Your credit score is more than just a number—it’s a key that can unlock financial opportunities or keep them out of reach. A 611 credit score is below the national average credit score and may limit your access to favorable loan terms, but it’s far from the end of the road. In this guide, we’ll break down what a 611 credit score means, how your credit score impacts your financial health, and actionable steps to improve your credit score. If you’re ready to take charge of your credit, Dovly is here to help.

A FICO score of 611 falls in the “fair” credit score range, which means it is below what is typically considered a “good” credit score. While a 611 credit score indicates there is room for improvement, it is still possible to qualify for credit and loans with strategic planning and diligent financial habits. This article will examine what a 611 credit score means, how it’s calculated, and practical tips for raising your score over time.

What Does a 611 Credit Score Mean?

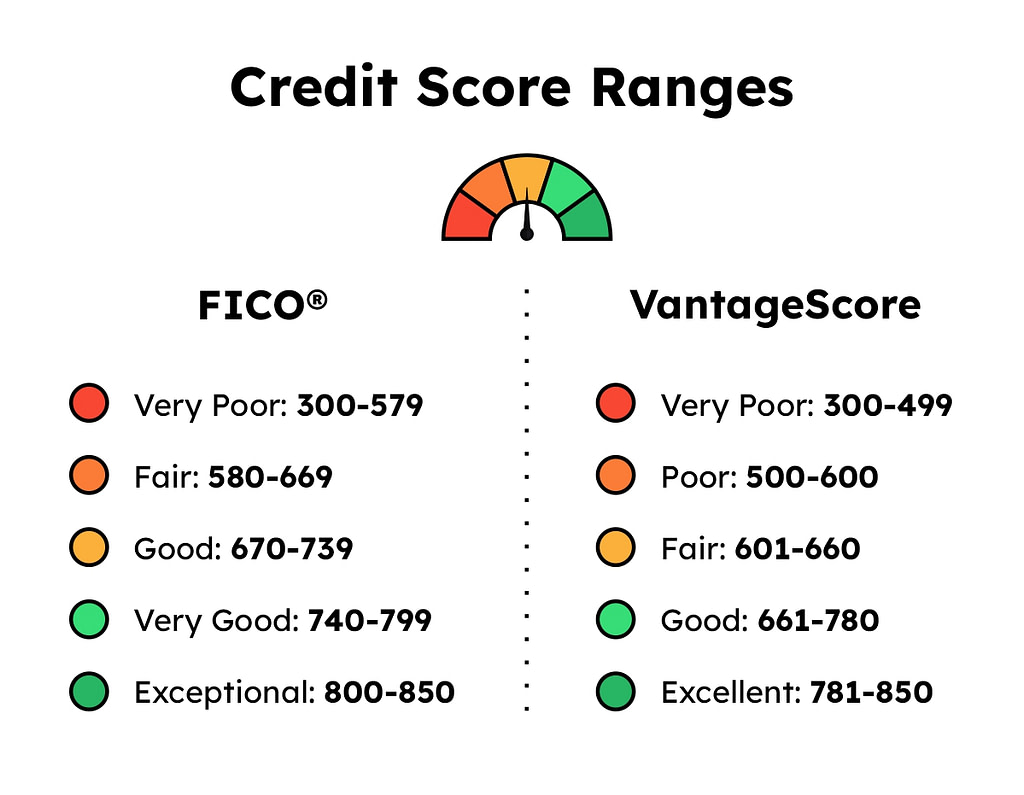

FICO scores range from 300 to 850, with higher scores indicating lower credit risk to lenders. Here is how the score ranges generally break down:

- 300-579: Poor

- 580-669: Fair

- 670-739: Good

- 740-799: Very Good

- 800-850: Exceptional

A 611 FICO score is in the bottom part of the fair range, just 29 points above what is considered poor credit. While not a terrible score, potential lenders may view applicants with a 611 as riskier borrowers who are more likely to default on a loan.

You may face higher interest rates, lower credit limits, or more difficulty getting approved for financing if your score is 611 However, it is still possible to qualify for credit cards, auto loans, mortgages, and other lending products with strategic planning

How is a 611 Credit Score Calculated?

FICO credit scores are calculated based on information in your credit reports at the three major bureaus – Equifax, Experian, and TransUnion. Several factors influence your score, including:

- Payment history (35%) – Presence of late payments, bankruptcies, foreclosures, etc. A 611 score likely has some late payments.

- Credit utilization (30%) – Percentage of available credit being used. Averaging 57% utilization with a 611 score.

- Length of credit history (15%) – Typically just 2-3 years with a 611 score.

- Credit mix (10%) – Variety of credit types, such as credit cards, loans, mortgages.

- New credit inquiries (10%) – Opening many new accounts in a short period can lower scores.

As you can see, payment history and credit utilization together make up 65% of your FICO score calculation. Focusing on those areas through responsible spending and on-time payments can start improving your 611 score.

Tips for Raising a 611 Credit Score

Here are some practical steps to take if your goal is boosting a 611 credit score:

1. Review credit reports and identify issues

Pull your credit reports from AnnualCreditReport.com and comb through them to spot any negative items dragging your score down. Look for late payments, collections accounts, bankruptcies, etc. Knowing your credit history will help you pinpoint areas to improve.

2. Pay all bills on time

Payment history being 35% of your score means timely payments should be a top priority. Set up autopay through creditor websites or your bank to ensure you never miss a due date.

3. Pay down balances

With credit utilization being 30% of your score, balances play a key role. Pay down card and loan balances to get utilization below 30% on each account and overall. This can boost scores quickly as it updates real-time when balances are lowered.

4. Become an authorized user

If you have a family member or spouse with good credit, ask if they will add you as an authorized user on a long-held account. Their good history can be added to your reports and scores.

5. Limit new credit applications

New credit makes up 10% of FICO scores. Applying for too many new accounts in a short period can indicate risk and lower your scores. Wait at least six months between applications.

6. Build positive history

Continue using credit responsibly over time. As the length of your history grows and new positive payments are added each month, your scores will gradually improve. Patience and diligence are key.

Lending Implications of a 611 FICO Score

While a 611 credit score presents some challenges, it is still possible to qualify for credit and lending. Here is a look at potential implications across different financing needs:

Credit Cards – You may need to start with options geared to fair credit, like secured cards. Limiting applications and keeping balances low once approved will help increase scores.

Auto Loans – Approval is achievable but expect higher interest rates around 10-20%. Shopping lenders and having a down payment can improve your chances.

Mortgages – Most conventional loans require minimum 620 scores. But FHA loans allow scores as low as 500, with higher rates/fees.

Personal Loans – Qualifying will be difficult with a 611 score. Try a credit-builder loan from a credit union to establish positive history.

Other Lending – Rental and utilities may require larger deposits. Explore guarantor options. Cell phone plans may need down payments.

The key is reviewing all financing options, even those aimed at fair/poor credit. Compare terms across multiple lenders and look for opportunities to establish positive payment history. A 611 FICO is not insurmountable, but will require diligence.

What 611 Credit Score Means for You

Some employers pull credit reports for jobs that involve financial responsibility. A 611 credit score may raise concerns but not a sole disqualifier.

Some insurers use credit-based scores to set premiums. A 611 credit score may mean higher insurance rates for auto or home.

FHA loans are an option for people with fair to poor credit scores as they only require a minimum credit score of 580. Here are some tips to help you:

- Save for a bigger down payment

- Work on paying off existing debt

- Get a co-signer if needed

Also, building credit through good financial habits can improve mortgage options over time.

Other Mortgage Options:

- VA Loans: If eligible, VA loans have no minimum credit score requirement.

- USDA Loans: Rural development loans may have flexible credit score requirements

Your credit card options may be limited but there are still some options to help you build credit:

- Secured Credit Cards: These cards require a security deposit which becomes your credit limit. They are great for building or rebuilding credit as your payment history is reported to the credit bureaus. OpenSky is a great option!

- Store Credit Cards: Offered by retailers, these cards may have higher interest rates and fees but are easier to get with poor credit. They can help you build credit if you make regular, on-time payments.

- Credit-Builder Credit Cards: For people with lower credit, these cards have lower limits and higher interest rates but can be a good starting point.

What Affects Your Score

Credit scores are made up of several factors, each weighted differently. These are the main factors that are used in calculating credit scores:

- Payment History (35%): Missed or late payments will hurt your score.

- Credit Utilization (30%): How much credit you’re using compared to your limits. High utilization will lower your score.

- Length of Credit History (15%): Longer credit history will help boost your score.

- Credit Mix (10%): Having a variety of credit types (e.g., credit cards, loans) will help your score.

- New Credit (10%): Applying for multiple credit accounts in a short period will lower your score due to hard inquiries.

With this understanding, you’re empowered to take steps to improve your credit score.

What is Considered A Good FICO Score?

FAQ

What does a FICO score of 611 mean?

A FICO® Score☉ of 611 places you within a population of consumers whose credit may be seen as Fair. Your 611 FICO® Score is lower than the average U.S. credit score. 17% of all consumers have Scores in the Fair range (580-669).

Can I buy a house with a 611 credit score?

Can I get a mortgage with an 611 credit score? Yes, your 611 credit score can qualify you for a mortgage.

What is an acceptable FICO score?

For example, FICO® considers anything between 670 and 739 a good credit score, while VantageScore® says good credit scores fall between 661 and 780. Keep reading to take a closer look at credit scores, including how they’re determined, who’s looking at them, and what you can do to monitor and improve yours.

Can you get a car with a 611 credit score?

There’s no minimum credit score required to get an auto loan. However, a credit score of 661 or above—considered a prime VantageScore® credit score—will generally improve your chances of getting approved with favorable terms. For the FICO® Score☉ , a good credit score is 670 or higher.