for a larger loan.

-

Make a larger down payment – Coming up with a down payment of 20% or more can allow you to borrow more.

-

Pay down debts – Reducing credit card balances and other debts boosts the amount you can borrow.

-

Build credit – Give your credit score a boost by responsibly managing credit and paying bills on time.

The Takeaway

A credit score of 680 puts you in the fair range, enabling you to qualify for most mortgages, auto loans, and personal loans – but perhaps not as large as if your score was over 700. Each lender will make their decision based on their own lending criteria. Improving your credit score and paying down debts can help increase the loan amounts available to you. But even with a 680 FICO score, you should still have decent loan options. Monitor your credit, make payments on time, and practice good credit management habits to obtain the best loan terms.

What actually affects your credit score?

Find out the truth about the things that do and don’t impact your credit score.

What’s your desired loan term? Loan term

Current U.S. Bank clients can select a loan term up to 84 months. For those who aren’t current U.S. Bank clients, the maximum term length is 60 months.

Save 0.50% when you autopay from a U.S. Bank or external personal checking or savings account.

Unfortunately we cant offer you a loan term of that length. Please enter a shorter term.

After you’ve entered your details, choose Calculate for your result.

How Much Can I Borrow With A 680 Credit Score? – CreditGuide360.com

FAQ

How much of a personal loan can I get with a 680 credit score?

| Credit score range | Average APR | Average loan amount |

|---|---|---|

| 680-719 | 29.96% | $15,077 |

| 660-679 | 42.87% | $10,695 |

| 640-659 | 53.56% | $8,422 |

| 620-639 | 71.45% | $6,256 |

What credit score is needed for a $10,000 loan?

What kind of home loan can I get with a 680 credit score?

What credit score do you need for a $25,000 car loan?

The credit score required and other eligibility factors for buying a car vary by lender and loan terms. Still, you typically need a good credit score of 661 or higher to qualify for an auto loan. About 71% of vehicle financing is for borrowers with credit scores of 661 or higher, according to Experian.