The current average mortgage rate for someone with a good credit score (700) was 7.42% as of January 3, 2025, according to Curinos data. Your credit scores can directly impact your eligibility for a mortgage and the interest rate you receive. You may need a score in the high 700s (or higher) to get the best interest rate.

The current average mortgage rate on a conventional 30-year fixed-rate mortgage for someone with a good credit score of 700 was 7.42% as of January 3, 2025, according to Curinos data. You generally need a credit score of at least 580 to qualify for a mortgage, and a score of 760 or higher to get the best interest rate.

Your credit score is one of the most important factors lenders consider when determining the interest rate you will pay on loans and credit cards. A 590 credit score is considered fair, which means you will likely pay higher interest rates than borrowers with good or excellent credit. However, a 590 credit score does not necessarily preclude you from getting approved or securing a reasonable rate.

In this comprehensive guide, we will cover everything you need to know about what interest rate you can expect with a 590 credit score.

What Does a 590 Credit Score Mean?

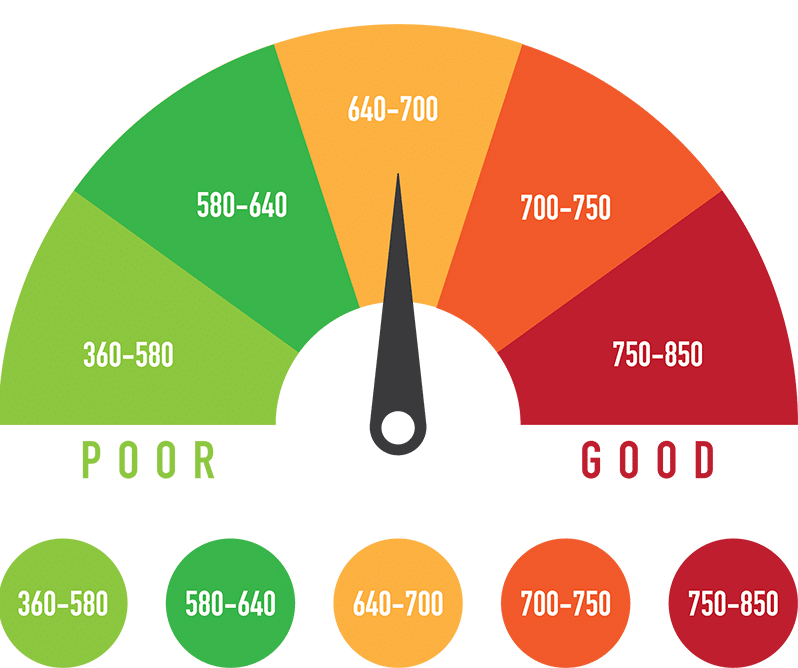

Credit scores generally range from 300 to 850 Scores are grouped into the following ranges

- 800-850: Exceptional

- 740-799: Very Good

- 670-739: Good

- 580-669: Fair

- 300-579: Very Poor

A 590 credit score falls into the fair range It is below the average credit score of around 690 With a 590 score, you will likely face challenges getting approved for credit and will pay higher interest rates compared to borrowers with good or excellent credit.

Lenders view a 590 credit score as an indication that you pose a moderate to high risk. You likely have some missed or late payments on your credit history. Your credit utilization ratio – the percentage of your total available credit that you are using – is likely high. You may even have collections accounts or judgments against you.

While a 590 is not a terrible score, it makes getting approved for credit more difficult. You will have fewer lenders willing to work with you and you will not qualify for the best rates. However, there are still financing options available at this score level if you shop around.

What Interest Rates Can You Get with a 590 Credit Score?

The exact interest rate you will pay with a 590 credit score depends on several factors:

- The type of loan or credit you are seeking

- Economic conditions

- The lender

- Additional factors like your income, existing debts, down payment amount, etc.

While your precise rate will vary, here are some general guidelines on the average interest rates you can expect with a 590 credit score based on credit type:

Credit Cards

- Interest rates: 18% – 22%

- Annual fees: $75 – $99

With a 590 score, you will likely only qualify for secured credit cards which require a refundable security deposit. Interest rates will be high compared to unsecured cards.

Auto Loans

- New car loans: 13% – 15%

- Used car loans: 15% – 22%

You can get approved for an auto loan with a 590 credit score, but expect to put down a larger down payment and pay a higher rate.

Mortgages

- Interest rates: 6% – 8%

A 590 credit score makes getting a mortgage difficult, but FHA loans are possible with a large down payment. You will pay higher mortgage insurance premiums.

Personal Loans

- Interest rates: 15% – 36%

Personal loan options will be limited and you’ll pay higher rates compared to borrowers with good credit. Short repayment terms are also likely.

Student Loans

Most federal student loans are not based on credit scores. However, you will pay higher rates on private student loans.

Factors That Determine Your Interest Rate

In addition to your credit score, lenders look at other criteria when setting interest rates, including:

-

Type of lender – Online lenders, credit unions, banks, and car dealerships set their own rates.

-

Loan amount – The more you borrow, the higher your rate.

-

Loan term – Longer repayment terms mean higher rates.

-

Your income – Insufficient income increases risk for lenders.

-

Your existing debts – Too much existing debt burdens your finances.

-

Down payment size – Larger down payments reduce risk for lenders.

-

Collateral – Loans backed by collateral like cars or homes get better rates.

-

Economic factors – When the economy improves, rates tend to go down.

While you can’t control all these factors, being aware of them can help you get the lowest rate possible.

How to Get a Better Interest Rate

If you want to get better interest rates than those available with a 590 credit score, here are some steps to take:

-

Shop around – Compare offers from multiple lenders. Don’t assume one will give the best rate.

-

Improve your credit – Increasing your score to over 620 can significantly improve loan terms.

-

Make a larger down payment – The more you can put down as a down payment, the better your rate.

-

Get a cosigner – Adding a cosigner with excellent credit can help you qualify for lower rates.

-

Choose shorter loan terms – Opt for a 15-year mortgage over a 30-year term, for example.

-

Lower your debt-to-income ratio – Pay down debts so you have less existing obligations.

-

Wait for special financing offers – Dealerships and lenders periodically offer special rate promotions.

With some work, you may be able to improve your credit score and qualify for better loan terms over time. But even at a 590 score, you still have financing options to achieve your goals. The key is shopping around and getting pre-approved so you can compare your actual loan offers. Be sure to weigh interest rates and fees carefully as you evaluate loan providers.

The Bottom Line

-

A 590 credit score is considered fair and will make getting approved for financing more challenging.

-

You can expect higher interest rates compared to borrowers with good credit – generally in the 15% – 22% range depending on loan type.

-

Your exact rate will depend on many factors including your income, debts, collateral, credit history and economic conditions.

-

Take steps to improve your credit and shop around with multiple lenders to get the most competitive interest rate possible.

While a 590 credit score presents some obstacles, focus on rehabilitating your credit over time, make financially wise decisions, and explore all of your options. There are still loans available to you even if your score is not yet where you want it to be. With some diligence, you can secure financing to move forward with major purchases or investments.

How to Improve Your Credit Score

There are many potential ways to improve your credit scores. The specifics will depend on whats affecting your credits cores today, but make an effort to:

You may also want to hold off on applying for new credit cards or loans if youre looking for a mortgage. Each application can lead to a hard inquiry and new accounts can lower the average age of your credit accountsâboth of these could hurt your credit scores a little. The additional monthly payment could also increase your DTI, which could make it harder or more expensive to get a mortgage.

How Credit Scores Can Affect Your Mortgage

Lenders consider many factors when reviewing your mortgage application, and theres often a minimum credit score requirement. Once youre above the minimum, a higher credit score could help you qualify for a mortgage with:

- Lower interest rate

- Higher loan limit

- Smaller down payment

- Higher debt-to-income ratio (DTI)

- Lower fees

In short, a higher credit score can make getting a mortgage easierâand cheaper. The most commonly used credit scoring models top out at 850, but you dont need a perfect score to get the best loan offer. Mortgage lenders tend to offer the best rates and terms to everyone who has a score above a certain point, such as 740 or 780.

Can I Get A Loan With A 590 Credit Score? – CreditGuide360.com

FAQ

What is the interest rate for a 590 credit score?

And with a score of 590-619, the average rate was 15.92%. It’s also worth mentioning that interest rates can vary significantly among lenders, even for borrowers with the exact same credit score. And this is especially true for borrowers in the subprime credit tiers (below-average credit scores).

What can a 590 credit score get you?

Credit Rating: 590 is considered a bad credit score. Borrowing Options: Most borrowing options are available, but the terms are unlikely to be attractive. For example, you could borrow a small amount with certain unsecured credit cards or a personal loan for damaged credit, but the interest rate is likely to be high.

What credit score is needed for a $30,000 car loan?

There’s no minimum credit score required to get an auto loan. However, a credit score of 661 or above—considered a prime VantageScore® credit score—will generally improve your chances of getting approved with favorable terms. For the FICO® Score Θ , a good credit score is 670 or higher.

What credit score is needed for a $300,000 loan?

To buy a $300K house, you typically need a credit score of at least 580 for an FHA loan or 620 for a conventional loan. A higher score—around 720 or more—can help you qualify for better interest rates. How much is the down payment for a $300K house?